If you own a four-bedroom free standing home in San Remo, WA 6210, you're likely paying close attention to the rising cost of home insurance. This article breaks down a real home and contents insurance quote for a property in this suburb, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes to $3,047 per year (or around $292 per month) for combined home and contents cover, with a building sum insured of $952,000 and $100,000 in contents cover. Both the building and contents excess are set at $2,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for San Remo sits at $2,775 per year, meaning this quote lands about 10% above the local average. That's not a red flag — a number of property-specific factors (more on those below) can reasonably push a premium higher than the suburb norm. What it does tell us is that there may be room to shop around without sacrificing cover quality.

It's also worth noting that the spread of premiums in this suburb is quite wide. The 25th percentile sits at just $1,158 per year, while the 75th percentile reaches $3,468 per year. This quote falls comfortably within that upper band, suggesting it's a competitive — if not exceptional — result for a property of this size and specification.

---

How San Remo Compares

To put this quote in proper context, here's how San Remo stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| San Remo (6210) | $2,775/yr | $2,781/yr |

| Western Australia | $2,811/yr | $2,127/yr |

| National | $5,347/yr | $2,764/yr |

| LGA (Mandurah) | $1,732/yr | — |

A few things stand out here. First, San Remo's average and median premiums are remarkably close to each other ($2,775 vs $2,781), which suggests a relatively consistent pricing environment in the suburb — there aren't many extreme outliers dragging the average up or down. You can explore the full San Remo suburb insurance statistics on CoverClub.

Second, the LGA average for Mandurah is notably lower at $1,732 per year, which is well below both the suburb and state figures. This gap could reflect differences in property values, construction types, or the mix of cover levels across the broader Mandurah area.

Third, the national average of $5,347 per year is dramatically higher than what San Remo homeowners are typically paying. Much of this is driven by elevated premiums in cyclone-prone regions of Queensland and the Northern Territory, as well as high-value properties in capital cities. Compared to the national insurance landscape, San Remo homeowners are in a relatively favourable position. You can also review WA-wide home insurance data to see how the state compares as a whole.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on what insurers charge. Here's how each one plays into the pricing:

