Rosebank is a quiet, leafy locality in the Northern Rivers region of New South Wales, sitting within the Ballina Local Government Area. It's the kind of place where character-filled homes — many of them older timber cottages — dot a rural-residential landscape. But charm comes with complexity when it comes to insuring your home. This article breaks down a recent building insurance quote for a three-bedroom free standing home in Rosebank (postcode 2480) and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $4,664 per year (or $447/month) for building-only cover, with a $1,000 building excess and a sum insured of $567,000.

Our price rating for this quote is EXPENSIVE — Above Average.

To put that in context, the average building insurance premium across Rosebank sits at around $2,407 per year, with a median of just $1,807. That means this particular quote is running at nearly double the local median — a significant gap that's worth investigating before simply accepting the price.

It's worth noting, however, that the sample size for Rosebank is relatively small (5 quotes), so local averages can shift meaningfully with just a handful of data points. Still, the premium here sits well above the suburb's 75th percentile of $3,006 — meaning it's more expensive than at least three-quarters of comparable quotes in the area.

That said, several property-specific factors (discussed below) can legitimately push a premium higher, so this isn't necessarily a case of being overcharged — it may simply reflect the risk profile of this particular home.

---

How Rosebank Compares

Understanding where Rosebank sits in the broader insurance landscape helps put this quote in perspective. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Rosebank (2480) | $2,407/yr | $1,807/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Ballina LGA | $23,241/yr | — |

A few things stand out here. First, the Ballina LGA average of $23,241 is extraordinarily high — one of the more striking figures in our dataset. This is likely driven by flood-risk properties closer to the coast and river systems within the LGA, which can dramatically skew averages upward. Rosebank itself, being further inland, tends to attract lower premiums than many of its LGA neighbours.

Second, the NSW state average of $9,528 is well above the national average of $5,347, largely because New South Wales includes high-risk coastal and flood-prone zones that inflate the state-wide figure. Rosebank's local averages are actually quite modest by comparison.

You can explore more data for this area on our Rosebank suburb stats page, or broaden your view with NSW state insurance statistics and national home insurance benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely contributing to its above-average premium. Here's what insurers typically pay close attention to:

