Sans Souci is a leafy, waterside suburb in Sydney's south, sitting within the Georges River local government area. It's a popular spot for families drawn to its harbour foreshore, quality schools, and relaxed lifestyle — and the housing stock reflects that, with a mix of established homes and newer builds commanding serious real estate values. With property prices high, making sure your home and contents insurance is both comprehensive and competitively priced is more important than ever.

This article breaks down a recent home and contents insurance quote for a five-bedroom free standing home in Sans Souci (postcode 2219), comparing it against suburb, state, and national benchmarks to help you understand what a fair price looks like — and how to get one.

---

Is This Quote Fair?

The short answer: yes — and then some. This quote came in at $2,567 per year (or $246 per month) for a home and contents policy covering a building sum insured of $1,097,000 and contents valued at $109,000. CoverClub's pricing engine rates this as CHEAP — below average for the area.

To put that in perspective, the average premium across the nine quotes sampled in the Sans Souci suburb sits at $4,227 per year, with a median of $3,399. This quote lands well below even the 25th percentile of $2,998 — meaning it's cheaper than at least 75% of comparable quotes in the suburb. That's a genuinely strong result for a property of this size and value.

The excess is set at $2,000 for both building and contents, which is on the higher side and likely contributes to keeping the premium down. It's worth keeping in mind that a higher excess means more out-of-pocket cost if you do need to make a claim, so make sure that trade-off suits your financial situation.

---

How Sans Souci Compares

Zooming out to a broader view, the numbers tell an interesting story.

| Benchmark | Premium |

|---|---|

| This quote | $2,567/yr |

| Sans Souci suburb average | $4,227/yr |

| Sans Souci suburb median | $3,399/yr |

| Georges River LGA average | $2,880/yr |

| NSW state average | $9,528/yr |

| NSW state median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

The NSW state average of $9,528 looks eye-watering, but it's heavily skewed by high-risk postcode areas — coastal flood zones, bushfire-prone regions, and cyclone corridors in northern NSW all push that figure up significantly. The state median of $3,770 is a more reliable reference point, and this quote still comes in well beneath it.

At a national level, the average sits at $5,347, while the median is $2,764 — meaning this quote is broadly in line with what typical Australian homeowners pay nationally, even though this is a significantly larger-than-average home in a high-value Sydney suburb.

You can explore more data on Sans Souci insurance premiums, compare it against NSW-wide statistics, or check out national home insurance benchmarks to see where your own property sits.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an insurance pricing perspective.

