If you own a free standing home in Robina, QLD 4226, you're likely paying close attention to the cost of home and contents insurance — especially as premiums across Queensland have climbed sharply in recent years. This article breaks down a real insurance quote for a 3-bedroom, 2-bathroom brick veneer home in Robina, comparing it against suburb, state, and national benchmarks so you can judge whether your own cover is competitively priced.

---

Is This Quote Fair?

The quote in question comes in at $1,605 per year (or $154 per month) for combined home and contents cover, with a building sum insured of $467,000 and contents valued at $50,000. Both the building and contents excesses are set at $2,000.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a meaningful finding. Based on 106 quotes collected for Robina (postcode 4226), the suburb average sits at $3,763 per year, and the median is $3,127 per year. This quote lands well below even the 25th percentile of $2,404 — meaning it's cheaper than at least 75% of comparable quotes in the suburb.

In plain terms: if you're paying around $1,605 annually for a similar property in Robina, you're getting a genuinely competitive deal. Of course, premium comparisons are only meaningful when the underlying cover is equivalent, so it's always worth scrutinising policy inclusions, exclusions, and claim limits — not just the bottom-line price.

---

How Robina Compares

Robina sits within the City of Gold Coast LGA, one of the most expensive local government areas in Australia for home insurance. The Gold Coast LGA average premium is a striking $8,161 per year — more than five times the quote analysed here.

Zooming out further, the picture becomes even more dramatic:

| Benchmark | Annual Premium |

|---|---|

| This quote | $1,605 |

| Robina suburb average | $3,763 |

| Robina suburb median | $3,127 |

| Gold Coast LGA average | $8,161 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

Queensland as a whole is one of the most expensive states in the country for home insurance, driven by elevated risks from flooding, storms, and cyclones across much of the state. The QLD state average of $9,129 per year reflects just how exposed many Queensland homeowners are — particularly in coastal and flood-prone regions.

Nationally, the average home insurance premium sits at $5,347 per year, with a median of $2,764. Robina's median of $3,127 sits modestly above the national median, which is consistent with its Gold Coast location and the broader Queensland risk environment.

The quote analysed here beats every single one of these benchmarks — a strong result by any measure.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its favourable premium. Understanding these factors can help you make smarter decisions about your own cover.

