If you own a free standing home in Saint Marys, Tasmania (7215), you're likely curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is worth accepting. Saint Marys is a quiet rural township nestled in Tasmania's Break O'Day region, known for its relaxed pace, heritage character, and proximity to the stunning east coast. Like many regional Tasmanian properties, homes here tend to be older, well-built, and increasingly attracting the attention of tree-changers and lifestyle buyers.

This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom free standing home in Saint Marys, comparing it against local, state, and national benchmarks so you can make a more informed decision.

---

Is This Quote Fair?

The short answer: yes — and then some.

This quote comes in at $2,184 per year (or $195/month) for combined home and contents cover, with a $547,000 building sum insured and $100,000 in contents. CoverClub's pricing analysis rates this quote as CHEAP — below average for the area, which is a strong outcome for any homeowner.

To put it in perspective, the Tasmanian state average sits at $2,814 per year, with a median of $2,326/yr. This quote beats even the median by roughly $142 annually — meaning more than half of Tasmanian homeowners are paying more for their cover. Nationally, the picture is even starker: the national average is a hefty $5,347/yr, with a median of $2,764/yr. By that measure, this Saint Marys homeowner is paying less than half the national average.

For a property with above-average fittings, solar panels, ducted climate control, and a reasonably generous sum insured, landing a premium this competitive is genuinely good news.

---

How Saint Marys Compares

While suburb-level data isn't available for Saint Marys specifically, we can draw useful comparisons from broader benchmarks. You can explore available Saint Marys suburb stats here.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,184 |

| LGA (Northern Midlands) Average | $2,528 |

| TAS State Average | $2,814 |

| TAS State Median | $2,326 |

| National Average | $5,347 |

| National Median | $2,764 |

This quote sits $344 below the LGA average and $630 below the state average. Against the national average, the saving is a remarkable $3,163 per year — though it's worth noting that national figures are heavily skewed by high-risk areas in Queensland and Western Australia prone to cyclones, floods, and bushfires.

Tasmania generally enjoys lower premiums than the mainland, thanks to its more temperate climate and lower exposure to extreme weather events like cyclones and major flooding. Saint Marys, in particular, is not classified as a cyclone risk area, which keeps premiums more manageable.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour — and a few are worth keeping an eye on.

