If you own a free standing home in Rosebud, VIC 3939, you already know the appeal — a relaxed coastal lifestyle on the Mornington Peninsula, just over an hour from Melbourne. But when the home insurance renewal arrives, that laid-back feeling can quickly give way to sticker shock. This article breaks down a real quote for a 2-bedroom, 1-bathroom home in Rosebud, rated Expensive (Above Average), and helps you understand what's driving the cost — and what you can do about it.

---

Is This Quote Fair?

The quote in question comes to $2,471 per year (or $237/month) for combined home and contents cover, with a building sum insured of $453,000 and contents valued at $10,000. Both the building and contents excess sit at $1,000.

Our price rating for this quote is Expensive — Above Average, and the numbers back that up. Compared to the Rosebud suburb average of $1,700/yr, this quote sits roughly 45% higher than what most local homeowners are paying. Even against the suburb's 75th percentile of $1,889/yr, this quote exceeds that benchmark by more than $580.

That said, context matters. The building sum insured of $453,000 is a meaningful figure — rebuilding costs on the Mornington Peninsula aren't cheap — and the property has several characteristics that insurers typically flag as higher risk. More on those shortly.

---

How Rosebud Compares

To put this quote in proper perspective, here's how Rosebud stacks up against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,471 |

| Rosebud Suburb Average | $1,700 |

| Rosebud Suburb Median | $1,600 |

| Rosebud 25th Percentile | $1,290 |

| Rosebud 75th Percentile | $1,889 |

| Mornington Peninsula LGA Average | $2,652 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

(Based on 37 quotes collected for the Rosebud suburb sample.)

A few things stand out here. While the quote looks expensive against the Rosebud suburb average, it actually sits below the Mornington Peninsula LGA average of $2,652 and is comfortably under both the Victorian and national averages. This suggests that while there may be room to shop around within Rosebud, the quote isn't wildly out of step with what similarly aged and constructed homes across the broader region are attracting.

The relatively low suburb median ($1,600) may partly reflect a mix of newer builds, brick-veneer homes, or lower sum-insured properties in the local sample — factors that tend to attract cheaper premiums.

