If you own a free standing home in Saint Clair, NSW 2759, you're likely paying close attention to the rising cost of home insurance. This article breaks down a real home and contents insurance quote for a five-bedroom brick veneer property in the suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $2,033 per year (or $195/month) for combined home and contents insurance, covering a building sum insured of $800,000 and contents valued at $50,000, each with a $1,000 excess.

Our pricing analysis rates this quote as Expensive — above average for the area.

To put that in perspective, the suburb average premium for Saint Clair sits at $1,657 per year, with a median of $1,552. This quote lands well above both figures — roughly 23% above the suburb average and 31% above the median. It also sits just above the 75th percentile for the suburb ($2,000/yr), meaning fewer than one in four comparable quotes in the area cost more.

That said, context matters. A $800,000 building sum insured is a significant coverage amount, and the property's features — including its size and solar panel installation — can push premiums upward. The question isn't just whether the premium is high, but whether the level of cover justifies the cost. Based on the data, there is likely room to shop around.

---

How Saint Clair Compares

Understanding where Saint Clair sits within the broader insurance landscape helps put this quote in context. Here's a snapshot based on data from CoverClub's Saint Clair suburb stats:

| Benchmark | Premium |

|---|---|

| This quote | $2,033/yr |

| Saint Clair suburb average | $1,657/yr |

| Saint Clair suburb median | $1,552/yr |

| Saint Clair 25th percentile | $1,209/yr |

| Saint Clair 75th percentile | $2,000/yr |

| Penrith LGA average | $2,220/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 66 quotes sampled for the Saint Clair area.)

One of the most striking figures here is the NSW state average of $9,528 per year — an extraordinary number driven by high-risk coastal, flood-prone, and cyclone-affected regions across the state. The NSW state insurance data reflects the enormous variability in premiums across New South Wales. When compared to the national average of $5,347, Saint Clair homeowners are actually in a relatively favourable position overall.

The Penrith LGA average of $2,220 per year is also worth noting — this quote sits below the broader local government area average, which suggests that Saint Clair itself is a comparatively lower-risk pocket within the Penrith region.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers price the risk. Here's what's at play:

