If you own a free standing home in Redcastle, VIC 3523, you're likely curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. This article breaks down a real building insurance quote for a three-bedroom weatherboard home in Redcastle, comparing it against local, state, and national benchmarks so you can make a genuinely informed decision.

---

Is This Quote Fair?

The short answer: yes — this is an excellent result.

The quote in question comes in at $2,026 per year (or roughly $194 per month), covering building only with a sum insured of $508,000 and a building excess of $5,000. Our price rating for this quote is CHEAP, meaning it sits meaningfully below what most homeowners in the area are paying.

To put that in perspective, the suburb average premium in Redcastle is $3,689 per year, and the median sits at $3,564. That means this quote is approximately 45% below the suburb average — a significant saving of over $1,600 annually. Even compared to the 25th percentile of local quotes (i.e., the cheapest quarter of premiums in the area), which sits at $2,995, this quote still comes in well under the mark.

A building excess of $5,000 is on the higher side and is worth noting — this is likely one of the levers that has helped bring the annual premium down. If you'd prefer a lower excess, it's worth requesting an alternative quote structure, as reducing the excess will generally increase the premium.

---

How Redcastle Compares

Redcastle is a small rural locality in the Mitchell LGA, north-central Victoria — and its insurance pricing reflects a market that sits above both the state and LGA averages, though this particular quote bucks that trend entirely.

Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Redcastle (suburb) | $3,689/yr | $3,564/yr |

| Mitchell LGA | $2,743/yr | — |

| Victoria (state) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

| This quote | $2,026/yr | — |

A few things stand out here. First, Redcastle's suburb average of $3,689 is notably higher than both the Victorian state average of $3,000 and the Mitchell LGA average of $2,743. This suggests that insurers are pricing some elevated risk into the Redcastle postcode — likely related to bushfire exposure, which is a real consideration for rural Victorian properties.

Second, while the national average of $5,347 looks alarming, it's heavily skewed by high-risk coastal and cyclone-prone regions in Queensland and Western Australia. The national median of $2,764 is a far more useful comparison point for a property like this — and this quote still comes in comfortably below it.

It's also worth noting that the suburb sample size here is 18 quotes, which is a reasonably small dataset. Individual results can vary considerably depending on the insurer, the specific property details, and the coverage options selected.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers assess and price the risk.

