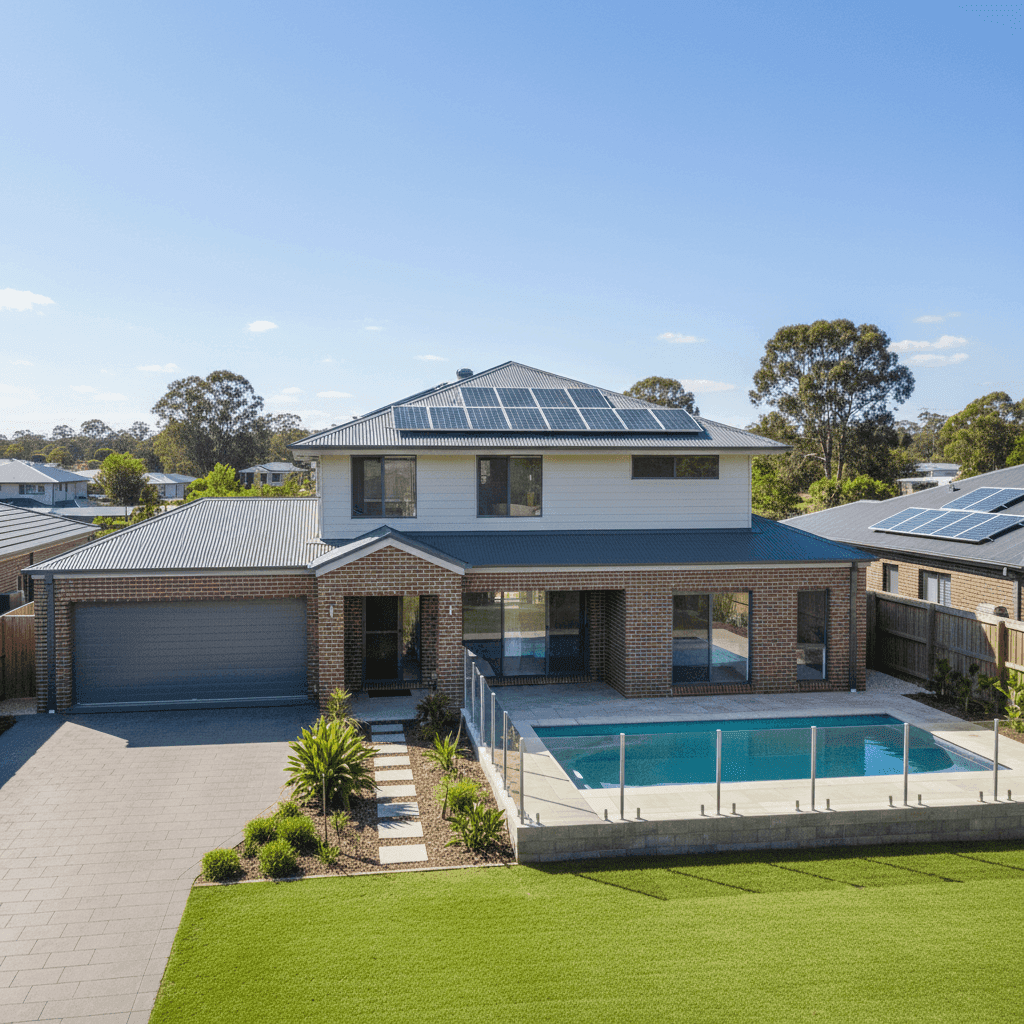

Seventeen Mile Rocks, nestled in Brisbane's western suburbs along the Brisbane River, is a well-established residential pocket popular with families seeking spacious homes close to the city. If you own a free standing home here — particularly a larger one with five bedrooms, a pool, and solar panels — understanding what you should be paying for home and contents insurance is an important part of managing your household finances. This article breaks down a real insurance quote for a property in this suburb and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,752 per year (or $257/month) for a combined home and contents policy, covering a building sum insured of $840,000 and $60,000 worth of contents, each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average, which is a reasonable outcome for a property of this size and specification. It sits comfortably below the suburb average of $3,317/year and just under the suburb median of $2,920/year, suggesting the policyholder is getting a slightly better-than-typical deal for Seventeen Mile Rocks without being in the cheapest tier of the market.

