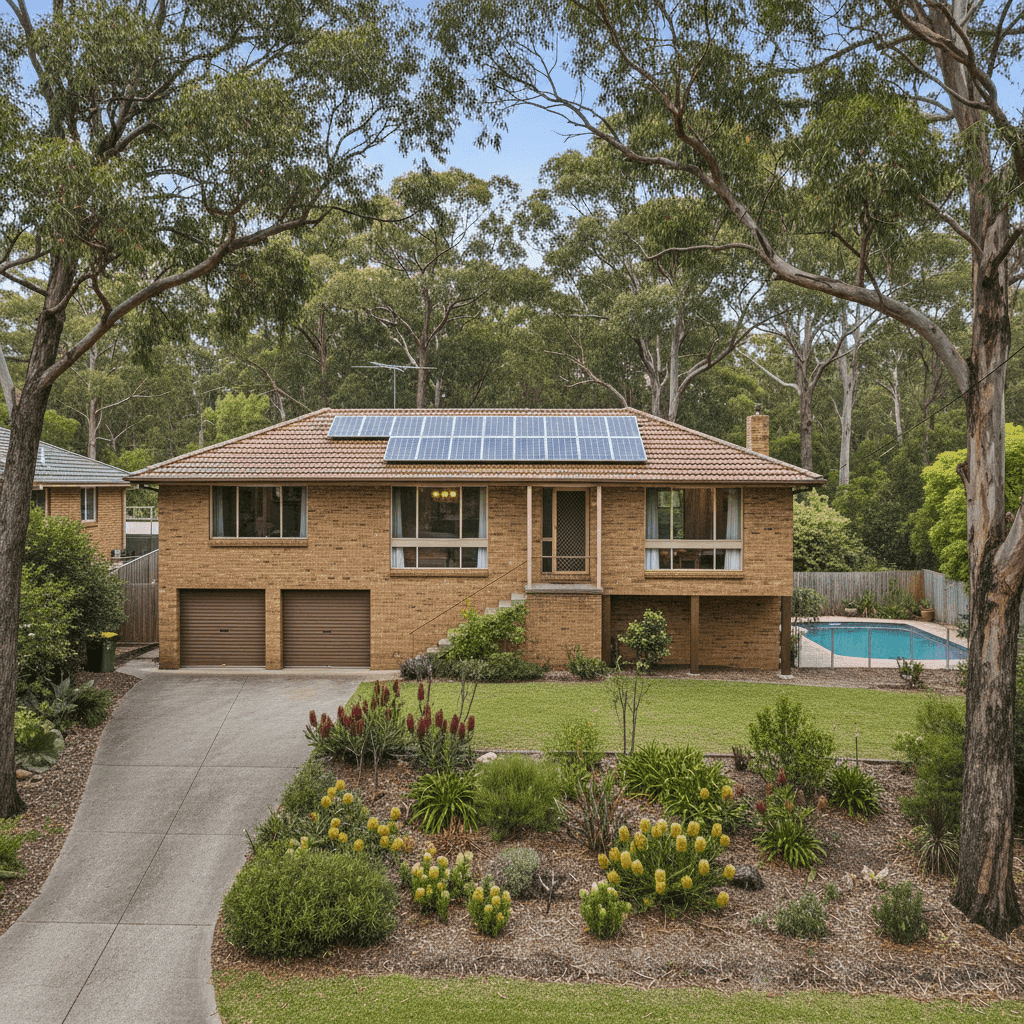

Saint Ives Chase is a leafy, well-established suburb on Sydney's Upper North Shore, known for its bushland surroundings, generous block sizes, and solid family homes. If you own a free standing home in this pocket of the Northern Beaches LGA, you're likely paying a premium that reflects both the high property values in the area and the unique risks that come with living close to native bushland. This article takes a close look at a recent home and contents insurance quote for a four-bedroom, three-bathroom brick veneer home in Saint Ives Chase — and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The quote in question comes in at $3,729 per year (or $357/month) for a combined home and contents policy, covering a building sum insured of $1,000,000 and contents valued at $50,000, each with a $1,000 excess.

Our analysis rates this quote as Expensive — above average for the suburb. Here's what that means in context:

- The suburb average for Saint Ives Chase is $3,495/yr, and the median sits at $3,491/yr

- This quote lands above the 75th percentile ($3,674/yr), meaning it's pricier than at least three-quarters of comparable quotes in the area

- The 25th percentile is $3,316/yr — so there's a meaningful spread of around $400 between the most competitive and least competitive quotes in this suburb

In short: while this isn't an outrageous figure for a well-appointed home in a bushfire-prone suburb, there's a reasonable chance a more competitive quote exists. Shopping around is well worth the effort.