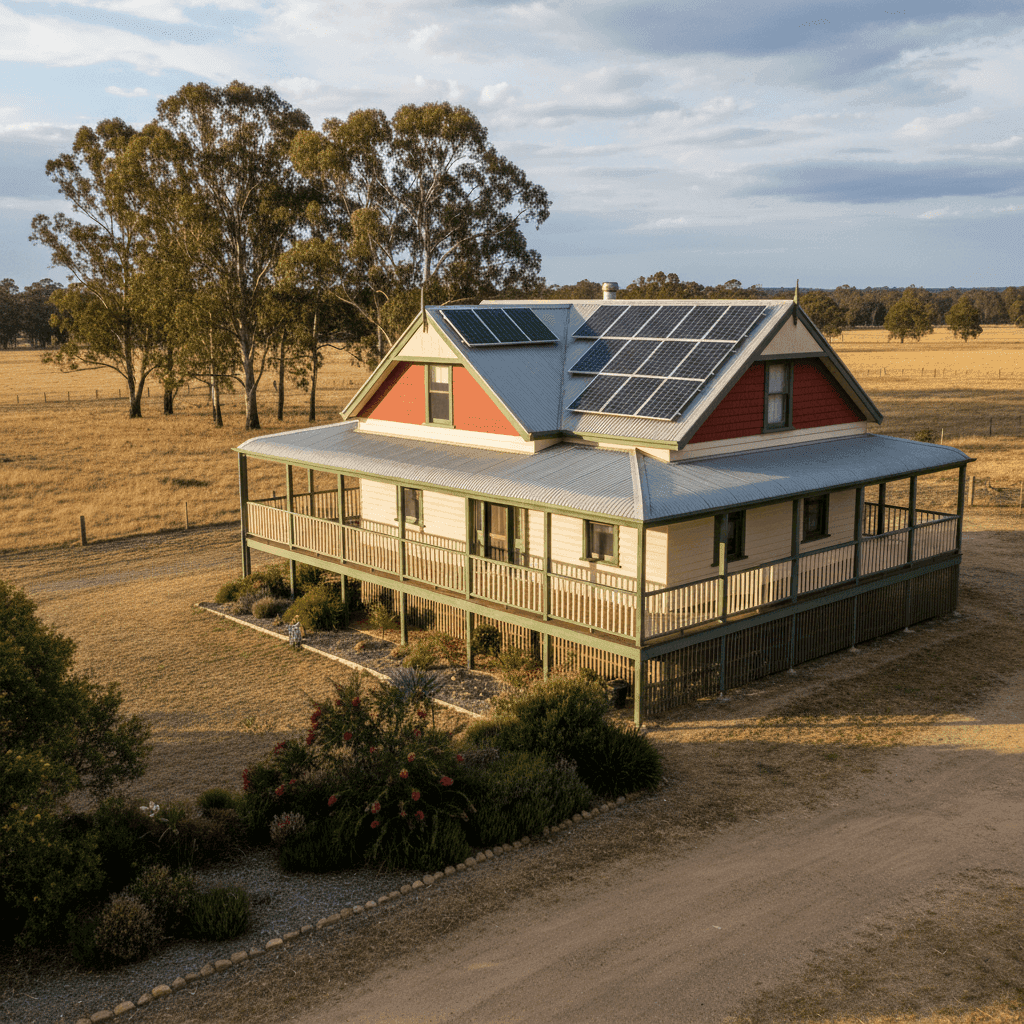

Weatherboard timber walls are one of the most significant factors. Timber-framed and clad homes are generally considered higher risk than brick veneer or full brick construction, as they are more susceptible to fire damage and can be more costly to repair or rebuild. Insurers typically charge more for weatherboard homes — so achieving a below-average premium with this construction type is a genuinely good outcome.

Steel/Colorbond roofing is viewed favourably by most insurers. It's durable, low-maintenance, and performs well in both fire and storm conditions compared to older materials like terracotta tiles or asbestos sheeting. This likely helps offset some of the risk associated with the timber walls.

Stump foundations are common in older and rural Victorian homes and can attract scrutiny from insurers — particularly around the risk of subsidence or structural movement. The home was built in 2001, which means it's relatively modern for a stumped property, and this may have helped keep the premium competitive.

Solar panels are present on this property. While solar systems add value to the home, they can also add complexity to insurance claims (particularly in storm or hail events). It's important to confirm with your insurer that the solar system is included in the sum insured and covered under the policy.

Ducted climate control is another feature worth checking. Ducted systems can be expensive to repair or replace, and not all standard building policies automatically cover them in full. Verify that your policy includes HVAC systems as part of the building cover.

The 130 sqm building size and standard fittings quality both contribute to a relatively straightforward rebuild cost assessment, which likely helps keep the premium manageable. The sum insured of $508,000 appears reasonable for a property of this size and specification in regional Victoria.

---

Tips for Homeowners in Redcastle

1. Review your bushfire risk rating and policy terms Rural properties in north-central Victoria can fall within bushfire-prone zones. Check whether your property has a Bushfire Attack Level (BAL) rating and confirm that your policy covers bushfire damage — including ember attack. Some policies have specific exclusions or sub-limits in high-risk areas.

2. Confirm your solar panels are covered Solar panel systems should be explicitly listed in your building sum insured. Ask your insurer whether panels are covered for storm damage, hail, and accidental breakage, and whether the inverter is included. Don't assume — get it in writing.

3. Reassess your sum insured regularly Building costs in regional Victoria have risen significantly in recent years due to labour shortages and material price increases. A sum insured that was accurate two years ago may no longer reflect the true cost of rebuilding your home. Consider using a building cost calculator or speaking with a quantity surveyor to verify your figure.

4. Understand the trade-off of a high excess The $5,000 building excess on this policy is higher than typical. While it reduces the annual premium, it means you'll need to cover the first $5,000 of any building claim yourself. If your financial buffer is limited, it may be worth comparing quotes with a lower excess to find the right balance for your situation.

---

Compare Your Own Quote

Whether you're renewing your existing policy or shopping around for the first time, it pays to see what the market has to offer. CoverClub makes it easy to compare home insurance quotes across multiple insurers in minutes — so you can see exactly where your premium sits relative to your neighbours.

Get a quote today at CoverClub and find out if you're paying a fair price for your Redcastle home.