If you own a free standing home on Russell Island in Queensland's Moreton Bay, you already know that island living comes with its own unique set of rewards — and risks. Waterfront lifestyle, lush surrounds, and a tight-knit community are part of the appeal, but insurers also weigh up factors like location, construction type, and flood or storm exposure when pricing your policy. This article breaks down a real building insurance quote for a 3-bedroom, 1-bathroom weatherboard home in Russell Island (QLD 4184), helping you understand what's driving the premium and whether the price stacks up.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote comes in at $2,981 per year (or $268/month) for building-only cover on a $438,000 sum insured. CoverClub's pricing engine rates this as CHEAP, meaning it sits meaningfully below the suburb average.

To put that in perspective:

- The suburb average for Russell Island is $4,219/yr

- The suburb median sits at $3,948/yr

- Even the 25th percentile (the cheapest quarter of quotes in the area) is $3,151/yr

This quote undercuts even the cheapest quartile of local premiums — a strong result for any homeowner. At roughly $1,238 below the suburb average, the annual saving is substantial. Over five years, that's potentially more than $6,000 kept in your pocket rather than paid to an insurer.

That said, it's always worth checking what's included. A lower premium is only good value if the cover is appropriate for your property and circumstances. Make sure the $438,000 sum insured accurately reflects what it would cost to rebuild your home from scratch, including demolition, site access costs (which can be higher on an island), and the quality of your fittings.

---

How Russell Island Compares

Russell Island sits within the Redland LGA, and the local insurance market reflects some of the pressures common across coastal and island Queensland. Here's how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,981 |

| Russell Island suburb average | $4,219 |

| Russell Island suburb median | $3,948 |

| Redland LGA average | $3,178 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. Queensland's state average of $9,129 is dramatically higher than the national average of $5,347 — a reflection of the state's exposure to cyclones, flooding, and severe storms across many regions. However, the QLD median of $3,903 tells a different story: the average is being pulled upward by very expensive premiums in high-risk areas like North Queensland. Russell Island's median of $3,948 is broadly in line with the state median, suggesting it sits in a moderate-risk band rather than an extreme one.

Compared to the national median of $2,764, Russell Island premiums do run a little higher — which is expected for an island location with additional logistical and weather-related considerations. This quote, at $2,981, is only slightly above the national median, making it genuinely competitive on a country-wide basis.

