If you own a free standing home in Runnymede, QLD 4615, you might be wondering whether you're paying a fair price for your building insurance — or leaving money on the table. This article breaks down a real building-only insurance quote for a three-bedroom, two-bathroom home in Runnymede, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover for your property.

---

Is This Quote Fair?

The quote in question comes in at $1,926 per year (or $186 per month) for building-only cover on a 214 sqm free standing home with a sum insured of $400,000. The building excess is set at $2,000.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. In a state where insurance premiums have been climbing steadily, landing a quote well below both the Queensland and national averages is a result worth paying attention to.

To put it in perspective: Queensland homeowners are among the hardest hit by rising insurance costs in Australia, driven by extreme weather events, flooding, and cyclone exposure across much of the state. The fact that this Runnymede property is sitting at under $2,000 per year suggests the risk profile here is relatively favourable — and the insurer has priced accordingly.

---

How Runnymede Compares

Let's look at how this $1,926 annual premium stacks up against the broader market:

| Benchmark | Premium |

|---|---|

| This Quote | $1,926/yr |

| Gympie LGA Average | $5,581/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The numbers are striking. This quote is:

- 66% below the Gympie LGA average of $5,581

- 79% below the Queensland state average of $9,129

- 50% below the Queensland median of $3,903

- 30% below the national median of $2,764

Even against the national median — generally considered a more representative benchmark than the average, which can be skewed by high-risk properties — this quote comes in well under. Note that no suburb-level data was available for Runnymede specifically, so the Gympie LGA figure is the closest geographic comparison we have.

You can explore more detailed premium data for this area at the Runnymede suburb stats page, or browse Queensland-wide insurance statistics and national home insurance benchmarks to see the bigger picture.

