Russell Island is a unique slice of South East Queensland — a bay island community in Moreton Bay that attracts sea-changers, retirees, and savvy investors drawn to its relaxed lifestyle and relatively affordable land prices. But what does it actually cost to insure a free standing home here, and how does that compare to the rest of Queensland and Australia? This article breaks down a real building insurance quote for a 3-bedroom, 2-bathroom home on Russell Island, so you can benchmark your own cover.

---

Is This Quote Fair?

The quote in question comes in at $2,578 per year (or $247/month) for building-only cover on a 3-bedroom free standing home with a sum insured of $350,000. The building excess is set at $2,000.

Based on CoverClub's pricing data, this quote is rated CHEAP — below average for the area. That's genuinely good news for the homeowner. With a suburb average of $4,219/yr and a suburb median of $3,948/yr, this quote sits well below what most Russell Island homeowners are paying for comparable cover. Even the most competitive quarter of quotes in the suburb (the 25th percentile) comes in at $3,151/yr — still $573 more expensive than this result.

In short, this is a competitive outcome. Whether you're reviewing your own renewal or shopping around for the first time, a premium like this is worth paying attention to.

---

How Russell Island Compares

To put this quote in proper context, it helps to zoom out and look at the broader insurance landscape.

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,578 |

| Russell Island suburb average | $4,219 |

| Russell Island suburb median | $3,948 |

| Russell Island 25th percentile | $3,151 |

| Russell Island 75th percentile | $4,804 |

| LGA (Redland City) average | $3,178 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

Based on 28 quotes sampled for postcode 4184. See full [Russell Island insurance statistics](https://coverclub.com.au/stats/QLD/4184/russell-island), [QLD state data](https://coverclub.com.au/stats/QLD), and [national benchmarks](https://coverclub.com.au/stats/national).

A few things stand out here. The Queensland state average of $9,129/yr looks alarming at first glance, but the median of $3,903/yr tells a more balanced story — the average is being pulled upward by high-risk areas in Far North Queensland and cyclone-prone coastal regions. Russell Island, while a bay island, is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums more manageable.

Compared to the national median of $2,764/yr, this quote is only slightly above — a reasonable position for a bay island property that carries some inherent geographic considerations.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk. Here's what matters most:

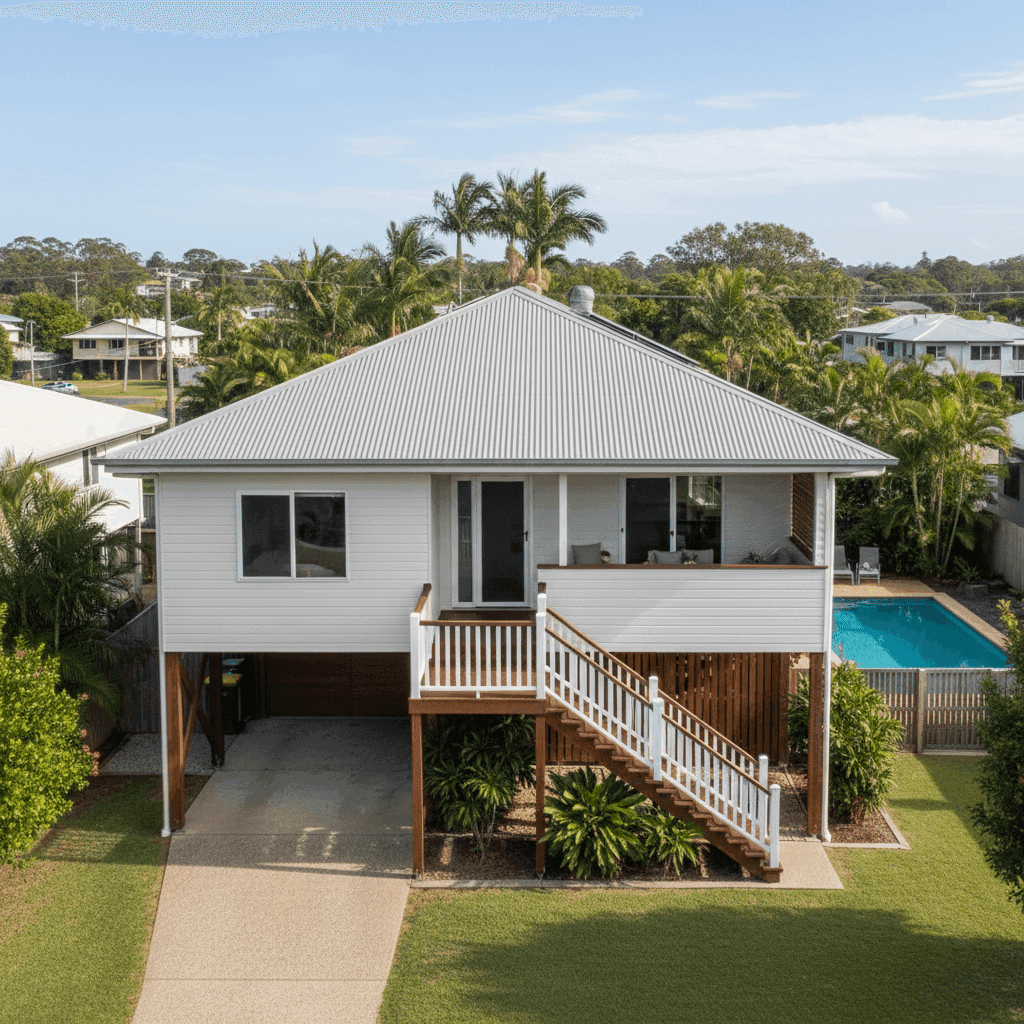

Pole Foundation

This home is built on poles — a common construction method on Russell Island, where elevated foundations help manage tidal flooding risk and sloping terrain. While pole homes can attract slightly higher premiums with some insurers due to perceived structural complexity, they also offer practical flood resilience that can work in your favour depending on the insurer's risk model.

Hardiplank/Hardiflex Cladding

The external walls are Hardiplank Hardiflex — a fibre cement cladding that's widely used across Queensland. It's regarded as durable, low-maintenance, and resistant to moisture and pests. Insurers generally view fibre cement cladding favourably compared to timber weatherboard, as it carries a lower fire and rot risk.

Steel/Colorbond Roof

A Colorbond steel roof is one of the most insurer-friendly roofing materials available in Australia. It's lightweight, durable, resistant to ember attack, and well-suited to coastal and subtropical climates. This is likely contributing positively to the competitive premium.

Swimming Pool

The property includes a pool, which adds a modest amount to the insured value and can influence liability considerations under some policies. It's worth confirming your policy covers pool-related structures (fencing, pumps, filtration equipment) under the building definition.

Ducted Climate Control

Ducted air conditioning is a fixed building feature and is typically covered under building insurance as part of the home's permanent fixtures. Its inclusion in the sum insured of $350,000 is appropriate.

Tile Flooring

Tiled flooring throughout is a practical and durable choice for a Queensland island home. It's generally viewed neutrally by insurers — neither a risk factor nor a premium driver.

No Solar Panels

The absence of solar panels simplifies the insurance picture slightly. Solar systems can add complexity around coverage (panels, inverters, wiring) and occasionally affect sum insured calculations.

---

Tips for Homeowners in Russell Island

Whether you're locked into a policy or about to renew, here are four practical steps worth taking:

1. Review your sum insured annually Building costs have risen significantly across Australia in recent years. A sum insured of $350,000 for a 130 sqm home built in 2006 may be appropriate today, but it's worth using a building cost calculator each year to confirm your cover keeps pace with reconstruction costs — not just market value.

2. Understand what "building" cover includes on a pole home On elevated/pole homes, the definition of "building" can vary between insurers. Make sure your policy clearly covers the sub-floor structure, stairs, decking, and any undercroft enclosures — not just the main dwelling above the poles.

3. Check your flood and storm surge definitions Russell Island sits within Moreton Bay, and while it's not a cyclone zone, storm tide and localised flooding are real considerations. Read your PDS carefully to understand how your insurer defines "flood" versus "storm surge" — they're not always treated the same way, and exclusions can catch homeowners off guard.

4. Compare at renewal, not just when you first buy The fact that this quote is rated "cheap" relative to the suburb average shows that meaningful price variation exists in this market. Don't assume your current insurer is still the best option at renewal time — the gap between the cheapest and most expensive quotes in Russell Island spans over $1,600/yr.

---

Compare Your Home Insurance Today

If you own a home on Russell Island — or anywhere in Queensland — it's worth knowing where your premium sits relative to your neighbours'. CoverClub makes it easy to compare building and contents insurance quotes in one place, with transparent pricing data so you can make an informed decision.

Get a home insurance quote now and see how your current premium stacks up.