If you own a large free standing home in Samford Valley, QLD 4520, you already know this leafy semi-rural suburb offers a lifestyle that's hard to beat — rolling hills, acreage blocks, and a tight-knit community just 30 minutes from Brisbane's CBD. But with that lifestyle comes the responsibility of adequately protecting what is likely your most valuable asset. This article breaks down a real building insurance quote for a substantial six-bedroom home in Samford Valley and puts the numbers in context so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question is $2,495 per year (or $241 per month) for building-only cover on a 363 sqm, six-bedroom, five-bathroom brick veneer home built in 2012, with a sum insured of $1,194,000 and a building excess of $5,000.

Our price rating for this quote is CHEAP — below average for the area. That's a strong result for the homeowner. To put it plainly: this premium sits well below what most comparable properties in Samford Valley are paying, and it's a meaningful saving worth understanding.

The $5,000 building excess is on the higher end of the spectrum, which is one factor that helps bring the annual premium down. Choosing a higher excess is a legitimate strategy to reduce ongoing costs — provided you're comfortable covering that amount out of pocket in the event of a claim. For a home of this size and value, many owners are willing to make that trade-off.

---

How Samford Valley Compares

To appreciate just how competitive this quote is, it helps to look at the broader data. Based on quotes collected for Samford Valley (postcode 4520):

| Benchmark | Premium |

|---|---|

| This quote | $2,495/yr |

| Suburb 25th percentile | $3,550/yr |

| Suburb average | $5,106/yr |

| Suburb median | $5,205/yr |

| Suburb 75th percentile | $6,103/yr |

This quote comes in 51% below the suburb average and sits beneath even the cheapest quarter of quotes collected locally. That's a significant gap — the difference between this premium and the suburb average is over $2,600 per year, or more than $200 per month.

Zooming out to the state level, the picture becomes even more striking. Queensland's average home insurance premium sits at $9,129 per year, driven upward by high-risk coastal and cyclone-prone regions in North Queensland. The QLD median, however, is a more moderate $3,903 — still well above this quote. Samford Valley itself is not classified as a cyclone risk area, which is a significant factor keeping premiums lower than much of regional Queensland.

At a national level, the average premium across Australia is $5,347/yr, with a median of $2,764/yr. This quote lands just above the national median — a reasonable outcome for a large, high-value home.

It's also worth noting that the LGA average for Brisbane is a striking $16,277/yr, heavily skewed by flood-affected and high-risk suburbs within the broader Brisbane council area. Samford Valley, while technically part of the Moreton Bay region historically, benefits from its elevated terrain and lower flood exposure compared to many Brisbane suburbs.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an insurance pricing perspective:

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to weatherboard or lightweight cladding, which can translate to lower premiums or better claim outcomes.

Tiled roof is another positive. Concrete or terracotta tiles are durable, long-lasting, and perform well in storms — a key consideration in South East Queensland where severe hail and wind events are not uncommon.

Slab foundation is the most common and straightforward foundation type for insurers to assess. It carries fewer complexities than raised timber stumps, which can be susceptible to movement or pest damage.

No cyclone risk is a major pricing factor. Properties in North Queensland's cyclone belt can attract enormous premiums. Samford Valley's inland, elevated position keeps it out of this category entirely.

