If you own a free standing home in Redridge, QLD 4660, you've probably wondered whether you're paying a fair price for home and contents insurance — or whether your insurer is taking you for a ride. This article breaks down a recent quote we analysed for a three-bedroom, two-bathroom home in Redridge, comparing it against local, state, and national benchmarks to help you understand what's driving the price.

---

Is This Quote Fair?

The annual premium for this property came in at $1,021 per year (or roughly $94 per month), covering both building (insured at $370,000) and contents ($43,000). Our price rating for this quote? Cheap — well below average.

To put that in perspective: the average home and contents premium across Queensland sits at $4,547 per year, with a state median of $3,931. Nationally, the average is $2,965 and the median is $2,716. This quote comes in at roughly 78% below the Queensland average and 66% below the national average — a genuinely exceptional result.

For a newly built home in regional Queensland, this kind of premium is rare. Several factors specific to this property are working strongly in the homeowner's favour, which we'll unpack below.

---

How Redridge Compares

While there's no suburb-level data available for Redridge at this stage, we can benchmark against the broader region and state. The Fraser Coast LGA average premium is $3,385 per year — still more than three times higher than this quote.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,021 |

| Fraser Coast LGA Average | $3,385 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

Queensland consistently records some of the highest home insurance premiums in the country, largely driven by the state's exposure to cyclones, flooding, and severe storms. The Fraser Coast region is no exception — many homeowners in the area face elevated premiums due to weather-related risk. That makes this quote all the more noteworthy.

You can explore more data for your area on the Redridge suburb stats page, or browse the Queensland state overview and national insurance statistics to see how your premium stacks up more broadly.

---

Property Features That Affect Your Premium

Insurance underwriters assess dozens of variables when pricing a policy. For this particular property, several characteristics are likely contributing to the favourable premium:

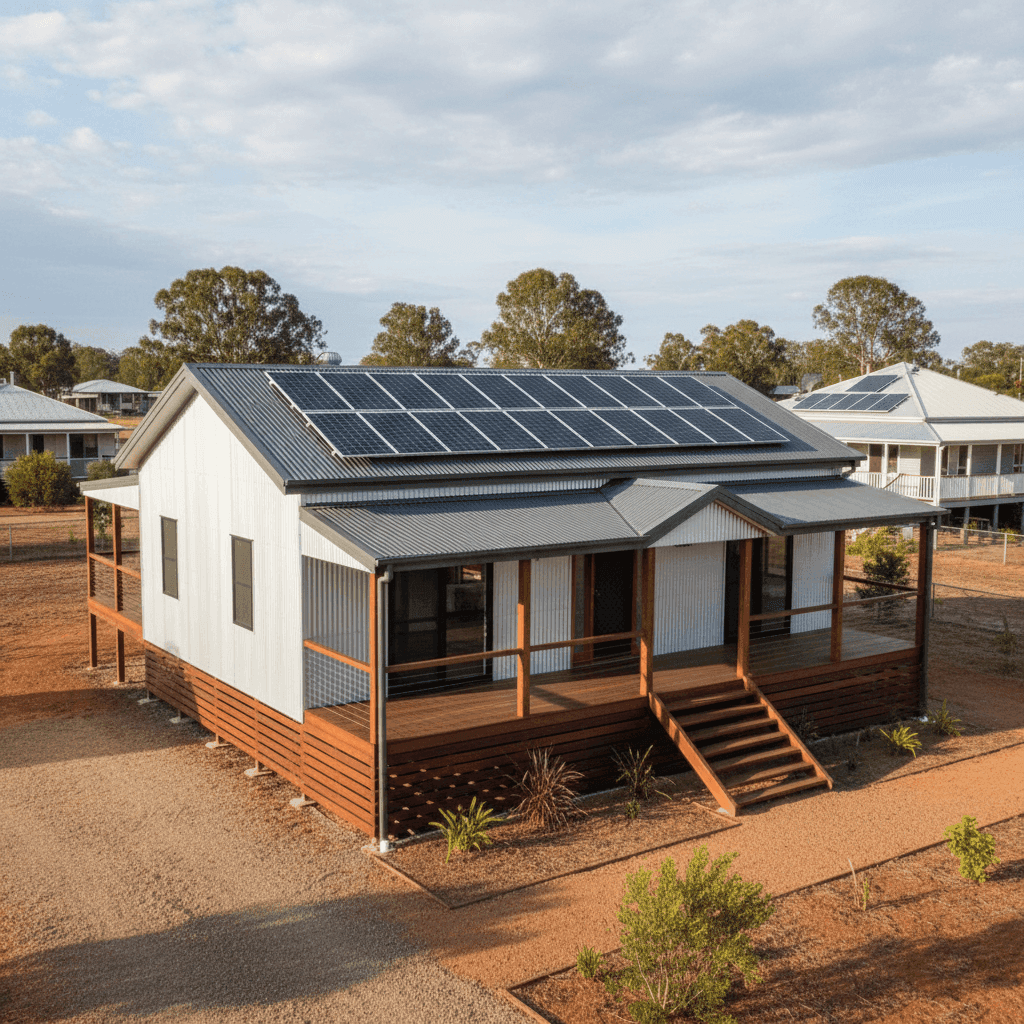

🏗️ Brand New Construction (2024)

This home was built in 2024, making it essentially brand new. Modern builds comply with the latest Australian building codes, which means stronger structural integrity, better fire resistance, and improved resilience to weather events. Insurers reward this with lower premiums.

🧱 Aluminium Walls & Colorbond Roof

Aluminium cladding and steel (Colorbond) roofing are both durable, low-maintenance materials that perform well in Queensland's harsh climate. They're resistant to corrosion, fire, and impact — all factors that reduce an insurer's risk exposure compared to, say, weatherboard or older fibrous cement cladding.

🏠 Elevated on Stumps

The home is elevated by at least one metre on stumps — a classic Queensland design that offers real practical benefits. Elevation reduces flood and stormwater inundation risk significantly, which is a major pricing factor in coastal and riverine Queensland communities. This is likely one of the biggest contributors to the lower-than-average premium.

☀️ Solar Panels

Solar panels are listed as a feature of this property. Most insurers include solar panels under building cover, so it's important to confirm they're accounted for in your sum insured. At $370,000, the building cover appears appropriate for a 139 sqm home of this quality, but it's worth verifying that the replacement cost of your solar system is factored in.

🚫 No Cyclone Risk Zone

Despite being in Queensland — a state synonymous with tropical weather — this property is not located in a designated cyclone risk area. Cyclone loading adds a significant surcharge to premiums across much of northern and coastal QLD, so being outside that zone is a meaningful advantage.

🪵 Timber/Laminate Flooring

Timber and laminate floors are generally viewed neutrally by insurers from a risk standpoint, though they can be costly to replace after water damage. Ensuring your contents and building sums insured reflect the replacement value of your flooring is a sensible step.

---

Tips for Homeowners in Redridge

Even with a competitive premium, there are always ways to protect yourself better and ensure you're getting full value from your policy.

1. Review Your Sum Insured Annually

Construction costs have risen sharply across Australia in recent years. A $370,000 sum insured may be appropriate today for a 139 sqm new build, but it's worth reassessing each year at renewal. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Confirm Solar Panels Are Covered

Solar panel systems can cost anywhere from $5,000 to $15,000 or more. Check your policy wording to confirm whether your panels are covered under the building section, and whether damage from hail, storm, or electrical faults is included. If in doubt, ask your insurer directly.

3. Consider Your Excess Strategy

This policy has a $2,500 building excess and a $500 contents excess. A higher building excess is one reason the premium is so low — you're essentially self-insuring for smaller claims. Make sure you're comfortable with that trade-off and that you have savings available to cover the excess if needed.

4. Don't Set-and-Forget Your Contents Value

$43,000 in contents cover is a reasonable starting point for a three-bedroom home, but it's easy to accumulate more than you realise. Electronics, furniture, appliances, clothing, and tools all add up. Do a quick home inventory every year or two to make sure your contents sum insured still reflects reality.

---

Compare Your Own Quote

Whether you're renewing your policy or buying insurance for the first time, it pays to shop around. Queensland homeowners are often significantly overpaying — and as this quote shows, the right property features combined with the right insurer can make an enormous difference.

Get a home insurance quote at CoverClub and see how your premium compares to the averages in your area. It takes just a few minutes and could save you thousands.