Brick Veneer Walls & Tiled Roof

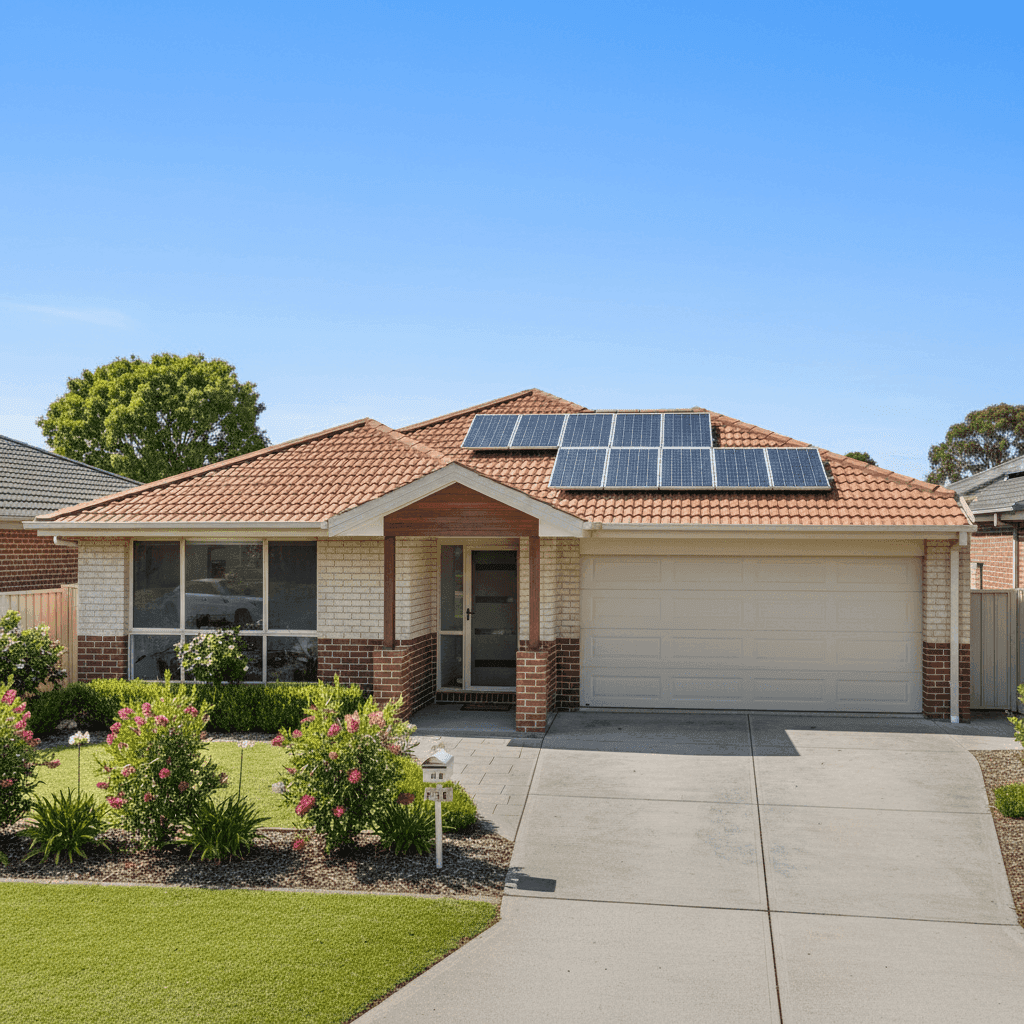

Brick veneer construction with a tiled roof is generally viewed favourably by insurers. These materials offer solid fire resistance and durability, which can help moderate premiums compared to properties with timber cladding or metal roofing. Built in 2005, the home is also relatively modern, meaning it's likely to comply with contemporary building codes — another positive signal for underwriters.

Slab Foundation

A concrete slab foundation is common in Western Sydney and is generally considered a stable, low-risk base. It reduces exposure to certain subsidence or underfloor moisture issues that can affect older homes on stumps or piers.

Timber & Laminate Flooring

While attractive, timber and laminate flooring can be more costly to repair or replace after a water damage event compared to tiles. This can nudge contents and building replacement estimates slightly higher.

Solar Panels

The presence of solar panels adds replacement value to the building and introduces a small element of additional risk (e.g., fire risk from faulty inverters or panels). Insurers factor this into their assessments, and it's important to ensure your building sum insured adequately accounts for the cost of replacing your solar system.

Building Size: 214 sqm

At 214 square metres, this is a sizeable home. Larger floor areas directly increase the estimated cost to rebuild, which in turn supports a higher building sum insured — and a higher premium. Ensuring your sum insured accurately reflects current construction costs in Western Sydney is essential to avoid being underinsured.

Standard Fittings

Standard-quality fittings keep replacement costs predictable and generally don't attract the premium loading that high-end or bespoke finishes might.

---

Tips for Homeowners in Saint Clair

1. Review Your Building Sum Insured Annually

Construction costs in Greater Western Sydney have risen significantly in recent years. Make sure your $800,000 building sum insured still reflects the true cost of rebuilding your home from scratch — not just its market value. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Shop Around — Especially Above the 75th Percentile

At $2,033/yr, this quote sits above the 75th percentile for Saint Clair. That's a strong signal to compare. Different insurers weigh risk factors differently, and even modest differences in how they assess your solar panels, floor area, or construction type can translate to hundreds of dollars in savings.

3. Consider a Higher Excess to Reduce Your Premium

Both the building and contents excesses are set at $1,000. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, increasing your excess to $2,000 or more can meaningfully reduce your annual premium.

4. Confirm Your Solar Panels Are Properly Listed

Many homeowners assume solar panels are automatically covered under their building policy — but coverage terms vary. Check with your insurer that your panels are explicitly included in your building sum insured and that the listed value is up to date, particularly if you've upgraded your system.

---

Compare Home Insurance Quotes in Saint Clair

Whether you're renewing your current policy or shopping for the first time, it pays to compare. CoverClub makes it easy to see how your premium stacks up and find competitive quotes tailored to your property. Get a home insurance quote today and make sure you're not paying more than you should for the cover your home deserves.