Red Creek is a quiet rural locality in South Australia's Murray Bridge region, and like much of the Murray Bridge LGA, it's home to a mix of older and mid-era freestanding homes on generous blocks. For homeowners in this area, understanding what drives your insurance premium — and whether you're getting a fair deal — can make a real difference to your household budget.

This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom freestanding home in Red Creek SA 5255, comparing it against local, state, and national benchmarks so you can make an informed decision.

---

Is This Quote Fair?

The annual premium for this property came in at $1,303 per year (or $120/month), covering a building sum insured of $300,000 and $60,000 in contents. Our pricing analysis rates this quote as CHEAP — below average — which is great news for the homeowner.

To put that in context:

- The Murray Bridge LGA average premium is $1,970/yr

- The South Australian state average is $1,933/yr, with a median of $1,787/yr

- The national average sits at $2,965/yr, with a median of $2,716/yr

At $1,303/yr, this quote is roughly 33% below the SA state average and an impressive 56% below the national average. Even compared to the SA median of $1,787/yr, this homeowner is saving over $480 annually. By any measure, this is a competitive result.

The building excess is set at $2,000 and the contents excess at $1,000, which are fairly standard figures. A higher excess is one way insurers offer lower premiums, so it's worth confirming these levels suit your financial situation — but for many households, the trade-off is well worth it given the premium savings on offer here.

---

How Red Creek Compares

While there isn't enough suburb-level data to calculate a Red Creek-specific average, we can use the SA state figures and Murray Bridge LGA data as reliable reference points.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,303 |

| Murray Bridge LGA Average | $1,970 |

| SA State Average | $1,933 |

| SA State Median | $1,787 |

| National Average | $2,965 |

| National Median | $2,716 |

The gap between this quote and the national average is striking. Homeowners in major metropolitan areas — particularly in Queensland and New South Wales — often face significantly higher premiums driven by extreme weather risk, higher rebuilding costs, and dense urban property values. Red Creek's relatively low-risk profile appears to be working in this homeowner's favour.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining, as they each play a role in how insurers calculate risk and set premiums.

