Shannonvale is a quiet rural locality nestled in Far North Queensland's lush Daintree hinterland, sitting within the Douglas local government area. It's the kind of place where the landscape is breathtaking — but where the weather can be equally dramatic. For owners of a free standing home in this postcode, understanding what drives your home insurance premium is essential to making sure you're properly covered without paying more than you need to.

This article breaks down a real home and contents insurance quote for a 3-bedroom, 2-bathroom free standing home in Shannonvale (QLD 4873), compares it against state and national benchmarks, and offers practical tips to help local homeowners get the best value from their cover.

---

Is This Quote Fair?

The annual premium for this property came in at $7,363 per year (or $706/month), covering both building (sum insured: $555,000) and contents ($50,000), each with a $1,000 excess. CoverClub's pricing engine rates this quote as CHEAP — below average for the area.

At first glance, $7,363 might seem steep compared to what many Australians pay in lower-risk suburbs. But context is everything. Shannonvale sits in a designated cyclone risk zone, which immediately places it in a higher-risk category than the vast majority of Australian postcodes. Insurers price cyclone exposure heavily, reflecting the potential for catastrophic structural damage during severe tropical weather events.

Given that risk profile, a below-average rating is genuinely good news for this homeowner. It suggests the combination of property features, sum insured, and insurer pricing has landed in a competitive spot relative to what others in Queensland are paying for comparable cover.

---

How Shannonvale Compares

While no suburb-level aggregate data is available for Shannonvale specifically, we can draw meaningful comparisons using broader benchmarks. Here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $7,363/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| Douglas LGA Average | $5,140/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out from this data. The Queensland state average of $9,129/yr is notably higher than the national average of $5,347/yr — a reflection of the outsized cyclone and flood risk that affects much of the state. This quote sits $1,766 below the Queensland average, which is a meaningful saving on an already elevated baseline.

The Douglas LGA average of $5,140/yr is lower than this quote, but it's worth noting that LGA averages can be skewed by a mix of property types, ages, and cover levels. A newly built, high-value home with a large building sum insured will naturally attract a higher premium than a modest older dwelling with minimal contents cover.

Compared to national benchmarks, this premium is higher — but that's expected for a cyclone-prone region of Far North Queensland. The relevant comparison for Shannonvale homeowners is really the Queensland average, against which this quote performs well. You can explore more local data on the Shannonvale suburb stats page.

