Riverhills is a quiet, leafy suburb in Brisbane's western corridor, popular with families drawn to its spacious blocks, established streetscapes, and easy access to Centenary Highway. For owners of a free standing home in this area, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget. This article breaks down a recent insurance quote for a four-bedroom, two-bathroom brick home in Riverhills (QLD 4074) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,223 per year (or $218/month), covering both building (sum insured: $626,000) and contents ($30,000), each with a $1,000 excess. CoverClub's pricing engine has rated this quote as Fair — Around Average, which is a reasonable outcome for a property of this size and age.

So what does "fair" actually mean in dollar terms? Looking at the suburb-level data for Riverhills:

- The suburb average sits at $2,598/year

- The suburb median is $2,273/year

- The 25th percentile (the cheaper end) is $1,653/year

- The 75th percentile (the pricier end) is $2,884/year

At $2,223, this quote lands just below the suburb median — meaning roughly half of comparable quotes in the area are more expensive. It's comfortably within the middle band of the market, sitting between the 25th and 75th percentiles. That's a solid position to be in, though it's worth noting there is still meaningful room to potentially improve the price by shopping around, particularly if you can edge closer to that $1,653 lower-quartile mark.

---

How Riverhills Compares

One of the more striking aspects of this quote becomes clear when you zoom out to the broader Queensland insurance market. The state average premium across QLD is a staggering $9,129 per year, with a median of $3,903/year. That gulf between average and median tells an important story — Queensland's insurance costs are heavily skewed upward by high-risk areas, particularly flood-prone regions, cyclone corridors in the north, and coastal zones. Riverhills, by comparison, benefits from its inland, non-cyclone-rated location.

Even against national benchmarks, the picture is favourable. The national average sits at $5,347/year, with a median of $2,764/year. This quote of $2,223 falls below both the national median and the Queensland median — a genuinely competitive result.

Perhaps most telling is the LGA (Brisbane) average of $16,277/year. This figure is dramatically inflated by high-value properties and significant flood-risk homes across the broader Brisbane council area, so it shouldn't be used as a direct benchmark — but it does underscore how much variation exists even within a single local government area.

| Benchmark | Premium |

|---|---|

| This Quote | $2,223/yr |

| Riverhills Suburb Median | $2,273/yr |

| Riverhills Suburb Average | $2,598/yr |

| QLD State Median | $3,903/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers are willing to charge. Understanding them helps you anticipate future movements in your premium and identify opportunities to manage costs.