---

How Saint Ives Chase Compares

Understanding where your suburb sits relative to broader benchmarks can be genuinely eye-opening. Here's how Saint Ives Chase stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Saint Ives Chase (2075) | $3,495/yr | $3,491/yr |

| Northern Beaches LGA | $3,266/yr | — |

| NSW | $9,528/yr (avg) | $3,770/yr |

| National | $5,347/yr (avg) | $2,764/yr |

A few things stand out here. The NSW state average of $9,528/yr looks alarming at first glance, but the median of $3,770/yr tells a more grounded story — a small number of very high-risk properties (think flood zones, extreme bushfire zones, and coastal storm-surge areas) pull that average up significantly. The national picture is similar, with a median of $2,764/yr versus an average of $5,347/yr.

Compared to the Northern Beaches LGA average of $3,266/yr, Saint Ives Chase premiums run slightly higher — which makes sense given the suburb's bushland interface and the higher rebuild costs associated with larger, older homes in the area.

You can explore the full data for this suburb at our Saint Ives Chase insurance stats page, compare it against all NSW suburbs, or see how it measures up on the national insurance stats page.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a detailed picture of your property. Here are the key features of this particular home and how they likely influence the premium:

Brick Veneer Walls & Tiled Roof

Brick veneer construction with a tiled roof is a very common combination in Sydney's suburbs, and insurers generally view it favourably. Both materials offer solid fire resistance and durability compared to timber cladding or metal roofing, which can work in your favour at pricing time.

Built in 1975

Homes from this era are well past their mid-century mark, meaning certain systems — electrical wiring, plumbing, and roofing underlays — may be ageing. Insurers factor in the age of a home when calculating rebuild risk and potential claims frequency, so older homes can attract slightly higher premiums than newer builds.

Stump Foundation & Timber/Laminate Flooring

The home sits on stumps and is elevated by less than one metre. This style of construction is common in older Sydney homes and can increase susceptibility to subfloor moisture and pest damage, both of which are considerations for insurers. Timber and laminate flooring, while attractive, can also be more costly to replace than concrete or tile in a claim scenario.

Swimming Pool

A pool adds to the replacement cost of the property and introduces additional liability considerations. Most insurers will factor this into the building sum insured, so it's important that your coverage reflects the true cost of reinstating the pool and its associated equipment.

Solar Panels

Solar panels are now a standard feature on many Australian homes, but they do add to the overall replacement value of the building. Make sure your building sum insured accounts for the full reinstallation cost of your solar system — a figure that can easily reach $10,000–$20,000 for a quality setup.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and are typically covered under the building sum insured. This is another feature that reinforces the importance of having an adequate — not just a minimum — building sum insured.

Bushfire Proximity

Saint Ives Chase is bordered by national park and bushland reserves, placing many properties in or near bushfire attack level (BAL) zones. This is one of the most significant premium drivers in the suburb and is likely contributing to the above-average cost of this quote.

---

Tips for Homeowners in Saint Ives Chase

1. Review Your Building Sum Insured Carefully

At $1,000,000, the building sum insured for this property is substantial — but it needs to reflect the actual cost to rebuild, not the market value of the land. Given the home's size (214 sqm), age, pool, solar panels, and ducted systems, it's worth using a quantity surveyor or an online rebuild cost calculator to verify this figure annually.

2. Shop Around — The Market Has Real Variation

With a 25th-to-75th percentile spread of around $360/yr in this suburb alone, there's genuine price variation between insurers. Using a comparison platform like CoverClub to run multiple quotes side by side takes minutes and could save you hundreds of dollars a year.

3. Ask About Bushfire Mitigation Discounts

Some insurers offer premium reductions for homeowners who take active steps to reduce bushfire risk — such as maintaining a defendable space, installing ember guards on vents, or using fire-resistant materials in renovations. It's worth asking your insurer directly whether any mitigation measures you've taken are recognised in your premium.

4. Consider a Higher Excess to Lower Your Premium

The current policy carries a $1,000 excess on both building and contents. If you have the financial capacity to absorb a higher out-of-pocket cost in the event of a claim, opting for a $2,000 or $2,500 excess can meaningfully reduce your annual premium. Just make sure the savings over time genuinely outweigh the increased risk you're taking on.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're not overpaying. Head to CoverClub to get a personalised home and contents insurance quote for your Saint Ives Chase property — it's fast, free, and gives you real market data to make a confident decision.