---

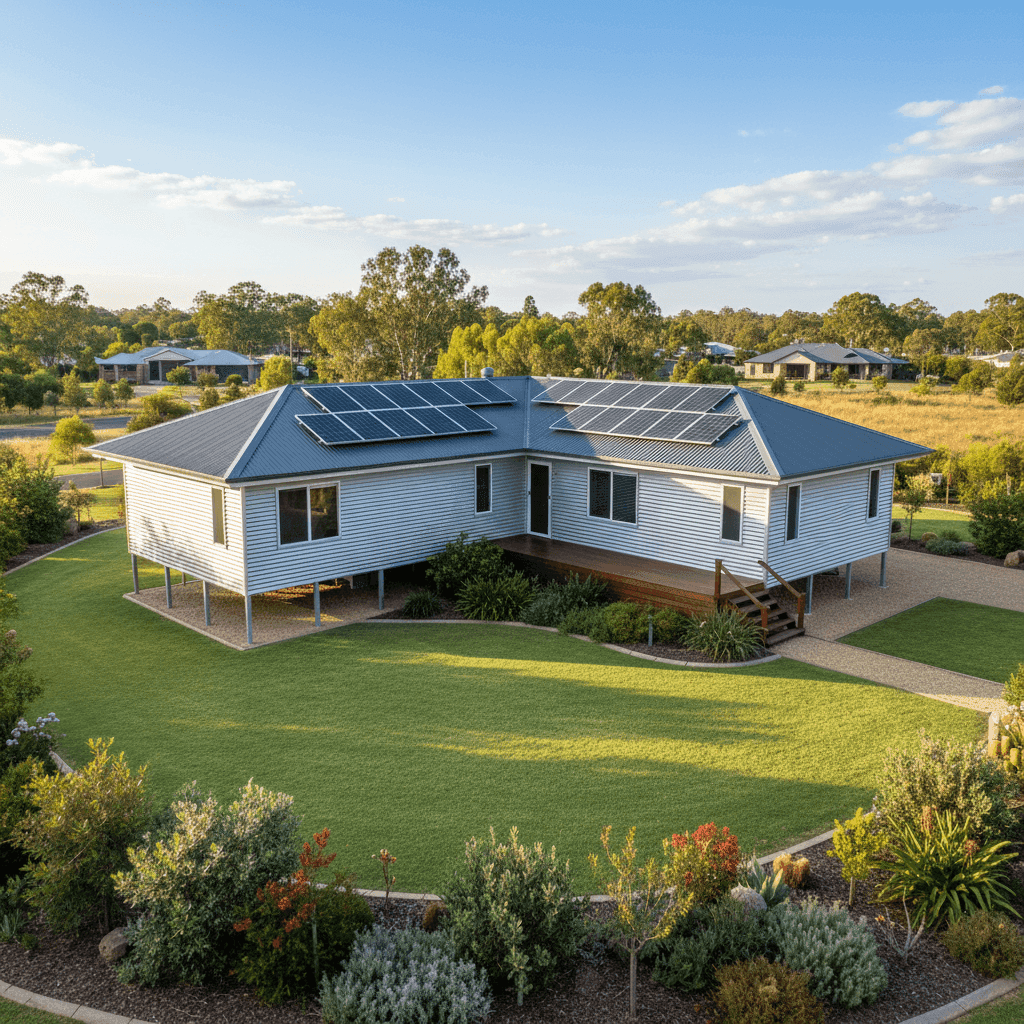

Property Features That Affect Your Premium

Several characteristics of this Runnymede property likely contribute to its competitive premium. Here's how each feature plays a role:

Aluminium Cladding & Colorbond Roof

Aluminium external walls and a steel Colorbond roof are both considered relatively low-risk materials by insurers. Colorbond roofing in particular is highly regarded — it's durable, fire-resistant, and performs well in high winds. These materials tend to attract more favourable premiums compared to older or more vulnerable options like weatherboard or terracotta tiles.

Stump Foundation

The home sits on stumps, which is common in regional Queensland. Stump foundations can offer some resilience in flood-prone areas by elevating the floor above ground level, though they do introduce their own risks (e.g., subfloor damage, pest access). Insurers assess this on a case-by-case basis, but it's generally a neutral-to-positive factor in areas with occasional surface water.

Construction Year: 1998

At roughly 27 years old, this home is modern enough to have been built under relatively up-to-date building codes, but old enough that some systems (plumbing, electrical) may warrant attention. Homes built in the late 1990s generally don't attract the premium loading that older properties sometimes do.

Solar Panels

The presence of solar panels is worth noting. While solar adds value to a property, it also introduces a specific risk — storm or hail damage to panels can be costly to repair or replace. Homeowners should confirm with their insurer whether solar panels are included in the building sum insured or require a separate endorsement.

Ducted Climate Control

Ducted air conditioning systems are a significant fixed asset in any home. Like solar, they should be factored into your sum insured calculation to ensure you're not underinsured in the event of a total loss or major damage.

No Pool, Tiles Flooring, Standard Fittings

The absence of a pool removes one common liability consideration. Tile flooring and standard-quality fittings are straightforward to price and replace, which keeps the overall risk profile clean and predictable for insurers.

Not in a Cyclone Risk Area

This is a meaningful factor. Much of Queensland — particularly northern and coastal regions — carries cyclone risk that can dramatically increase premiums. Runnymede's classification as outside a cyclone risk zone is likely one of the biggest contributors to this below-average premium.

---

Tips for Homeowners in Runnymede

Even with a competitive quote in hand, there are always ways to make sure you're properly protected and getting the best deal possible.

1. Review your sum insured regularly A $400,000 sum insured may be appropriate today, but building costs change. With construction costs rising across Australia in recent years, it's worth reassessing your sum insured annually to avoid being underinsured. Use a building cost calculator or speak with a quantity surveyor if you're unsure.

2. Confirm solar panels are covered Ask your insurer explicitly whether your solar panel system is included under the building definition in your policy. Some policies cover panels as standard; others require you to list them separately or increase your sum insured. Don't assume — check the Product Disclosure Statement (PDS).

3. Consider your excess carefully This policy carries a $2,000 building excess. A higher excess typically means a lower premium, but make sure you can comfortably cover that amount out of pocket if you need to make a claim. If $2,000 feels like a stretch, it may be worth comparing quotes with a lower excess to find the right balance.

4. Don't set and forget Insurance markets shift, and so do individual risk profiles. Even if this year's quote is well-priced, it's worth comparing at renewal time. Insurers sometimes offer better rates to new customers than to existing ones — so shopping around annually is a smart habit.

---

Compare Home Insurance Quotes for Your Runnymede Property

Whether you're renewing your current policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see what multiple insurers would charge for your specific property — in minutes, with no obligation.