Home insurance costs can vary dramatically from one suburb to the next — and even between similar properties on the same street. This article takes a close look at a real home and contents insurance quote for a four-bedroom, free standing home in Safety Bay, WA 6169, breaking down whether the premium is competitive and what factors are likely driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $3,472 per year (or $333/month) for combined home and contents cover, with a building sum insured of $919,000 and contents valued at $152,000. Both the building and contents excess are set at $500.

Our price rating for this quote is EXPENSIVE — above average for the area.

To put that in perspective, the suburb average premium in Safety Bay sits at just $1,617 per year, with a median of $1,785. Even at the upper end of the local market (the 75th percentile), most homeowners are paying around $2,213/yr — well below this quote. That means this premium is roughly 2.1× the suburb average and sits comfortably above the top quartile of local pricing.

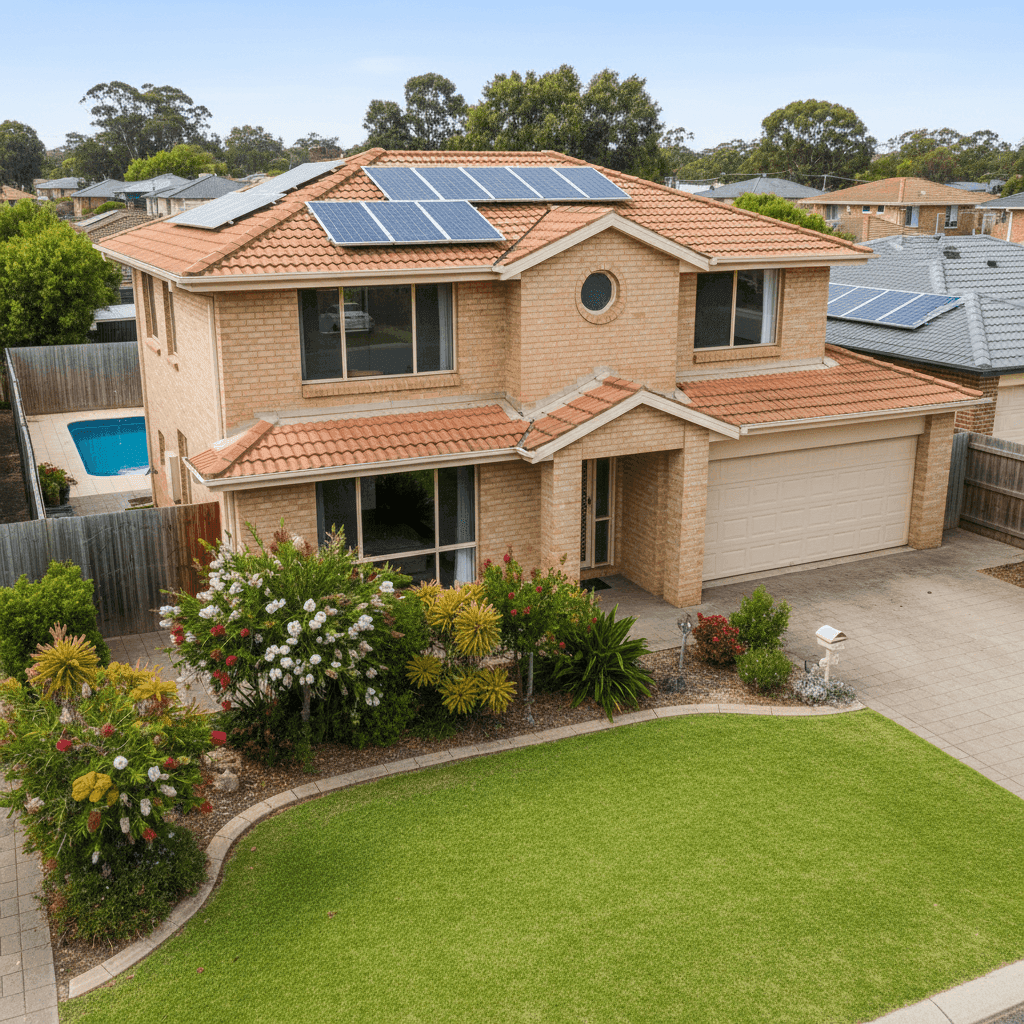

That said, it's important to consider context. This property carries a building sum insured of $919,000, which is a substantial coverage amount and likely higher than many comparable Safety Bay properties. Higher replacement values naturally push premiums up. The presence of a swimming pool, solar panels, and ducted climate control also adds to the insurer's risk exposure and replacement cost calculations.

