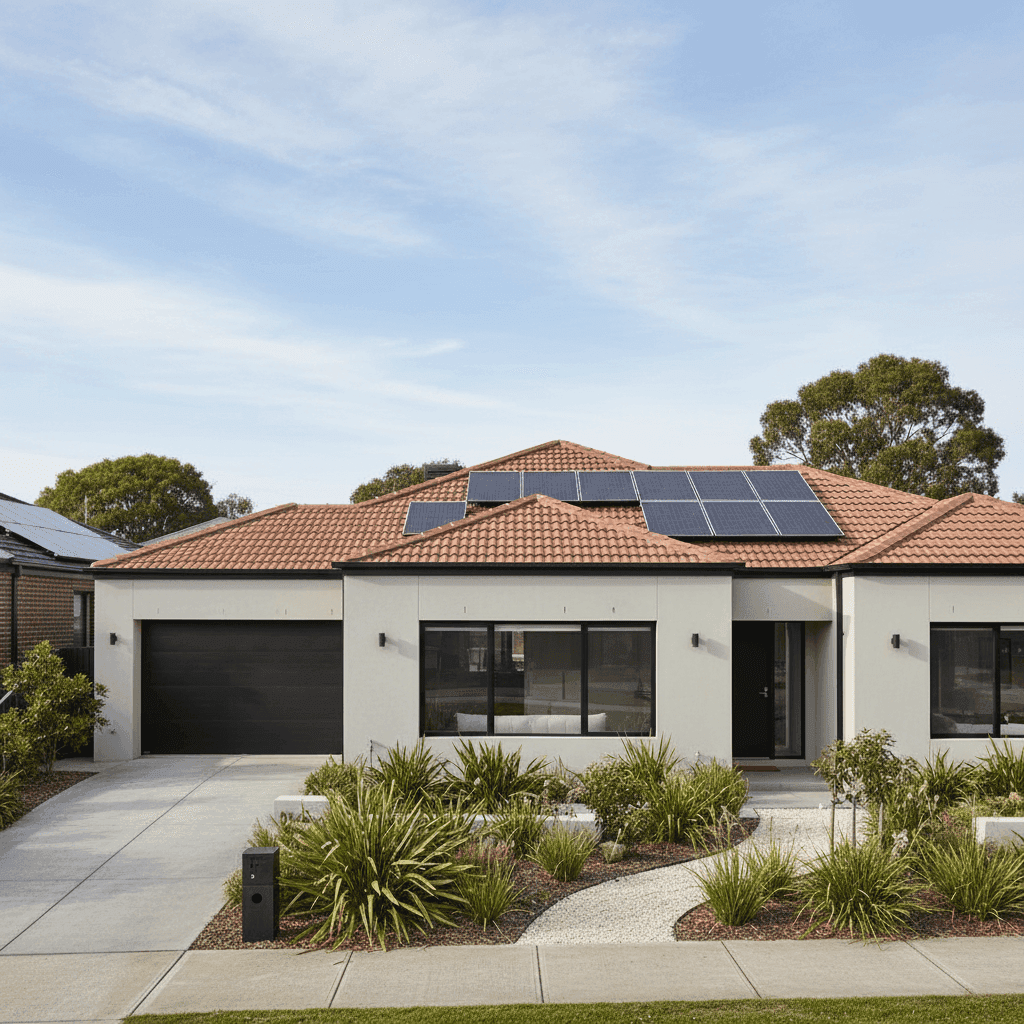

Sandringham is one of Melbourne's most desirable bayside suburbs — a leafy, well-established pocket of Victoria known for its proximity to the beach, quality schools, and a strong property market. It's also a suburb where home insurance premiums can vary significantly depending on your property's characteristics. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom semi detached property in Sandringham (postcode 3191), and puts that figure into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $1,953 per year (or roughly $187 per month), covering both building and contents with a sum insured of $1,400,000 for the building and $400,000 for contents. Both the building and contents excess sit at $5,000.

Our price rating for this quote is Fair — Around Average.

At first glance, $1,953 might sound like a lot, but context is everything in insurance. When you stack this figure against the suburb-level data for Sandringham, it actually sits below both the suburb average and median premium. The suburb average is $3,321 per year, and the median is $2,244 — meaning this quote beats more than half of the 32 quotes recorded in the area.