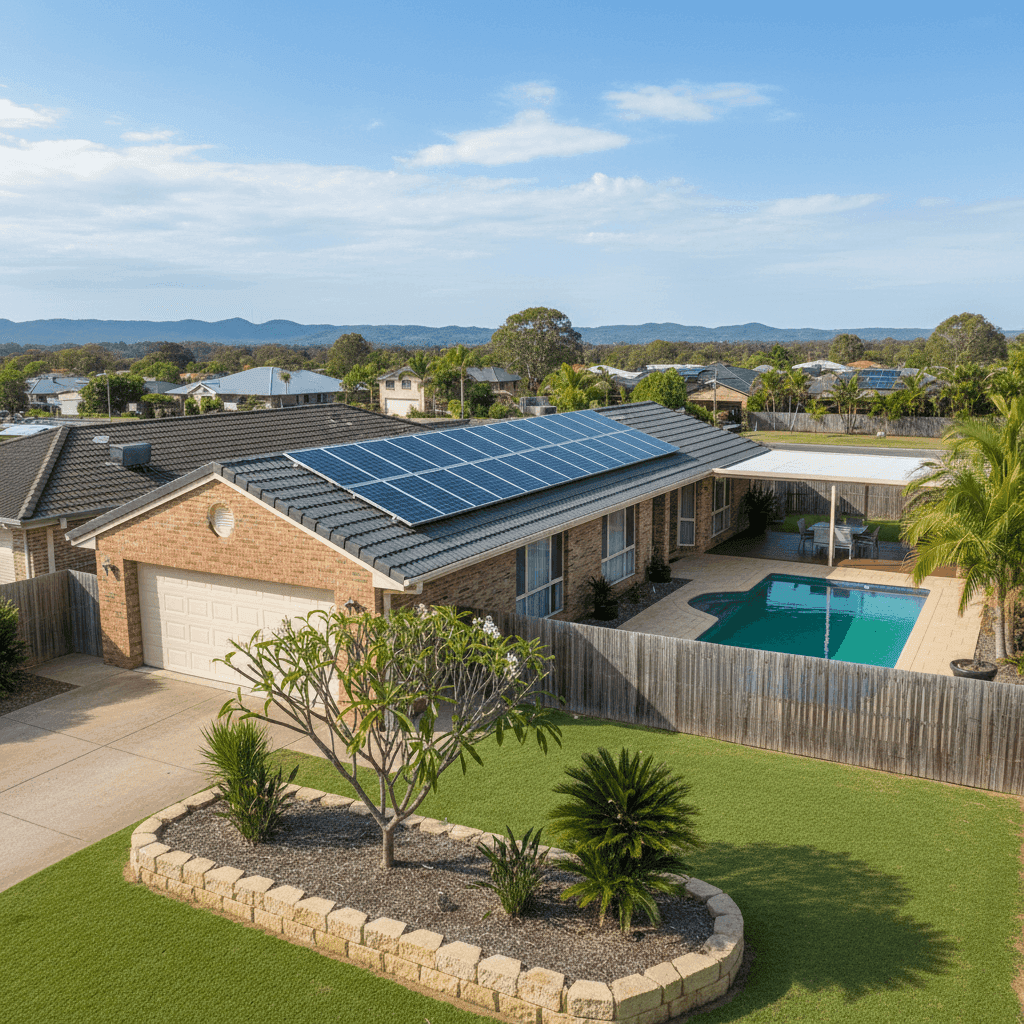

Brick Veneer Construction Brick veneer external walls are generally viewed favourably by insurers. They offer solid fire resistance and structural durability compared to lightweight cladding materials, which can translate to lower rebuild risk and, in turn, lower premiums.

Tiled Roof Concrete or terracotta tile roofs are considered a durable and relatively low-risk roofing material. They perform well in hail and wind events compared to corrugated iron or Colorbond in certain scenarios, though they can be more expensive to repair if damaged. Overall, tiles are a neutral-to-positive factor for insurers.

Slab Foundation A concrete slab foundation is a standard and stable choice for Queensland homes built from the 1990s onward. It generally presents fewer concerns around subsidence or pest damage compared to older timber subfloor constructions.

Construction Year: 1993 At around 30 years old, this home is mature but not aged. Properties built in the early 1990s typically comply with reasonable building standards, though they predate some of the more stringent cyclone and wind-resistance codes introduced after major weather events. This is worth noting for any Queensland homeowner.

Swimming Pool A pool adds some liability exposure and can marginally increase premiums due to the risk of accidents and the cost of damage or contamination following a storm or flood event. It's important to ensure your policy explicitly covers pool infrastructure.

Solar Panels Solar panels are an increasingly common feature on Australian rooftops, but they're not always automatically covered under standard home insurance policies. Homeowners should confirm whether their insurer covers panels as part of the building sum insured — and whether that coverage extends to accidental damage, storm damage, and loss of generation income.

No Cyclone Risk Robina is not classified as a cyclone risk area, which is a significant premium advantage compared to properties further north in Queensland. Cyclone-rated premiums can add hundreds — sometimes thousands — of dollars to annual costs.

---

Tips for Homeowners in Robina

Whether you're reviewing your existing policy or shopping around for the first time, here are four practical steps Robina homeowners can take to get the best value from their home insurance.

- Check your building sum insured regularly. Construction costs in South East Queensland have risen significantly since 2020. A sum insured set a few years ago may no longer be sufficient to fully rebuild your home. Use a building cost calculator or speak with a quantity surveyor to verify your coverage is adequate.

- Confirm solar panels and pool equipment are covered. As noted above, these features aren't always included by default. Review your policy's definitions of "building" and ask your insurer directly whether solar panels, pool pumps, and filtration equipment are covered — and to what limit.

- Consider a higher excess to reduce your premium. The $2,000 excess in this quote is already on the higher side, which likely contributes to the lower annual premium. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, opting for a higher excess can be an effective way to keep ongoing premiums manageable.

- Compare quotes annually. The home insurance market in Queensland is competitive, and premiums can vary enormously between providers for the same property. Don't assume your renewal quote is the best available — use a comparison tool like CoverClub to benchmark your premium before you renew.

---

Ready to Compare Your Home Insurance?

Whether your current premium looks like the one above or you're paying closer to the Gold Coast LGA average, it pays to check. Get a home insurance quote at CoverClub and see how your premium stacks up against real data from your suburb. With over 100 quotes on record for Robina alone, you can make a genuinely informed decision — not just take your insurer's word for it. Visit our Robina suburb stats page to explore the full data set.