So while the price rating is "expensive" relative to the suburb, the coverage level is also meaningfully higher than what a typical quote in this postcode might include.

---

How Safety Bay Compares

Understanding where Safety Bay sits in the broader insurance landscape helps homeowners make more informed decisions. Here's a quick snapshot:

| Benchmark | Premium |

|---|---|

| This Quote | $3,472/yr |

| Safety Bay Suburb Average | $1,617/yr |

| Safety Bay Suburb Median | $1,785/yr |

| Rockingham LGA Average | $1,561/yr |

| WA State Average | $2,811/yr |

| WA State Median | $2,127/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. Safety Bay and the broader Rockingham LGA are actually among the more affordable areas in Western Australia for home insurance — the suburb average of $1,617 is well below the WA state average of $2,811. This reflects the area's relatively low-risk profile: no cyclone zone designation, a stable coastal-suburban environment, and predominantly solid brick construction throughout the suburb.

Nationally, the picture is even more striking. According to national insurance data, the average home insurance premium across Australia is $5,347/yr, with a median of $2,764. By that measure, even this "expensive" Safety Bay quote is still below the national average — a reminder of just how wide the range of premiums can be across different regions and property types.

---

Property Features That Affect Your Premium

Several characteristics of this particular property are worth unpacking, as they directly influence what an insurer will charge.

Double Brick Construction

Built in 1985, this home features double brick external walls — one of the most robust and fire-resistant construction types available in Australia. Insurers generally view double brick favourably, as it reduces the likelihood of total loss from fire and offers strong structural integrity. This can work in the homeowner's favour when it comes to premiums.

Tiled Roof on a Slab Foundation

A tiled roof is considered a standard, durable roofing material by most insurers. Combined with a concrete slab foundation, the property sits on a solid structural base. Slab foundations are common in WA and are generally well-regarded for their resistance to subsidence and movement — particularly relevant in coastal areas like Safety Bay.

Swimming Pool

A pool is a notable premium driver. Insurers factor in the liability risk associated with pools (particularly for third parties), as well as the cost to repair or replace pool infrastructure if damaged. For a standard home and contents policy, pool inclusion can add meaningfully to the annual premium.

Solar Panels

With solar panels installed, the building sum insured needs to account for the replacement cost of the system — which can run into the tens of thousands of dollars. Most insurers cover rooftop solar as part of the building, so a higher sum insured is appropriate and expected here.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and require specialist installation. Their inclusion in the building's replacement cost is another factor that supports the higher sum insured — and by extension, the higher premium.

Timber and Laminate Flooring

While not a major premium driver on its own, timber and laminate flooring can be more costly to replace than carpet, and this is typically factored into contents or building calculations depending on the policy.

---

Tips for Homeowners in Safety Bay

If you're a homeowner in Safety Bay looking to get better value from your home insurance, here are some practical steps worth considering:

- Review your sum insured carefully. A building sum insured of $919,000 is significant. Make sure this figure reflects the actual rebuild cost of your home — not its market value. Overcovering can push premiums up unnecessarily, while undercovering leaves you exposed. Tools like the Cordell Sum Sure calculator can help you estimate an accurate rebuild cost.

- Compare multiple quotes before renewing. With only 20 quotes in our Safety Bay sample, the local market data is still developing — but the spread between the 25th percentile ($1,147/yr) and the 75th percentile ($2,213/yr) shows there's real variation between insurers for similar properties. Shopping around can make a significant difference.

- Ask about bundling discounts. Some insurers offer reduced premiums when you combine home and contents cover (as this policy does) or when you hold multiple policies with the same provider. It's always worth asking.

- Consider your excess level. Both the building and contents excess on this policy are set at $500. Opting for a higher excess — say $1,000 or $2,500 — can reduce your annual premium, provided you're comfortable covering that amount out of pocket in the event of a claim.

---

Compare Your Home Insurance with CoverClub

Whether you're renewing your existing policy or shopping for cover on a new property, it pays to compare. CoverClub helps Australian homeowners see how their premiums stack up against real data from their suburb, state, and across the country. Get a quote today and find out if you're paying a fair price — or leaving money on the table.