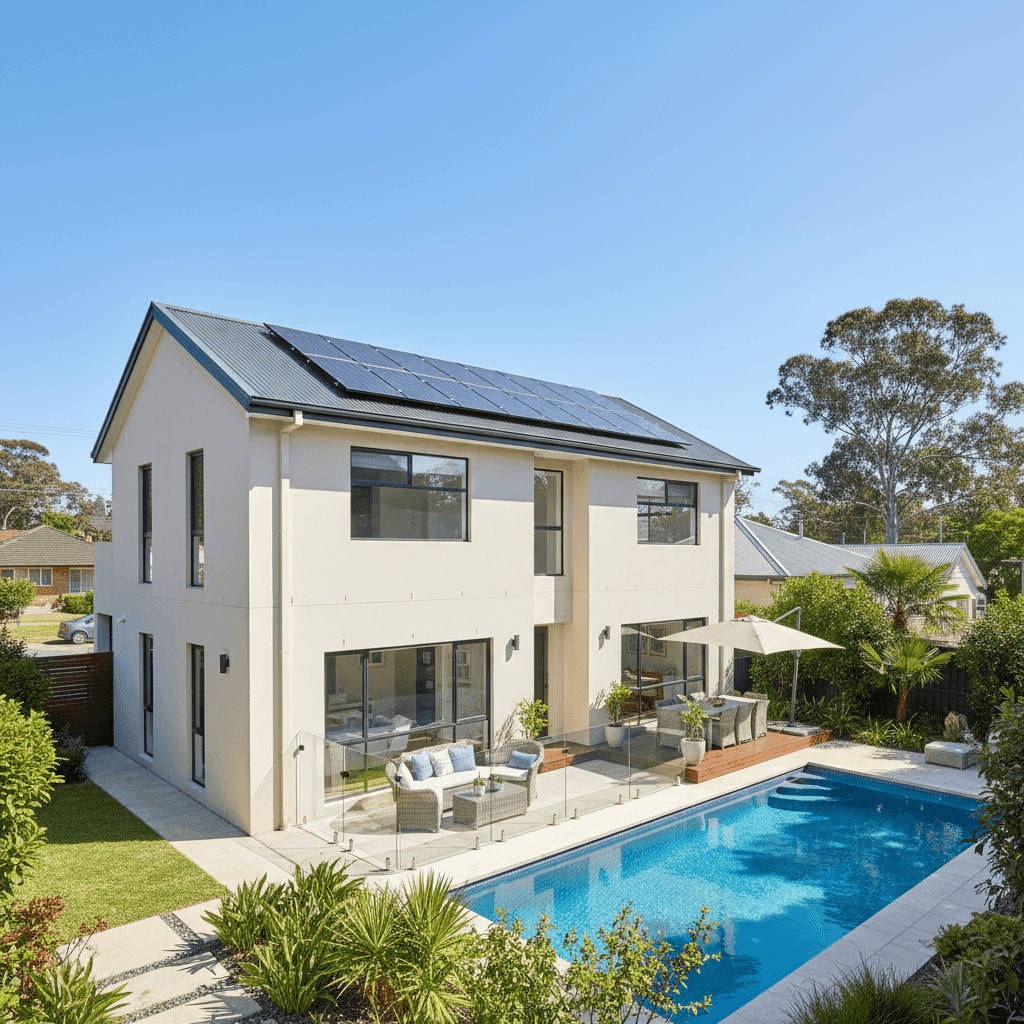

Hebel external walls are a standout. Autoclaved aerated concrete (AAC) panels like Hebel are highly regarded by insurers for their fire resistance and structural durability. Unlike timber-framed weatherboard homes, Hebel doesn't contribute to fire spread, which can meaningfully reduce risk assessments — particularly relevant in greater Sydney where ember attack remains a concern.

Steel/Colorbond roofing is another positive. It's durable, low-maintenance, and performs well in high-wind events and heavy rain. Insurers generally view it more favourably than terracotta or concrete tiles, which can crack or dislodge more easily.

Slab foundation is the most common and structurally stable foundation type in modern Australian construction, and it carries no particular premium loading. Similarly, tile flooring is considered low-risk compared to timber floors, which can be more susceptible to water damage claims.

Construction year 2020 is a significant advantage. Newer homes are built to more stringent building codes, with better waterproofing, electrical systems, and structural engineering. Insurers price this in — a four-year-old home carries far less latent risk than one built in the 1970s or 80s.

The above average fittings quality does add some cost to the building sum insured, as higher-end fixtures and finishes are more expensive to replace. At $1,097,000, the building cover reflects this — but it's essential to insure to full replacement value, not market value.

The swimming pool adds a modest premium loading due to liability considerations and the cost of repair or replacement if damaged. Solar panels are increasingly common on Australian rooftops and most insurers now include them under standard building cover, though it's always worth confirming this explicitly with your provider. Ducted climate control is a significant fixed asset and also factors into the replacement cost calculation.

At 315 sqm, this is a substantial home — well above the national average floor area — and the premium still comes in competitively, which speaks to the overall low-risk profile of the property and its location.

---

Tips for Homeowners in Sans Souci

1. Review your sum insured annually Building costs in Sydney have risen sharply over the past few years. A sum insured set even two years ago may no longer reflect the true cost of rebuilding your home from scratch. Use a building cost calculator or speak to a quantity surveyor to make sure you're not underinsured.

2. Confirm your solar panels are covered Solar panel systems can be worth $10,000–$30,000 or more. Most home building policies cover panels as a fixed structure, but exclusions can apply — particularly for mechanical or electrical breakdown. Check your Product Disclosure Statement carefully.

3. Don't overlook pool liability A swimming pool increases your exposure to public liability claims. Make sure your policy includes adequate liability cover (most standard policies offer $20 million, but it's worth checking) and that the pool complies with NSW pool fencing regulations — non-compliance can affect your ability to claim.

4. Compare quotes before renewal Insurance premiums can shift significantly year on year, and loyalty doesn't always pay. Even if you're happy with your current insurer, running a comparison at renewal time takes minutes and could save you hundreds. Get a home insurance quote through CoverClub to see what the market currently offers for your property.

---

Ready to Compare?

Whether you're a homeowner in Sans Souci or anywhere else in Australia, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy — just enter your address and get a clear picture of where your premium sits relative to the market. Start your comparison today and find out if your current policy is as competitive as it should be.