If you own a free standing home in Rochedale South, QLD 4123, you've probably wondered whether you're paying a fair price for home insurance — or quietly overpaying year after year. This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom brick veneer home in the suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,455 per year (or $235 per month) for combined home and contents cover, with a $621,900 building sum insured and $173,700 in contents cover. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up when you look at the numbers. The suburb average premium for Rochedale South sits at $2,108 per year, and the median is $2,056 — meaning this quote is modestly above the midpoint of what locals are paying. However, it falls comfortably within the 25th–75th percentile range of $1,569 to $2,562, which tells us it's not an outlier. Roughly half of comparable quotes in the area come in between those two figures, and this one lands squarely in that band.

In short: you're not getting a bargain, but you're not being gouged either. There may still be room to sharpen the price with a bit of shopping around.

---

How Rochedale South Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape. You can explore the full data on the Rochedale South insurance stats page, but here's a quick summary:

| Benchmark | Premium |

|---|---|

| This quote | $2,455/yr |

| Rochedale South suburb average | $2,108/yr |

| Rochedale South suburb median | $2,056/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Brisbane LGA average | $16,277/yr |

The contrast with state and national figures is striking. The Queensland state average of $9,129 per year is heavily skewed by high-risk areas — particularly cyclone-prone regions in Far North Queensland, where premiums can be eye-watering. The national average of $5,347 tells a similar story, pulled upward by flood zones, bushfire corridors, and coastal cyclone belts across the country.

Rochedale South, by comparison, is a relatively benign risk environment. It sits in Brisbane's south-eastern suburbs, outside any cyclone risk zone, and the suburb's median premium of around $2,056 reflects that. This quote at $2,455 is above the suburb median but well below both the state and national averages — a reassuring sign that the property's location is working in the owner's favour.

The Brisbane LGA average of $16,277 may look alarming at first glance, but this figure is heavily influenced by high-value properties and elevated-risk pockets within the broader local government area. It's not a useful benchmark for a standard suburban home like this one.