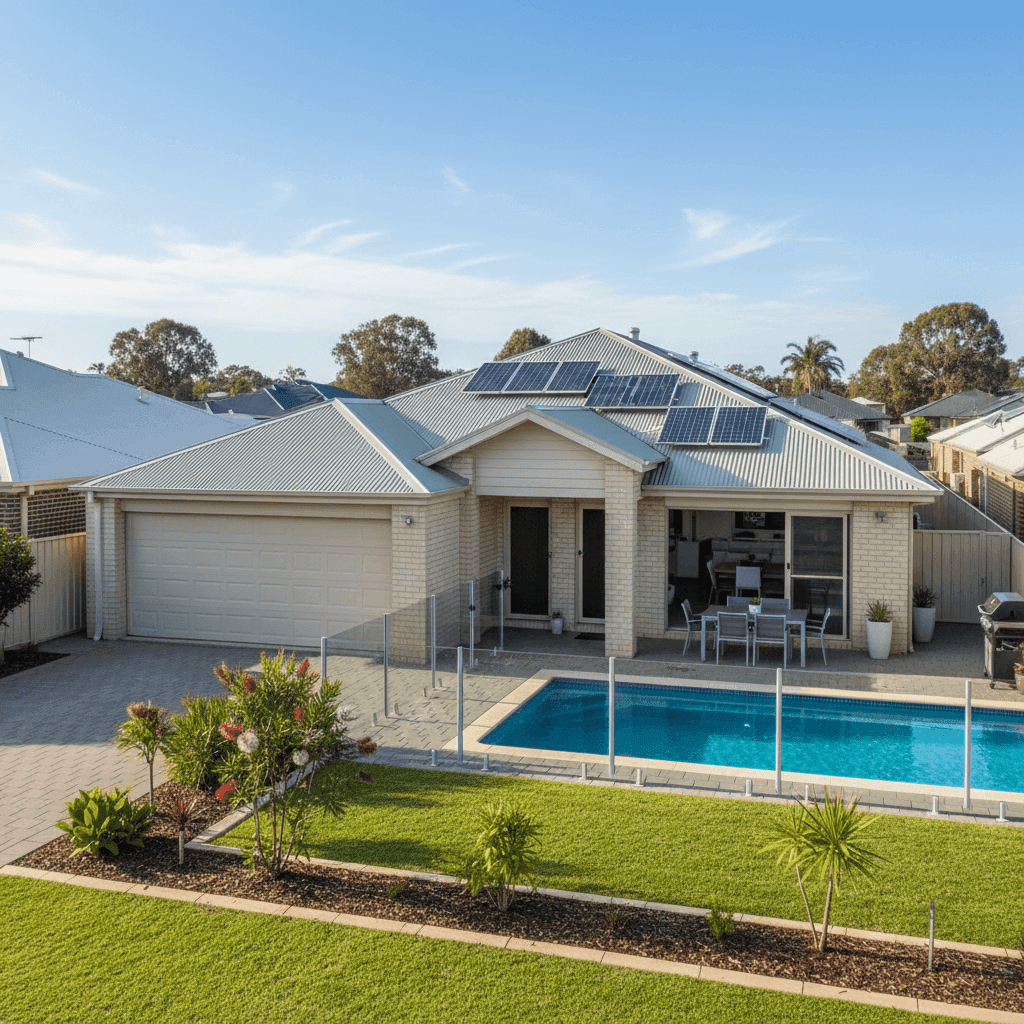

Double Brick Construction Double brick is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well over time. This construction type can actually work in your favour compared to weatherboard or lightweight cladding alternatives.

Steel / Colorbond Roof Colorbond roofing is another positive signal for insurers. It's resistant to corrosion, performs well in high winds, and has a long lifespan. Compared to older tile roofs, it typically attracts lower premiums.

Built in 1970 The age of the home is worth paying attention to. A property built in 1970 is over 50 years old, and while double brick construction ages well, insurers may factor in the potential for older electrical wiring, plumbing, or structural elements that could increase the likelihood of a claim. It's worth ensuring your building sum insured reflects the full cost to rebuild — not the market value — and that your policy covers gradual deterioration exclusions appropriately.

Swimming Pool A pool adds to your contents and liability risk profile. Most policies will cover the pool structure under building cover, but it's important to confirm this with your insurer and check what's included for pool equipment and fencing compliance.

Solar Panels Solar panels are increasingly common in WA and are generally covered under building insurance. However, coverage terms vary — some policies include inverters and panels as standard, while others may treat them as optional extras. Always confirm your panels are explicitly listed.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset and are typically covered under building insurance. Given WA's warm climate, this is an important inclusion to verify in your policy documents.

214 sqm Floor Area At 214 square metres, this is a sizeable home. Building sum insured calculations should reflect the full cost of reconstruction at current labour and materials rates — not just the land value or purchase price. With construction costs having risen sharply in recent years, it's worth reviewing your sum insured annually.

---

Tips for Homeowners in San Remo

1. Review your sum insured every year With a building sum insured of $952,000, it's essential to ensure this figure keeps pace with rising construction costs. Underinsurance is one of the most common — and costly — mistakes homeowners make. Use an independent building calculator or speak with a quantity surveyor if you're unsure.

2. Confirm solar panels and pool equipment are covered Don't assume your policy automatically covers all fixtures. Check your Product Disclosure Statement (PDS) to confirm that solar panels, inverters, pool pumps, and heating systems are explicitly included — and at what replacement value.

3. Consider your excess carefully Both the building and contents excess on this quote are set at $2,000. A higher excess generally reduces your premium, but make sure it's an amount you could comfortably pay out of pocket in the event of a claim. If cash flow is a concern, a lower excess with a slightly higher premium may be the smarter choice.

4. Shop around at renewal time A FAIR rating means this quote is competitive, but it's not necessarily the best available. Insurers price risk differently, and loyalty doesn't always pay. Use a comparison tool at renewal time to ensure you're not leaving money on the table — especially given the wide premium range seen in this suburb.

---

Compare Home Insurance Quotes in San Remo

Whether you're renewing your existing policy or insuring a new property, it pays to compare. At CoverClub, you can benchmark your quote against real data from homeowners in your suburb and across Australia. Get a home insurance quote today and see how your premium stacks up — in minutes, not hours.

--- Premium data is based on quotes collected via CoverClub and is intended as a guide only. Individual premiums will vary based on insurer, cover level, and property-specific risk factors. Always read the Product Disclosure Statement before purchasing a policy.