---

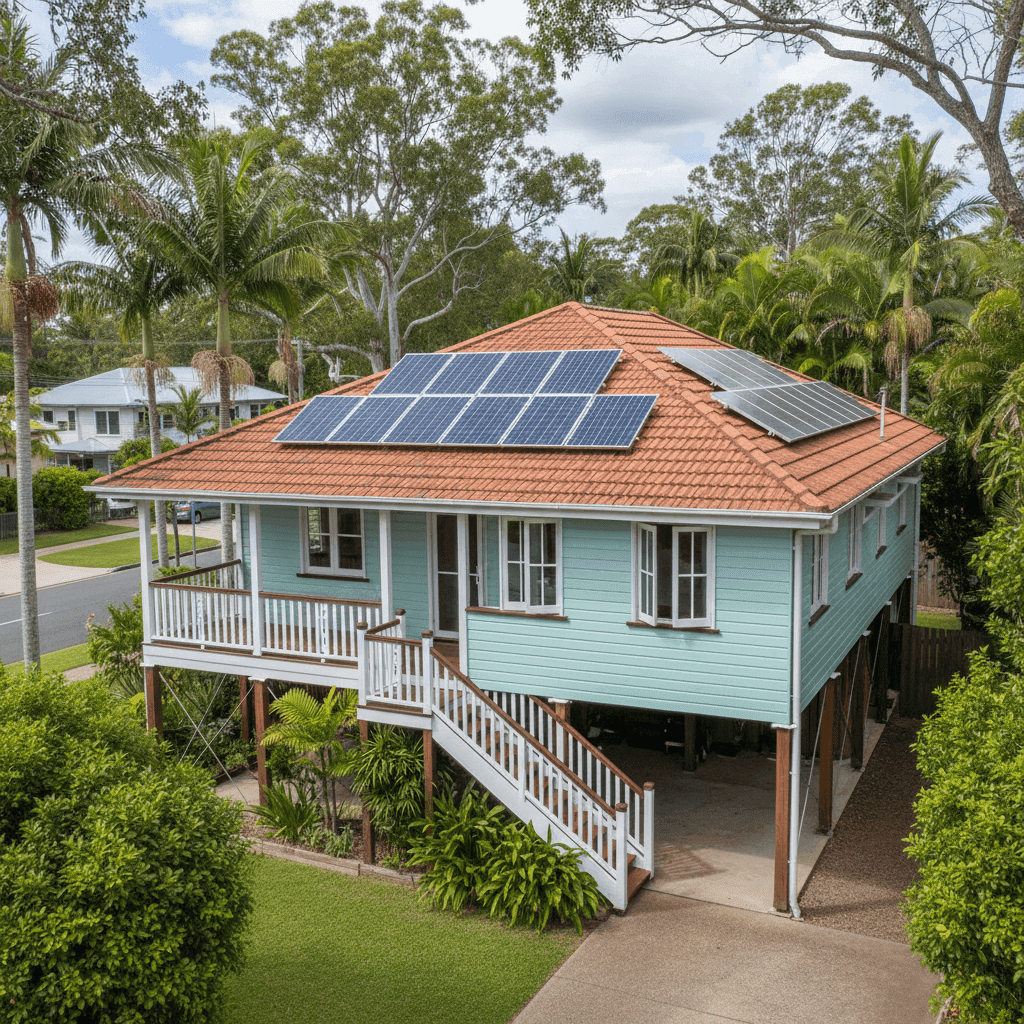

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk:

Weatherboard timber construction is one of the most significant factors. Timber-framed, weatherboard-clad homes are more susceptible to fire and moisture damage than brick veneer or brick homes, and insurers price this in. On the flip side, weatherboard homes are common across island and coastal Queensland, so local insurers are well-versed in underwriting them.

Elevated on stumps is actually a positive for flood and storm surge risk. Homes raised at least one metre off the ground are less likely to sustain inundation damage from heavy rainfall events or localised flooding — a meaningful consideration on low-lying island terrain. This elevation can help reduce premiums compared to slab-on-ground homes in the same area.

Tiled roof is generally viewed favourably by insurers. Concrete or terracotta tiles tend to be more durable and fire-resistant than Colorbond or older corrugated iron, though they can be more costly to repair after hail events.

Timber and laminate flooring can be more susceptible to water damage than tile, which is worth keeping in mind when reviewing your sum insured and excess choices.

Solar panels are present on this property. Some insurers include solar panels under building cover automatically; others treat them as an optional add-on or exclude damage caused by specific events. It's worth confirming with your insurer that your panels — and any associated inverter or battery system — are covered.

Above-average fittings quality means the cost to repair or replace internal fixtures, joinery, and finishes is higher than a standard home. This is appropriately reflected in the $438,000 sum insured and is an important reason not to underinsure.

---

Tips for Homeowners in Russell Island

1. Don't underinsure — island rebuild costs can be higher than you think Getting materials and tradespeople to Russell Island involves ferry logistics and added costs that simply don't apply on the mainland. Make sure your sum insured accounts for these access costs, not just the standard per-square-metre rebuild rate. Use a building cost calculator or speak with a local builder to get a realistic figure.

2. Review your solar panel cover explicitly Ask your insurer directly: are your solar panels covered under the building policy, and for what events? Panels can be damaged by hail, storm debris, or electrical faults. If they're not automatically included, it may be worth adding specific cover or checking whether a separate policy makes sense.

3. Revisit your policy annually The insurance market in Queensland is dynamic. Premiums, underwriting criteria, and available insurers change from year to year. A quote that's competitive today may not be the best option at renewal. Use CoverClub's comparison tool each year to check whether you're still getting a fair deal.

4. Consider your excess carefully This policy carries a $1,000 building excess. A higher excess generally lowers your premium, but make sure you can comfortably cover that amount out of pocket if you need to make a claim. Given the elevated nature of the home reduces some flood risk, a modest excess like $1,000 is a reasonable balance for most homeowners.

---

Compare Your Home Insurance Today

Whether you're a long-time Russell Island local or you've recently made the move to island life, it pays to know what you're paying — and whether you could be paying less. CoverClub makes it easy to compare building and contents insurance quotes from multiple insurers in one place.

Get a quote for your Russell Island home today and see how your current premium stacks up against the market. You might be surprised at what's out there.