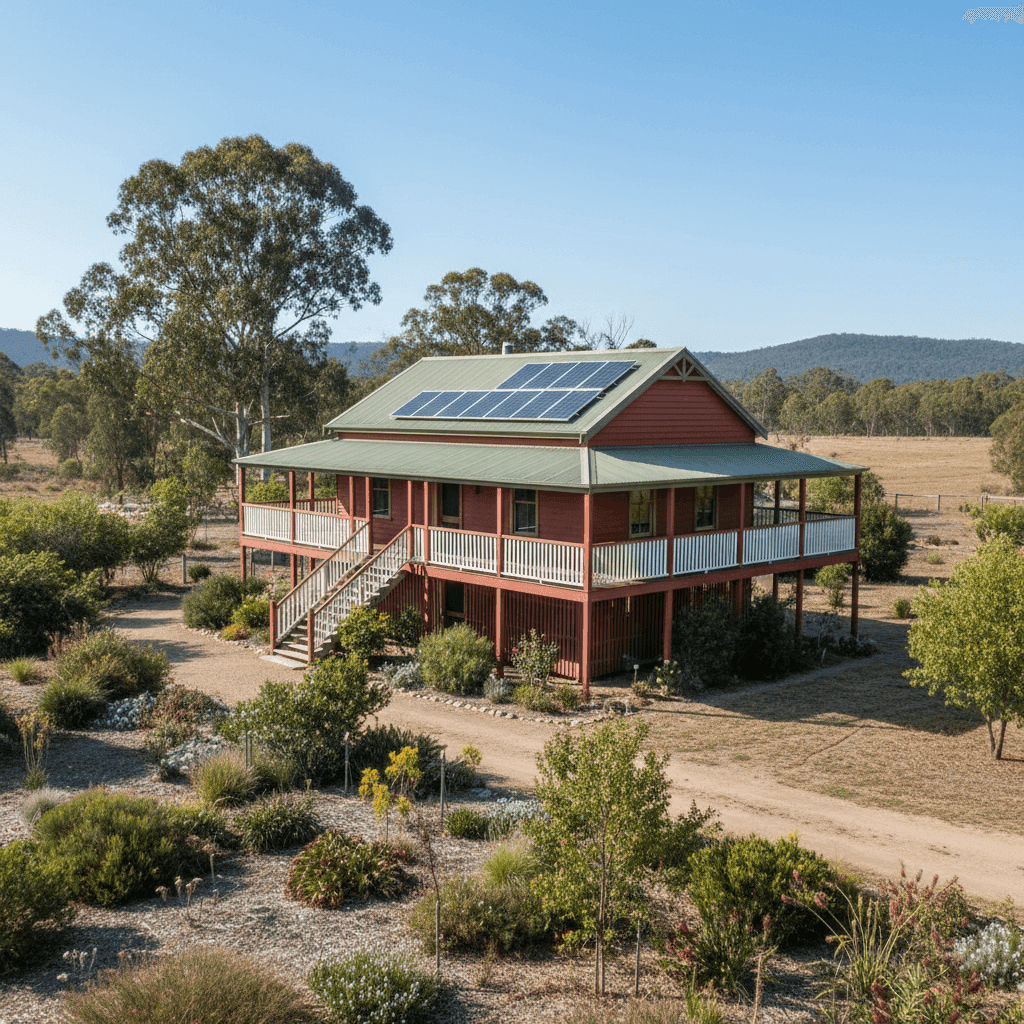

Weatherboard Timber Walls

Weatherboard wood is a classic Australian construction material, particularly common in homes built in the 1980s and 1990s. While it has great aesthetic appeal and is well-suited to rural settings, timber-clad homes can attract slightly higher premiums than brick veneer due to increased fire risk and susceptibility to moisture damage over time. Keeping the exterior well-maintained — regular painting, caulking, and checking for rot — can help demonstrate good upkeep and potentially support favourable renewal pricing.

Steel/Colorbond Roof

A Colorbond steel roof is generally viewed positively by insurers. It's durable, low-maintenance, and performs well in high-wind events and bushfire-prone conditions. Compared to older tile roofs, Colorbond is less likely to crack, leak, or require costly repairs, which can translate into lower claims risk.

Elevated Foundation (Stumps)

This home sits elevated on stumps by at least one metre. Elevated homes offer a natural defence against localised flooding and moisture ingress — a meaningful advantage in parts of South Australia that can experience seasonal flooding, particularly near the Murray River. However, elevated homes can also be more vulnerable to wind uplift, so ensuring the structure is well-anchored is important.

Solar Panels

The property has solar panels installed. It's essential that your policy explicitly covers solar panels as part of the building sum insured. Some policies include them automatically; others treat them as an optional add-on. Given that a quality solar system can represent $5,000–$15,000 in value, confirming coverage is a must.

Timber/Laminate Flooring

Timber and laminate floors can be costly to replace after a water or fire event. Make sure your building sum insured accounts for the full replacement cost of these finishes, particularly if they cover a significant portion of the 139 sqm floor area.

Construction Year: 1994

At roughly 30 years old, this home is approaching the age where certain systems — plumbing, wiring, roofing fixings — may begin to show wear. Insurers sometimes scrutinise older homes more closely, though a 1994 build is far from unusual in the rural SA market. Keeping maintenance records and addressing issues proactively can help at renewal time.

---

Tips for Homeowners in Red Creek

1. Review your building sum insured regularly Construction costs have risen sharply across Australia in recent years. A sum insured of $300,000 for 139 sqm may be adequate today, but it's worth checking against current per-square-metre rebuild costs in regional SA (typically $1,800–$2,500/sqm for standard construction). Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Confirm solar panel coverage explicitly Before renewing or switching policies, ask your insurer in writing whether your solar panels are covered under the building section, what events are included (e.g. storm, fire, accidental damage), and whether there's a separate sublimit. Don't assume — check.

3. Maintain your weatherboard cladding Timber exteriors require more ongoing maintenance than brick. A well-maintained home is less likely to generate a claim, and some insurers reward this at renewal. Peeling paint, gaps in cladding, or signs of rot should be addressed promptly.

4. Consider your excess levels carefully With a $2,000 building excess and $1,000 contents excess, you're carrying a reasonable amount of self-insurance. This helps keep premiums low, but make sure you have that amount readily accessible in an emergency. If cash flow is a concern, a slightly lower excess (at a modest premium increase) may offer better peace of mind.

---

Compare Your Home Insurance Today

Whether you're renewing your current policy or shopping around for the first time, it pays to compare. The quote analysed here is already well below average — but there may be even better options available depending on your specific circumstances.

Get a home insurance quote at CoverClub and see how your premium stacks up against the market in minutes. With no obligation and clear side-by-side comparisons, CoverClub makes it easy for Australian homeowners to find cover that's genuinely good value.