That said, "fair" doesn't necessarily mean "the best available." There's meaningful spread in the market — the cheapest 25% of quotes in this suburb come in at or below $2,173/year, while the most expensive quarter exceed $4,020/year. That's a range of nearly $1,850 between the 25th and 75th percentiles, which underscores how much premiums can vary depending on the insurer, the level of cover, and the specific risk profile of your property.

---

How Seventeen Mile Rocks Compares

To properly contextualise this quote, it helps to zoom out and look at the broader picture. You can explore full suburb-level data on the Seventeen Mile Rocks insurance stats page, but here's a snapshot:

| Benchmark | Premium |

|---|---|

| This Quote | $2,752/yr |

| Suburb Average (4073) | $3,317/yr |

| Suburb Median (4073) | $2,920/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Brisbane LGA Average | $16,277/yr |

A few things stand out immediately. The QLD state average of $9,129/year is dramatically higher than what's being paid in Seventeen Mile Rocks — but this is largely a reflection of the enormous insurance burden carried by higher-risk regions of Queensland, particularly cyclone-prone areas in Far North Queensland. Those premiums pull the state average up significantly.

Similarly, the Brisbane LGA average of $16,277/year looks alarming at first glance, but this figure is heavily influenced by flood-affected and high-risk properties across the broader Brisbane local government area. Seventeen Mile Rocks itself sits in a comparatively lower-risk zone.

Looking at the national picture, the average premium of $5,347/year again reflects the influence of high-risk regions across the country. The national median of $2,764/year is actually very close to this quote, suggesting it's broadly in line with what a typical Australian homeowner pays.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them can help you make sense of your premium — and potentially find ways to reduce it.

Brick Veneer Construction & Colorbond Roof Brick veneer external walls are generally viewed favourably by insurers. They're durable, fire-resistant, and less susceptible to storm damage than some lighter cladding options. A steel Colorbond roof is similarly well-regarded — it's lightweight, resilient, and widely used across Queensland. Together, these construction materials typically attract more competitive premiums than, say, a timber-framed home with a tile roof.

Slab Foundation A concrete slab foundation is standard for homes of this era and is considered low-risk by most insurers. It eliminates concerns about subfloor flooding or pest damage that can affect raised foundations, which is a minor but positive factor in the risk assessment.

Timber/Laminate Flooring While attractive and popular, timber and laminate flooring can be more susceptible to water damage than tiles. In the event of a burst pipe or localised flooding, floor replacement costs can be significant — something worth keeping in mind when reviewing your sum insured.

Swimming Pool A pool adds value to the property but also introduces additional liability and maintenance considerations. Some insurers factor pool-related risks into their pricing, particularly for accidental damage cover.

Solar Panels Solar panels are an increasingly common feature on Brisbane homes and can add meaningful replacement value to a property. At 325 sqm with a full solar system, ensuring your building sum insured of $840,000 adequately reflects the cost to rebuild — including panels — is important.

No Cyclone Risk Seventeen Mile Rocks falls outside designated cyclone risk zones, which is a significant premium advantage compared to properties in North Queensland. This is one reason premiums here are so much lower than the state average.

---

Tips for Homeowners in Seventeen Mile Rocks

1. Review Your Building Sum Insured Regularly Construction costs have risen sharply in recent years. A $840,000 sum insured may be appropriate today, but it's worth reassessing annually. Underinsurance is one of the most common issues homeowners face at claim time — and with a 325 sqm home featuring solar panels and quality fittings, the rebuild cost can be higher than expected.

2. Check Your Flood Cover Parts of Brisbane's western suburbs have experienced flooding events in the past. Even if your specific street isn't in a high-risk flood zone, it's worth confirming whether your policy includes flood cover — and understanding the distinction between flood, storm surge, and rainwater run-off in your Product Disclosure Statement (PDS).

3. Consider a Higher Excess to Lower Your Premium With both building and contents excesses set at $1,000, there may be room to increase these if you're comfortable self-insuring smaller claims. Raising your excess can meaningfully reduce your annual premium, particularly on the building component.

4. Compare Quotes at Renewal A "fair" rating means this quote is competitive, but the market is always shifting. Insurers re-price risk regularly, and loyalty doesn't always pay. Running a fresh comparison at renewal — especially given the wide spread between the 25th and 75th percentile quotes in this suburb — could save you several hundred dollars a year.

---

Get a Quote for Your Seventeen Mile Rocks Home

Whether you're reviewing an existing policy or shopping for cover on a new purchase, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see how your premium stacks up against the market — enter your address to get started and find out if you could be paying less for the same level of protection.