More precisely, the quote falls between the 25th percentile ($1,843/yr) and the median ($2,244/yr) for Sandringham. That puts it in the lower-middle range of the local market — a solid result for a property of this size and specification.

Given the high sum insured ($1,400,000 for the building alone) and the top-of-the-range fittings, landing under the suburb median is a genuinely competitive outcome. Rebuilding a 235 sqm home with premium finishes in Melbourne's south-east is not cheap, and insurers price accordingly.

---

How Sandringham Compares

To truly appreciate where this premium sits, it helps to zoom out and look at the broader picture.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,953 |

| Sandringham 25th Percentile | $1,843 |

| Sandringham Median | $2,244 |

| Sandringham Average | $3,321 |

| Sandringham 75th Percentile | $4,710 |

| LGA Average (Bayside, Vic.) | $2,625 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

Compared to the Victorian state average of $3,000/yr, this quote is approximately 35% cheaper. Against the national average of $5,347/yr, it's less than 37 cents in the dollar — though it's worth noting that national averages are heavily skewed by high-risk regions such as Far North Queensland, flood-prone inland areas, and cyclone-affected coastal zones.

The Bayside LGA average of $2,625 per year also sits comfortably above this quote, reinforcing that the premium here is on the more competitive end of what Sandringham homeowners typically encounter.

---

Property Features That Affect Your Premium

Several characteristics of this property will have influenced the final premium — some favourably, and some less so.

Hebel external walls are a positive factor. Autoclaved aerated concrete (AAC) panels like Hebel are lightweight, fire-resistant, and offer strong thermal performance. Insurers generally view modern, non-combustible wall materials favourably when assessing risk, particularly in areas where ember attack or fire spread is a concern.

Tiled roof is another tick in the right column. Tiles are durable, fire-resistant, and widely regarded by insurers as a lower-risk roofing material compared to timber shingles or older corrugated iron.

Slab foundation is the standard for newer builds and is typically considered stable and low-risk, particularly in coastal suburban areas like Sandringham that don't face significant subsidence or reactive soil issues.

Construction year 2021 is a meaningful advantage. A near-new home built to current Australian Standards means modern electrical wiring, compliant plumbing, and up-to-date building codes — all of which reduce the likelihood of a claim and are viewed positively by underwriters.

Timber and laminate flooring adds to the contents and building replacement cost, which may nudge the premium slightly higher, but the impact is generally modest.

Solar panels are an increasingly common feature, but they do add to the replacement value of the building and can increase the cost of a roof-related claim. Most insurers now include solar panels as part of the building sum insured, so it's worth confirming your coverage explicitly covers the system.

Ducted climate control is another high-value fixed asset that contributes to the building sum insured. A full ducted system in a 235 sqm home can cost $15,000–$30,000 to replace, so ensuring your $1,400,000 sum insured accounts for this is sensible.

Top-of-the-range fittings across a four-bedroom, three-bathroom home will push the per-sqm rebuild cost well above standard estimates. This is likely a key driver of the higher-than-typical sum insured, and it's appropriate — underinsurance is a serious risk for premium-finish properties.

---

Tips for Homeowners in Sandringham

1. Review your sum insured annually Building costs in Melbourne have risen sharply in recent years. A sum insured set at purchase may no longer reflect actual rebuild costs, especially with premium materials like Hebel and high-end fittings. Use a building cost calculator or speak with a quantity surveyor to validate your figure each year.

2. Confirm solar panel coverage Check your policy wording carefully to ensure your solar panel system is explicitly covered — both for damage to the panels themselves and for any liability arising from installation or electrical faults. Not all policies treat solar the same way.

3. Consider your excess carefully Both the building and contents excess on this policy are set at $5,000. A higher excess typically reduces your premium, but it means you'll need to cover the first $5,000 of any claim out of pocket. Make sure this aligns with your financial comfort level and that you have accessible savings to cover it if needed.

4. Don't set and forget your contents cover $400,000 in contents cover is substantial, but for a four-bedroom home with top-of-the-range fittings, it may not be excessive. Walk through each room and take stock of electronics, furniture, appliances, artwork, and clothing. A home inventory — even a simple photo record — can make claims far smoother.

---

Compare Your Options with CoverClub

Whether you're a Sandringham local reviewing your current policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against real data from your suburb, your state, and across Australia. Get a home insurance quote today and find out if you could be paying less — or whether you're already getting a fair deal.