If you own a free standing home in San Isidore, NSW 2650, you're probably wondering whether your home insurance premium is competitive — or whether you're quietly overpaying year after year. This article breaks down a real building insurance quote for a four-bedroom, two-bathroom brick veneer home in the area, and compares it against suburb, state, and national benchmarks to give you a clear picture of where you stand.

---

Is This Quote Fair?

The quote in question comes in at $1,377 per year (or roughly $127 per month) for building-only cover on a home with a sum insured of $759,000. Our pricing engine rates this as CHEAP — below average for the area.

To put that in perspective, the suburb average for San Isidore sits at $2,539 per year, meaning this quote is saving the homeowner approximately $1,162 annually compared to what many locals are paying. That's a meaningful difference — enough to cover a weekend away or a few months of groceries.

A below-average rating doesn't mean the cover is inferior. It simply means the insurer has assessed the specific risk profile of this property favourably. Several factors — including the relatively modern construction date, the robust materials used, and the low-risk location characteristics — likely contribute to the competitive pricing.

One thing worth noting: the building excess on this policy is $5,000, which is on the higher side. A higher excess typically reduces the annual premium, so part of the reason this quote looks attractive is that the homeowner is accepting more out-of-pocket cost in the event of a claim. Before celebrating the low premium, make sure you're comfortable with that excess level.

---

How San Isidore Compares

Understanding your premium in isolation only tells half the story. Here's how the San Isidore market stacks up against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,377 |

| Suburb Average (San Isidore) | $2,539 |

| Suburb Median | $2,480 |

| Suburb 25th Percentile | $2,161 |

| LGA Average (Narrandera) | $3,013 |

| NSW State Average | $3,801 |

| NSW State Median | $3,410 |

| National Average | $2,965 |

| National Median | $2,716 |

A few things stand out here. First, this quote sits well below even the 25th percentile for the suburb ($2,161), meaning it's cheaper than at least 75% of quotes recorded in the area. Second, NSW premiums as a whole are notably elevated — the state average of $3,801 is significantly higher than the national average of $2,965, reflecting the diverse range of risk profiles across the state, from coastal flood zones to bushfire-prone regions.

Interestingly, San Isidore's local suburb average of $2,539 is actually below both the NSW state average and the national average, suggesting the suburb itself carries a relatively moderate risk profile compared to many other parts of New South Wales. That context makes this quote — already well below the suburb average — even more impressive.

---

Property Features That Affect Your Premium

Insurers assess dozens of variables when pricing a home insurance policy. For this particular property, several features work in the homeowner's favour:

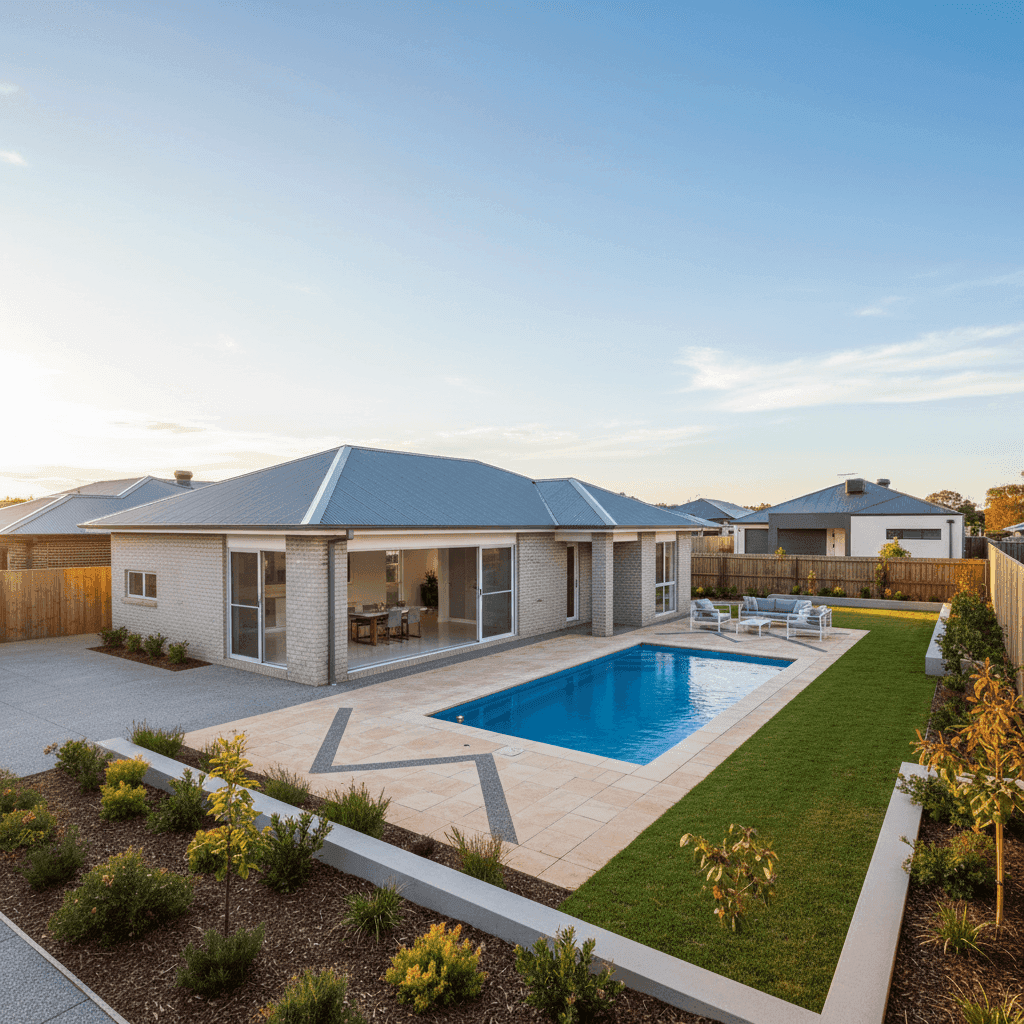

Modern Construction (2019) Homes built in the last decade benefit from current building codes, improved fire resistance standards, and modern electrical and plumbing systems. Insurers generally view newer builds as lower risk, which can translate directly to lower premiums.

Brick Veneer Walls & Colorbond Roof Brick veneer is one of the most common and well-regarded wall materials in Australian residential construction. It offers solid fire resistance and durability. Paired with a steel Colorbond roof — known for its longevity, wind resistance, and low maintenance — this combination is typically viewed favourably by underwriters.

Concrete Slab Foundation A slab foundation is generally considered stable and less susceptible to certain structural issues compared to older stumped or raised foundations. It's a tick in the box for most insurers.

Tile Flooring Tiled floors are durable, moisture-resistant, and relatively straightforward to repair or replace. They don't carry the same risk profile as, say, solid hardwood or carpet in terms of water or fire damage.

Swimming Pool A pool does add a layer of liability and maintenance risk to a property. Some insurers factor this into building premiums, particularly around the structural elements of the pool itself. It's worth confirming what your policy covers in relation to pool damage and any associated liability.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset. While they add to the overall rebuild value — and therefore the sum insured — they're generally not a major risk flag for insurers. Just ensure your sum insured adequately accounts for the replacement cost of the system.

No Cyclone Risk San Isidore is not in a designated cyclone risk zone, which removes one of the more significant premium loading factors that affect homeowners in northern parts of Australia. This contributes to the comparatively moderate pricing in the suburb.

---

Tips for Homeowners in San Isidore

1. Review Your Sum Insured Annually With a sum insured of $759,000 on a 214 sqm home built in 2019 with standard fittings, it's important to ensure this figure accurately reflects the current cost to rebuild — not the market value. Construction costs have risen considerably in recent years. Use a building calculator or speak to a quantity surveyor to validate your figure.

2. Weigh Up Your Excess Carefully The $5,000 building excess on this policy is high. While it lowers the annual premium, consider whether you could comfortably cover that amount if you needed to make a claim. If cash flow is a concern, it may be worth comparing policies with a lower excess, even if the annual premium is slightly higher.

3. Shop Around at Renewal Time Even if your current premium is competitive, insurers often increase premiums at renewal without significant justification. Make it a habit to compare quotes each year — it takes minutes and could save you hundreds.

4. Don't Forget Pool Maintenance Documentation If your insurer requires the pool to meet certain safety standards (fencing, filtration, etc.), keep records of maintenance and compliance. Some claims can be complicated or reduced if a pool is found to be non-compliant at the time of an incident.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for cover for the first time, it pays to see what's available across the market. Get a home insurance quote at CoverClub and see how your premium stacks up against other San Isidore homeowners — in just a few minutes, you'll know whether you're getting a fair deal or leaving money on the table.