---

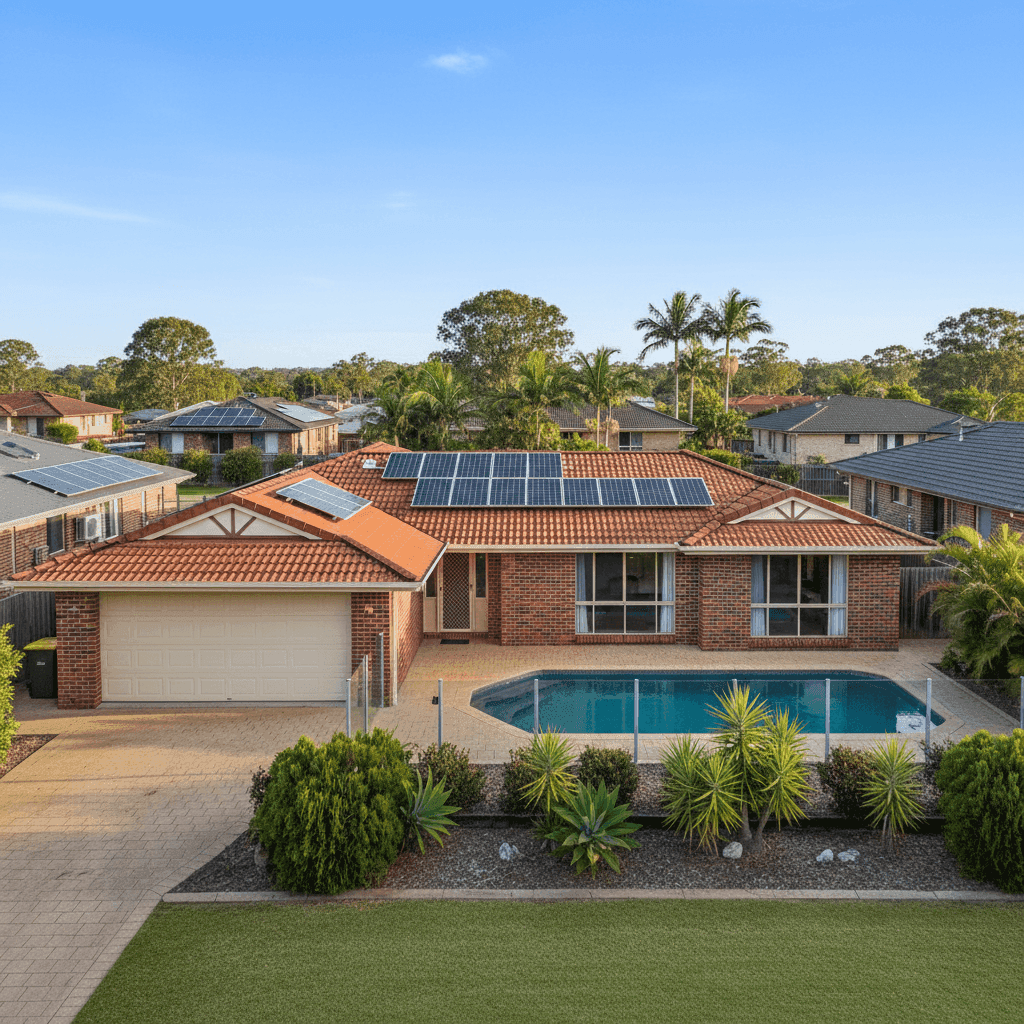

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how the key features stack up:

Brick veneer construction and tiled roof are both viewed favourably by insurers. Brick veneer walls offer solid fire resistance and durability, while a tiled roof — though heavier than Colorbond — is well-regarded for longevity and weather performance in south-east Queensland's subtropical climate. Together, these materials typically attract lower premiums than timber-framed or sheet-metal alternatives.

Slab foundation is another tick in the right column. Slab homes generally have fewer entry points for moisture and pests, and they're considered structurally stable, which insurers tend to price accordingly.

Timber and laminate flooring can be a double-edged sword. These materials are more susceptible to water damage than tiles, which means a burst pipe or flood event could result in a significant claim. It's worth confirming your policy covers accidental water damage to flooring.

The swimming pool adds both lifestyle value and insurance complexity. Pools increase the replacement cost of the property and introduce liability considerations — particularly if the property is ever rented or accessed by visitors. Make sure your policy explicitly covers pool infrastructure, including pumps, filtration systems, and fencing.

Solar panels are increasingly common on Brisbane rooftops, but they're not always automatically covered under standard building policies. With a system installed on this property, it's essential to verify that the panels are included in the building sum insured of $621,900 — or listed as a separate item.

Ducted climate control is another high-value fixture that should be captured in the building sum insured. These systems can cost thousands to repair or replace, and their coverage is sometimes overlooked at policy inception.

Construction year of 1975 means this home is around 50 years old. While it's been built to last, older homes can carry hidden risks — ageing plumbing, outdated wiring, and materials that no longer meet current building codes. Some insurers apply age-related loadings, so it's worth asking about this when comparing quotes.

---

Tips for Homeowners in Rochedale South

1. Verify your sum insured reflects today's building costs Construction costs have risen sharply in recent years. A building sum insured of $621,900 for a 139 sqm home works out to roughly $4,474 per square metre — which is within a reasonable range for a brick veneer home with extras like a pool and ducted air conditioning, but worth revisiting annually. Use an independent building calculator or ask your insurer to confirm the figure is adequate.

2. Confirm solar panels and pool equipment are explicitly covered Don't assume these are included. Ask your insurer in writing whether solar panels and pool infrastructure are covered under the building section, and whether there are any sub-limits or exclusions that apply.

3. Shop around at renewal time A "fair" rating means there's likely a better deal available. Insurers rarely reward loyalty — in fact, new customers often receive more competitive pricing. Set a reminder to compare quotes a few weeks before your renewal date each year.

4. Consider a slightly higher excess to reduce your premium With both excesses set at $500, there may be scope to increase these to $750 or $1,000 in exchange for a lower annual premium. If you have an emergency fund and are unlikely to make small claims, this trade-off can make financial sense over the long term.

---

Find a Better Deal with CoverClub

Whether you're renewing your existing policy or buying cover for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property — no obligation, no hassle. Get a home insurance quote today and find out if you can do better than average.