---

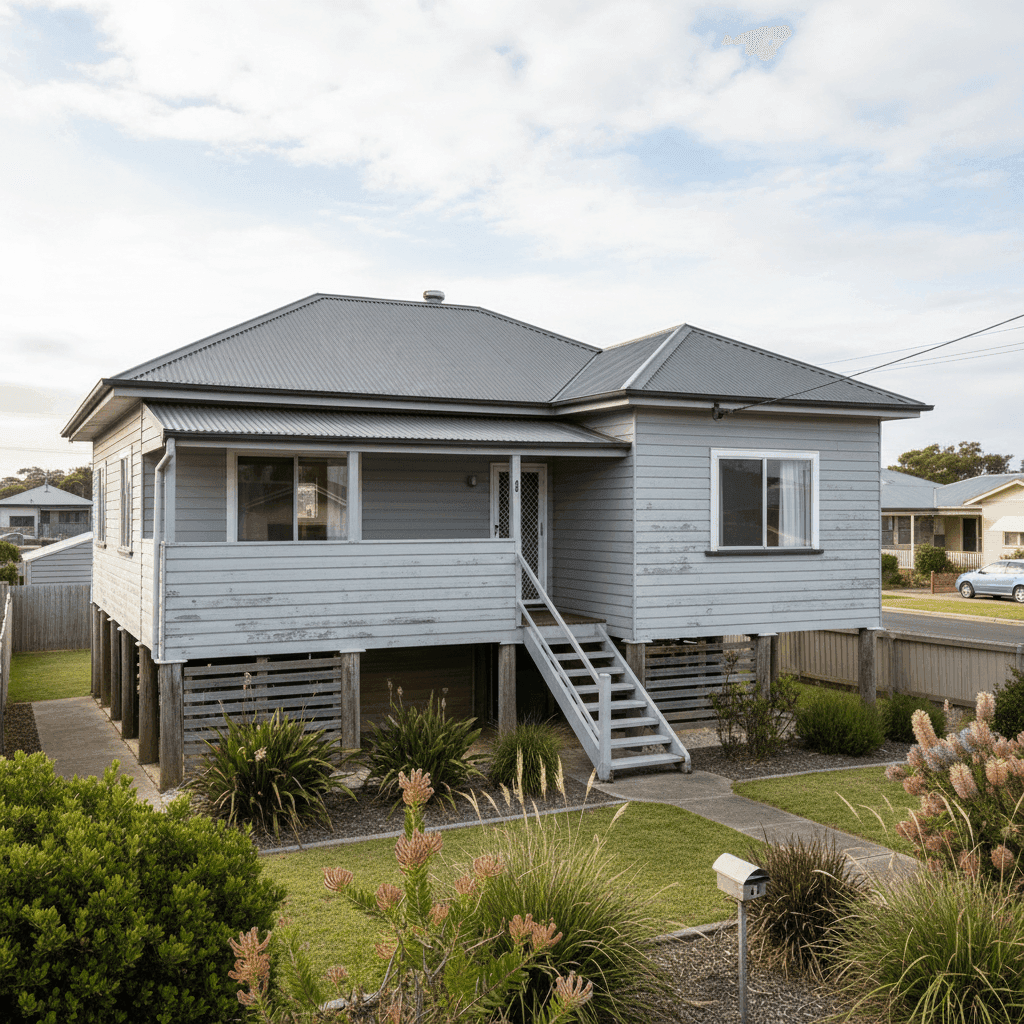

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the above-average premium. Understanding these can help you have a more informed conversation with insurers.

Fibro Asbestos External Walls

This is arguably the single biggest premium driver. Homes built with fibro asbestos cladding — common in Australian coastal towns from the 1950s through to the 1970s — carry a significant loading from most insurers. The reason is straightforward: if the home is damaged and needs repair or rebuilding, the safe removal and disposal of asbestos-containing materials is expensive, tightly regulated, and adds substantially to claim costs. Built in 1965, this home falls squarely in the era when fibro was widely used.

Construction Age (1965)

A home approaching its 60th year carries inherent risks that newer builds don't — ageing electrical wiring, older plumbing, and materials that may no longer meet current building codes. Insurers factor this in when pricing risk.

Stump Foundation

Homes on timber or concrete stumps are elevated off the ground, which can be both a blessing and a curse. While stumps can reduce flood inundation risk in some scenarios, they also introduce vulnerability to subfloor fires, pest damage, and structural movement over time — all of which can influence premium pricing.

Timber and Laminate Flooring

Timber floors, particularly in older homes on stumps, are more susceptible to fire spread and water damage than concrete slabs. Combined with the construction age, this adds another layer of risk in an insurer's assessment.

Ducted Climate Control

While not a major premium driver, the presence of ducted climate control does increase the cost to rebuild or repair, which can push the sum insured — and therefore the premium — slightly higher.

Coastal Location

Rosebud sits on the shores of Port Phillip Bay. Coastal properties can face elevated risks from salt air corrosion, storm surge, and wind events, all of which insurers weigh when calculating premiums in seaside suburbs.

---

Tips for Homeowners in Rosebud

1. Shop Around — Seriously

Given that the suburb median sits at $1,600/yr and this quote is $2,471/yr, there's a real possibility that another insurer will price this risk differently. Not all insurers apply the same loading for fibro asbestos or stump foundations. Compare quotes at CoverClub to see what's available for your specific property.

2. Review Your Sum Insured Carefully

A building sum insured of $453,000 is substantial. Make sure this figure reflects the cost to rebuild (not the market value) of your home. Overinsuring drives up premiums unnecessarily, while underinsuring leaves you exposed. Tools like the Cordell Sum Sure calculator can help you arrive at a more accurate figure.

3. Consider a Higher Excess

The current excess is $1,000 for both building and contents. Opting for a higher voluntary excess — say $2,000 or $2,500 — can meaningfully reduce your annual premium. This works well if you have savings set aside and are unlikely to make small claims.

4. Ask About Asbestos Disclosure and Remediation

Some insurers offer more competitive rates if you can demonstrate that asbestos-containing materials have been professionally assessed, encapsulated, or partially removed. It's worth asking the question — and getting any assessments documented.

---

Ready to Find a Better Deal?

Whether you're renewing your policy or taking out cover for the first time, comparing quotes is the fastest way to make sure you're not overpaying. At CoverClub, we make it easy to see how your premium stacks up against real data from your suburb and beyond. Get a quote today and find out if there's a better deal waiting for your Rosebud home.

You can also explore detailed pricing data for your area at the Rosebud suburb stats page or browse Victoria-wide home insurance trends.