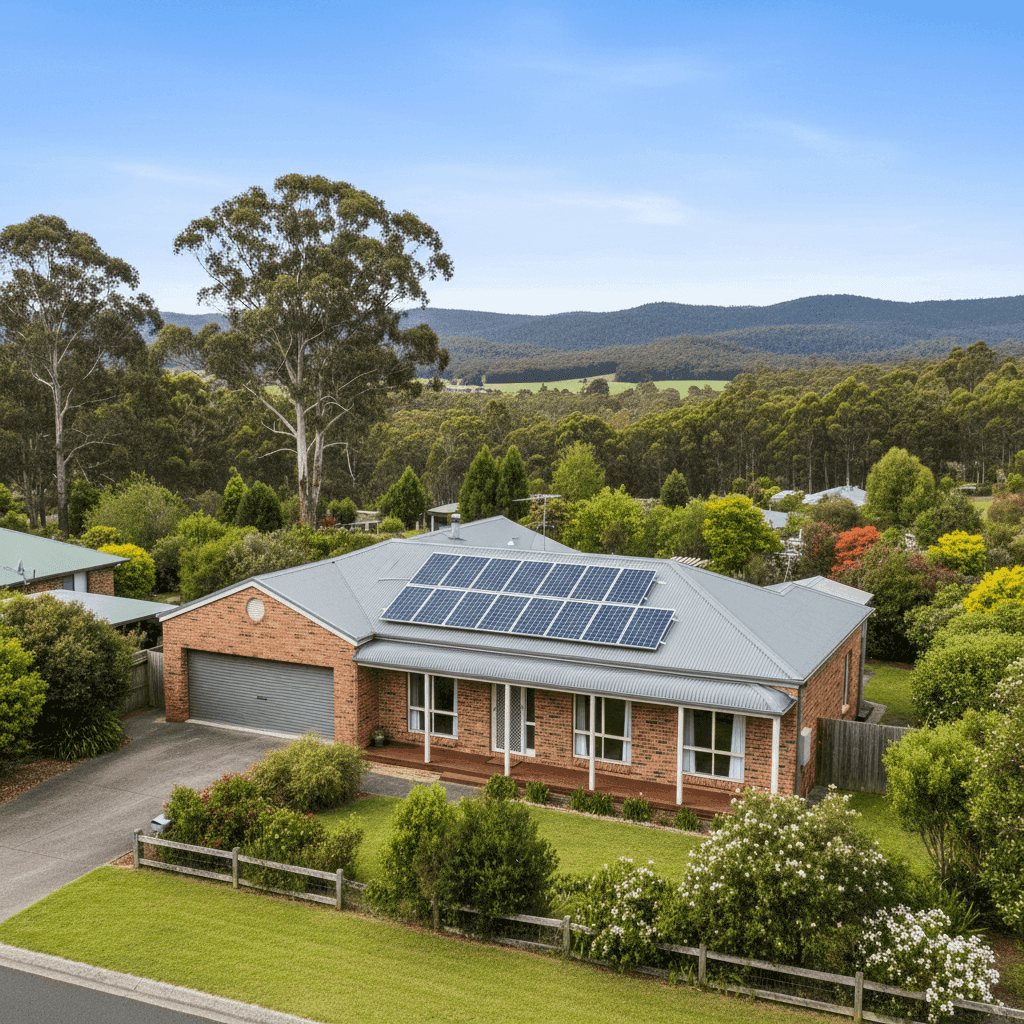

Brick Veneer Walls & Colorbond Roof

Brick veneer is one of the more insurer-friendly wall types. It offers solid fire resistance and structural durability, which typically translates to lower premiums compared to weatherboard or timber-clad homes. The steel Colorbond roof is similarly well-regarded — it's lightweight, durable, resistant to corrosion, and performs well in high-wind conditions.

Stump Foundation

The home sits on stumps, which is common for properties of this era (built in 1973) in Tasmania. While stumps can introduce some risk around subsidence or pest damage over time, well-maintained stump foundations are generally accepted by insurers without significant loading. It's worth having the stumps inspected periodically, particularly for older properties.

Timber and Laminate Flooring

Timber floors add character and value, but they can be more costly to repair or replace than concrete or tile. This is reflected in the contents and building sum insured, and it's one reason ensuring your building cover is adequate is so important.

Solar Panels

This property has solar panels, which are typically covered under building insurance as a fixed structure. It's worth confirming with your insurer that your sum insured accounts for the replacement cost of the panels — a full rooftop system can add $8,000–$15,000 or more to your rebuild cost.

Ducted Climate Control

Ducted heating and cooling systems are a significant fixed asset. Like solar panels, these should be factored into your building sum insured to avoid being underinsured in the event of a total loss.

Above-Average Fittings

The property features above-average quality fittings, which means fixtures, appliances, and finishes are likely of higher specification than a standard home. This is appropriately reflected in the $547,000 building sum insured — a figure that should be reviewed annually to keep pace with rising construction costs.

---

Tips for Homeowners in Saint Marys

1. Review your sum insured every year Construction costs in Tasmania have risen significantly in recent years. A sum insured set even two or three years ago may no longer reflect the true cost of rebuilding your home from scratch. Use a building cost calculator or speak with a local builder to sense-check your figure annually.

2. Confirm solar panels and ducted systems are included Not all policies automatically include solar panels or ducted HVAC systems in the building definition. Read your Product Disclosure Statement (PDS) carefully and ask your insurer directly if you're unsure.

3. Get your stumps inspected For homes built in the 1970s on stump foundations, a periodic inspection by a licensed building inspector is a smart move. Rotting or shifting stumps can lead to structural issues that may complicate insurance claims if pre-existing damage is found.

4. Compare at renewal time Even if you're happy with your current premium, it pays to compare quotes at renewal. Insurers regularly re-price their books, and a policy that was competitive last year may not be the best value this year. Platforms like CoverClub make it easy to see what else is available for your specific property.

---

Ready to Compare?

Whether you're reviewing an existing policy or shopping for cover for the first time, it's always worth seeing what the market has to offer. At CoverClub, you can compare home and contents insurance quotes tailored to your property in Saint Marys — quickly, easily, and at no cost. Get a quote today and make sure you're getting the right cover at the right price.