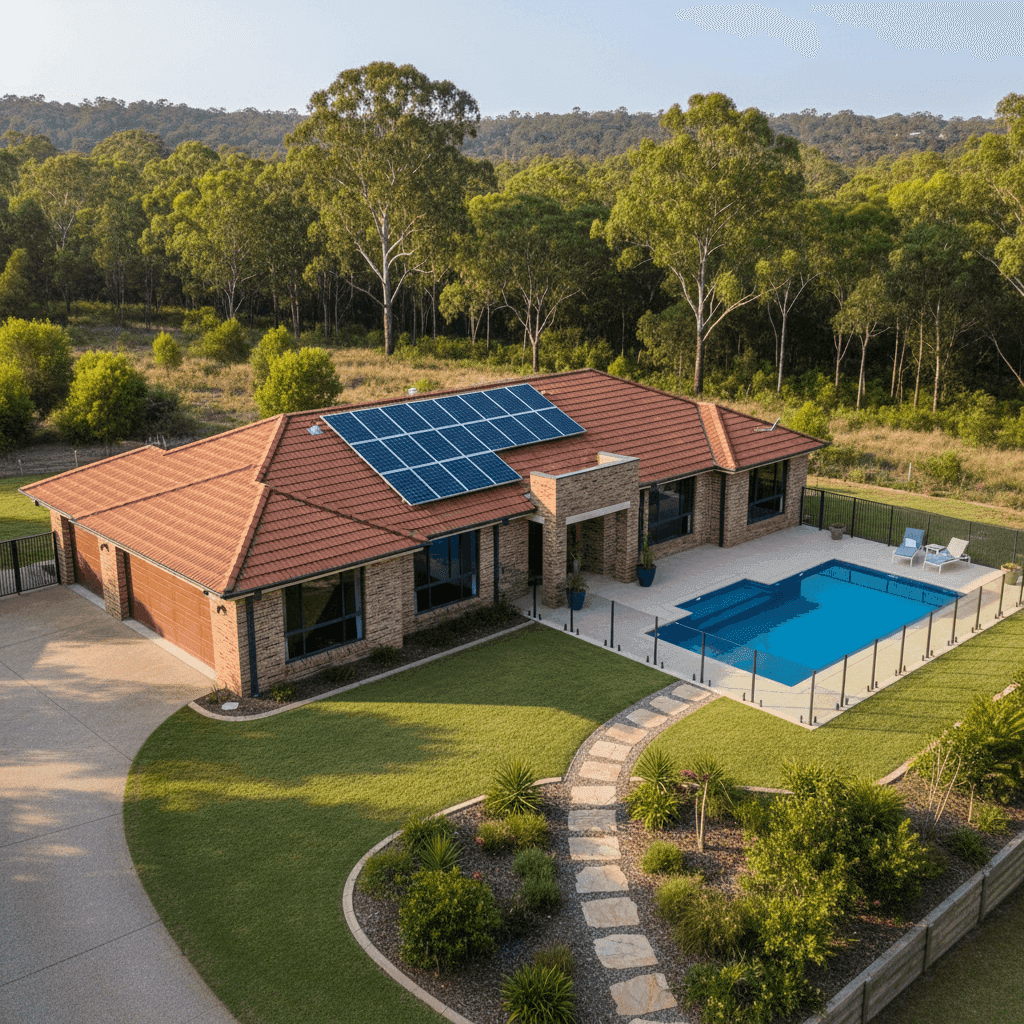

Solar panels and a pool are worth flagging. Solar panels add replacement value to your building sum insured — it's important to confirm they are included in your $1,194,000 building cover figure. Pools similarly need to be factored into your sum insured, as the structure itself (including fencing, pumps, and filtration) can cost tens of thousands of dollars to repair or replace.

Ducted climate control is another high-value fixed asset. Ducted systems are expensive to replace, and as a fixed installation, they should be covered under your building policy. It's worth verifying this with your insurer.

Standard fittings quality keeps the replacement cost estimate grounded. Homes with high-end or bespoke finishes — custom joinery, imported tiles, luxury appliances — can see their true rebuild cost exceed initial estimates. Standard fittings make it easier to model an accurate sum insured.

---

Tips for Homeowners in Samford Valley

1. Review your sum insured annually At $1,194,000 for a 363 sqm home built to a standard finish, this sum insured works out to roughly $3,289 per sqm — a reasonable estimate for South East Queensland. However, construction costs have risen sharply in recent years. It's worth revisiting this figure each renewal to ensure you're not underinsured, particularly given the cost of labour and materials post-pandemic.

2. Confirm solar panels and pool are included As noted above, both solar panels and your pool structure should be explicitly covered under your building policy. Check your Product Disclosure Statement (PDS) to confirm this, and ensure their replacement value is reflected in your sum insured.

3. Consider whether your excess suits your situation A $5,000 building excess is a meaningful cost in the event of a claim. While it helps reduce your annual premium, make sure you have accessible savings to cover it if needed. If your financial position changes, it may be worth comparing quotes with a lower excess to find the right balance.

4. Compare at renewal — don't auto-renew The fact that this quote is rated cheap relative to the suburb average is a reminder that premiums vary significantly between insurers. Loyalty doesn't always pay in home insurance. Using a comparison platform like CoverClub at renewal time takes only minutes and can surface meaningful savings.

---

Get Your Own Quote

Whether you're a Samford Valley local or researching home insurance anywhere in Australia, comparing quotes is the single most effective way to avoid overpaying. CoverClub makes it easy to see real premiums side by side, so you always know where you stand. Get a personalised home insurance quote today and find out if your current cover is as competitive as it could be.