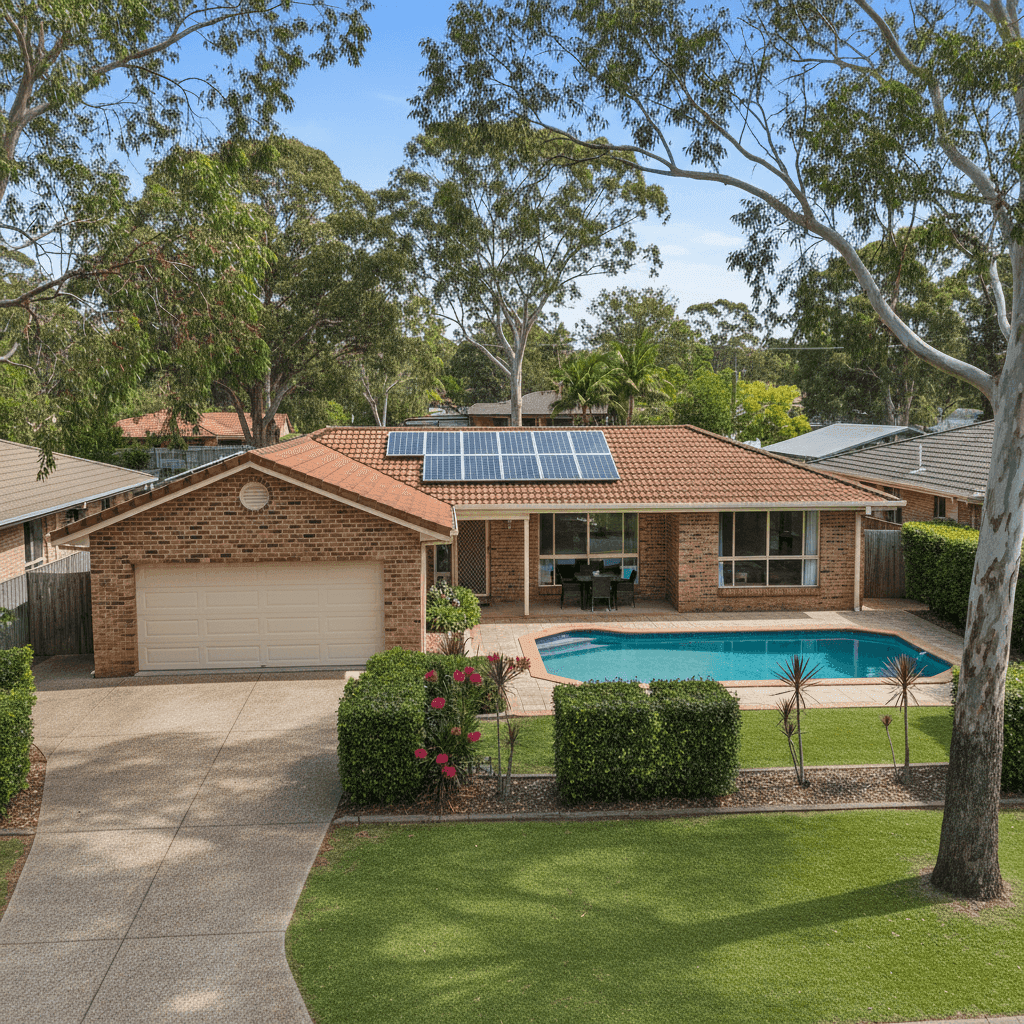

Brick Veneer Construction & Tiled Roof Brick veneer walls combined with a tiled roof are generally viewed favourably by insurers. Brick veneer offers good fire resistance and structural durability, while concrete or terracotta tiles are considered a lower fire risk than timber or metal alternatives. This combination typically attracts more competitive premiums compared to lightweight cladding or older fibrous cement construction.

Built in 1977 A construction year of 1977 places this home in an era before modern building codes introduced stricter standards around cyclone tie-downs, energy efficiency, and materials. While the home isn't considered "old" in the way a pre-war property might be, insurers may factor in the age of roofing, plumbing, and electrical systems when assessing risk. Regular maintenance and documented upgrades (such as rewiring or roof restoration) can help keep premiums in check.

Slab Foundation A concrete slab foundation is the norm for homes of this era in South East Queensland and is generally treated neutrally by insurers. It eliminates some of the subsidence and moisture risks associated with raised timber floors, which is a modest positive from an underwriting perspective.

Swimming Pool The presence of a pool adds a layer of liability exposure that insurers account for in home and contents policies. Beyond the premium impact, it's important to ensure your policy explicitly covers pool-related liability and that the pool structure itself (fencing, filtration equipment, surrounds) is included in your building sum insured.

Solar Panels Solar panels are increasingly common across Brisbane's western suburbs, and most modern home insurance policies include them under building cover — but it's worth confirming this explicitly. Panels represent a meaningful capital asset (often $8,000–$15,000 or more), and their replacement cost should be factored into your building sum insured.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and should be captured within the building sum insured. At 214 sqm, this is a reasonably sized home, and the ducted system adds to the overall replacement cost calculation.

---

Tips for Homeowners in Riverhills

1. Check Your Building Sum Insured Annually Construction costs in South East Queensland have risen sharply over recent years. A sum insured of $626,000 for a 214 sqm brick home works out to roughly $2,925 per sqm — which is within a reasonable range for this type of construction, but worth verifying against a current building cost calculator or quantity surveyor estimate. Being underinsured at claim time can be a costly mistake.

2. Confirm Solar Panels and Pool Equipment Are Covered Read your Product Disclosure Statement carefully to confirm that both your solar panel system and pool equipment (pumps, filters, heating) are explicitly covered under the building section. Some policies treat these as optional extras or cap their coverage.

3. Review Your Contents Sum Insured At $30,000, the contents cover on this policy is on the lower end for a four-bedroom home. A full contents audit — including whitegoods, electronics, furniture, clothing, and tools — often reveals that the true replacement value is considerably higher. Underinsuring contents is one of the most common and costly mistakes homeowners make.

4. Compare at Renewal, Not Just at Purchase Insurance loyalty rarely pays. Insurers frequently offer better pricing to new customers than to existing ones. Set a reminder to compare quotes at least 30 days before your renewal date — this gives you time to negotiate or switch without a coverage gap.

---

Ready to Find a Better Deal?

Whether you're benchmarking your existing policy or shopping for the first time, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Get a personalised quote today and see how much you could save — or simply confirm that you're already getting a fair deal.