---

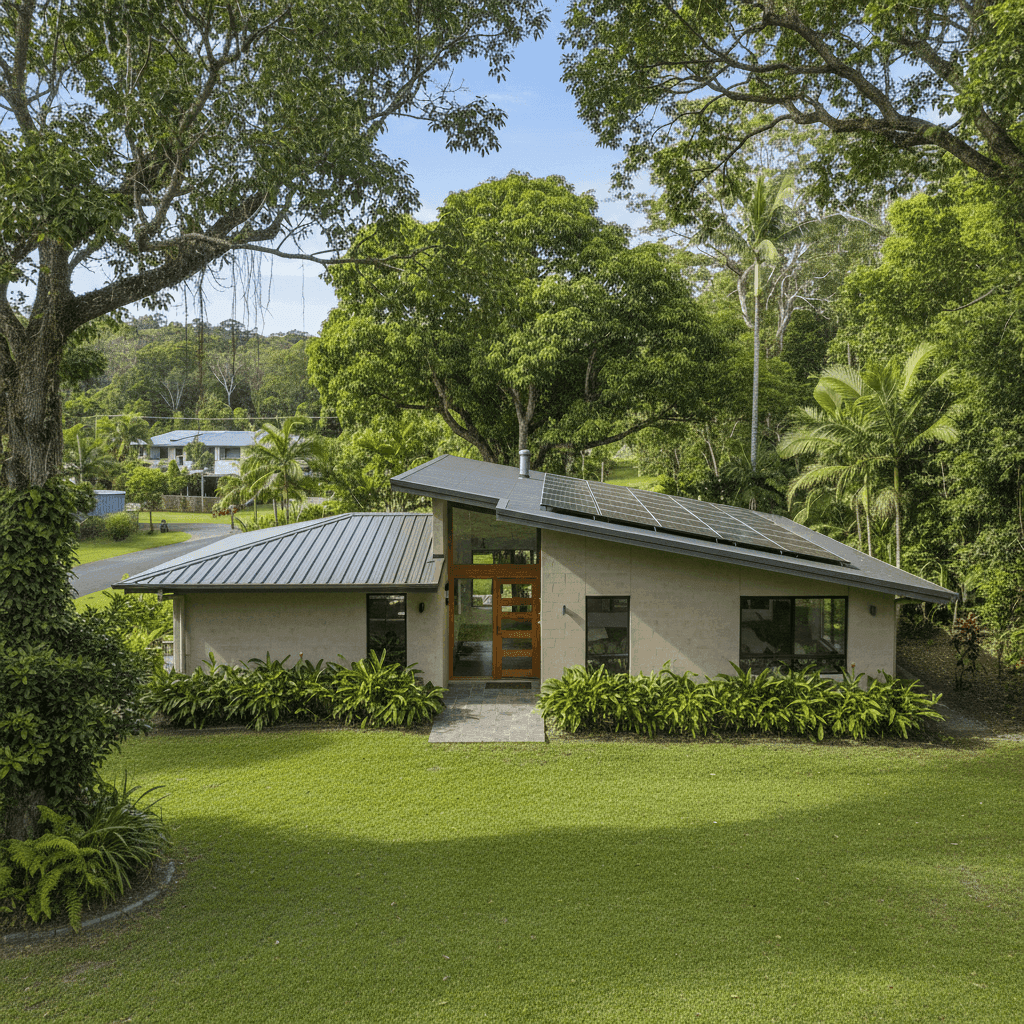

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers calculate risk and, ultimately, what you pay.

Cyclone Risk Zone

This is the single biggest factor. Properties in designated cyclone risk areas attract significant loading from insurers due to the potential for wind damage, storm surge, and associated water ingress. There's no way to remove this risk factor — it's geographic — but choosing a well-built, resilient home can help moderate the impact.

Concrete External Walls

Concrete construction is generally viewed favourably by insurers. It's more resistant to wind, fire, and impact damage than timber weatherboard, which means it can help keep premiums lower relative to other wall types in the same risk zone. For a cyclone-prone area, this is a meaningful advantage.

Steel / Colorbond Roof

A Colorbond steel roof is a strong performer in cyclone and storm conditions when properly installed to Australian standards. It's lightweight, resistant to corrosion, and less likely to fail under wind loading than some alternative roofing materials. Insurers typically regard this positively.

Slab Foundation & Tile Flooring

A concrete slab foundation provides excellent stability and is less susceptible to flood or moisture damage than raised timber floors. Combined with tile flooring throughout, this property has a moisture-resilient profile — an important consideration in the wet tropics climate of Far North Queensland.

Solar Panels

The presence of solar panels adds a modest amount to the insured value of the property and may slightly increase premiums. It's important to ensure your building sum insured accounts for the replacement cost of the solar system, as panels can be expensive to replace after a storm or cyclone event.

Building Size & Sum Insured

At 139 sqm and a building sum insured of $555,000, this property carries a relatively high per-square-metre replacement value. This reflects the cost of construction in a remote Far North Queensland location, where materials and labour are more expensive than in major urban centres.

---

Tips for Homeowners in Shannonvale

1. Check your cyclone preparedness — and let your insurer know Some insurers offer discounts or more competitive pricing for homes that have been cyclone-rated or upgraded with storm shutters, reinforced garage doors, or other resilience measures. If you've made improvements, it's worth flagging these when obtaining quotes.

2. Review your building sum insured regularly Construction costs in regional Queensland have risen significantly in recent years. Make sure your sum insured reflects the true cost of rebuilding your home from scratch — not just its market value. Underinsurance is a common and costly mistake, particularly after a major weather event.

3. Don't forget your solar panels Ensure your solar system is explicitly covered under your building policy. Check whether your insurer covers the panels for storm and cyclone damage, and confirm the replacement value is factored into your sum insured.

4. Compare quotes annually Even if you're happy with your current insurer, the home insurance market is competitive. Premiums can shift significantly from year to year, and loyalty doesn't always translate to the best price. Use a comparison platform like CoverClub to benchmark your renewal quote before you commit.

---

Ready to Compare?

Whether you're a first-time buyer in Shannonvale or a long-term homeowner reviewing your cover, comparing quotes is one of the simplest ways to make sure you're not overpaying. Get a home and contents insurance quote at CoverClub and see how your current premium stacks up in seconds.