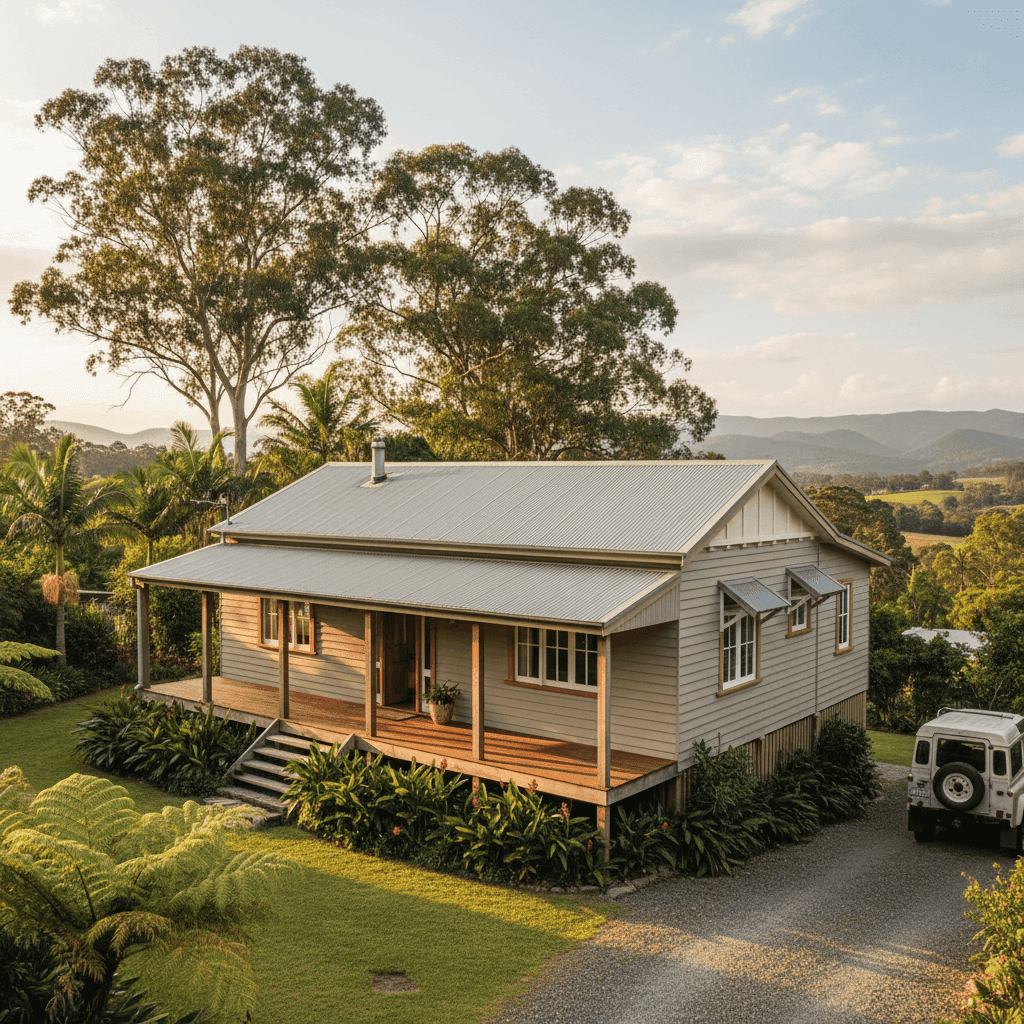

Weatherboard Timber Walls

Weatherboard construction is extremely common in older Australian homes, particularly in regional NSW. While it has undeniable aesthetic appeal, timber is considered a higher fire risk than brick or rendered masonry, and it's more susceptible to rot, pest damage, and general wear over time. Insurers typically charge more to cover weatherboard homes as a result.

Age of Construction (1953)

A home built in 1953 is over 70 years old. Older homes often have ageing electrical wiring, plumbing, and structural elements that increase the likelihood of a claim. Insurers factor this in when pricing a policy, and it can meaningfully lift the premium compared to a newer build.

Stump Foundation

Homes on stumps (also known as pier-and-beam or post foundations) are common in Queensland and northern NSW, and they do come with specific risks — including subfloor moisture issues, pest ingress, and structural movement. Insurers may apply a loading to stump-foundation homes, particularly older ones where the stumps themselves may be original timber.

Timber and Laminate Flooring

While not the most significant rating factor on its own, timber flooring in an older home on stumps can add to the perceived risk profile, particularly around moisture and subfloor ventilation concerns.

Sum Insured of $567,000

The sum insured represents the estimated cost to rebuild the home from scratch, not its market value. At 130 sqm, $567,000 works out to roughly $4,360 per square metre — which is on the higher end but not unreasonable given current construction costs, particularly for a weatherboard home requiring specialist trades. Getting this figure right is critical: underinsuring leaves you exposed, while overinsuring means you're paying more premium than necessary.

---

Tips for Homeowners in Rosebank

If you're a homeowner in Rosebank looking to get better value from your building insurance, here are some practical steps worth taking:

1. Shop around — seriously. With only 5 quotes in our local dataset, the range of premiums in Rosebank can vary considerably between insurers. What one insurer sees as high-risk, another may price more competitively. Comparing multiple quotes is the single most effective way to reduce what you pay. Start comparing now at CoverClub.

2. Review your sum insured annually. Construction costs have risen significantly in recent years, but they can also plateau or shift. Using an independent building cost calculator (many insurers offer one) to validate your sum insured each year ensures you're not over- or under-covered — and that you're not paying unnecessary premium on an inflated figure.

3. Maintain your home proactively. Insurers reward homes that are well-maintained. For a weatherboard home on stumps, this means keeping the subfloor clear and ventilated, treating any timber pest activity promptly, and ensuring the roof and gutters are in good condition. Some insurers may ask about maintenance history at claim time, so staying on top of it protects both your home and your policy.

4. Ask about your excess options. Increasing your excess from $1,000 to $2,500 or higher can noticeably reduce your annual premium. If you're confident you wouldn't claim for smaller incidents, a higher excess is a straightforward way to lower your ongoing costs — just make sure the saving is worth the additional out-of-pocket risk.

---

Compare Your Options with CoverClub

Whether this quote represents good value for your specific circumstances or there's a better deal out there, the only way to know for sure is to compare. CoverClub makes it easy to see how your premium stacks up against real quotes from across Rosebank, NSW, and Australia — so you can make a confident, informed decision.