If you own a free standing home in Sharon, QLD 4670, you've probably noticed that insurance premiums can vary quite a bit depending on your property's features, location, and the level of cover you choose. This article takes a deep dive into a real home and contents insurance quote for a four-bedroom, double brick home in Sharon — breaking down what the premium reflects, how it stacks up against local and national benchmarks, and what you can do to make sure you're getting the best value for your cover.

---

Is This Quote Fair?

The quote in question comes in at $4,624 per year (or $452/month) for combined home and contents cover, with a building sum insured of $870,000 and contents valued at $30,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — around average. That's a meaningful result. It tells us the premium isn't unusually high or suspiciously low; it sits comfortably within the typical range for comparable properties in the area.

To put that in context:

- The suburb average for Sharon (QLD 4670) is $5,077/year, and the median sits at $4,294/year

- This quote of $4,624 falls between the suburb median and average, which is a solid position — it's better than average, yet not an outlier that might signal under-insurance or stripped-back cover

- The 75th percentile in the suburb is $5,118/year, meaning roughly three-quarters of comparable quotes come in at or below that figure — and this quote sits well within that range

In short, for a property of this size and specification in Sharon, $4,624 is a reasonable and competitive premium. You're not overpaying significantly, but there may still be room to improve.

---

How Sharon Compares

Understanding your premium means looking beyond your own postcode. Here's how Sharon stacks up against broader benchmarks, based on data from CoverClub's Sharon suburb stats:

| Benchmark | Annual Premium |

|---|---|

| Sharon suburb average | $5,077 |

| Sharon suburb median | $4,294 |

| This quote | $4,624 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. The Queensland state average of $9,129 is remarkably high — significantly above both the national average and this quote. This is largely driven by high-risk postcodes across Queensland, particularly coastal and cyclone-prone regions in Far North QLD, where premiums can be extreme. Sharon, located in the Bundaberg region, sits outside the designated cyclone risk zone, which is a meaningful advantage for homeowners here.

Compared to the national average of $5,347, this quote is about $723 less per year — a positive sign that Sharon isn't being penalised by the broader Queensland risk profile. The national median of $2,764 is considerably lower, but that figure is heavily influenced by lower-risk, lower-value properties in metropolitan and regional areas across all states.

With a suburb sample size of 41 quotes, the Sharon data is reasonably representative, giving us confidence in these comparisons.

---

Property Features That Affect Your Premium

The specific characteristics of this property play a significant role in determining the premium. Here's what matters most:

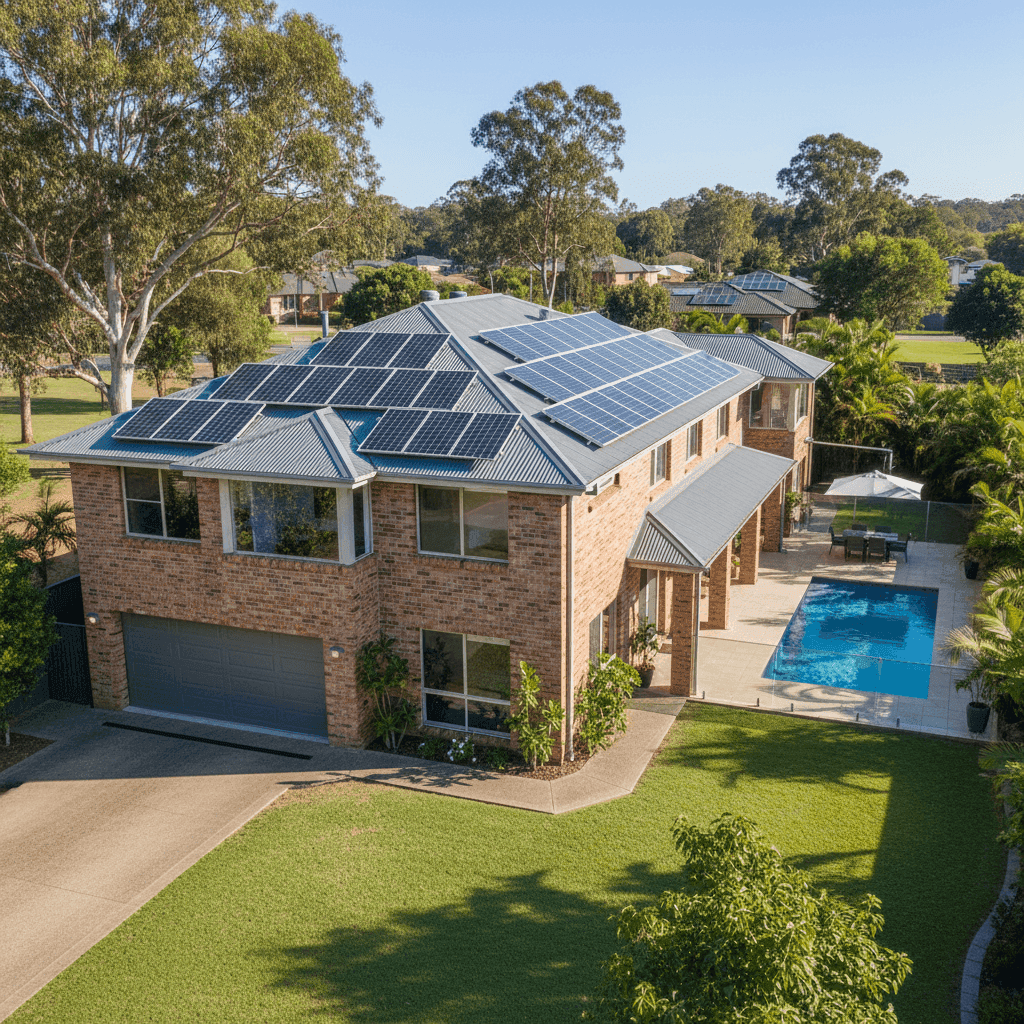

Double Brick Construction

Double brick external walls are generally viewed favourably by insurers. They offer strong resistance to fire, wind, and impact damage compared to timber or lightweight cladding. This construction type typically attracts lower premiums or at least doesn't attract surcharges — a definite plus for this property.

Steel/Colorbond Roof

Colorbond steel roofing is one of the most popular and insurer-friendly roof types in Australia. It's durable, resistant to ember attack, and handles heavy rain well. Insurers tend to price this more competitively than older materials like terracotta tiles or asbestos sheeting.

Slab Foundation

A concrete slab foundation is standard for homes of this era and is generally considered low-risk from an insurance perspective. It reduces exposure to subfloor issues like termite damage or moisture ingress that can affect raised foundations.

Swimming Pool

The presence of a pool adds replacement value to the property and may contribute modestly to the premium. Pools also introduce a liability consideration, though this is typically covered under a standard home policy. It's worth confirming your policy explicitly covers pool structures and associated equipment.

Solar Panels

Solar panels are an increasingly common feature and can affect your sum insured. The $870,000 building sum insured on this policy should ideally account for the replacement cost of the solar system. Check with your insurer that panels are included in building cover — some policies treat them as a grey area between building and contents.

Ducted Climate Control

Ducted air conditioning systems are a fixed building feature and should be captured in the building sum insured. Given the Bundaberg region's warm climate, this is a valuable asset worth protecting.

Construction Year: 1992

At over 30 years old, this home is well-established but not ancient. Insurers may factor in the age of electrical wiring, plumbing, and roofing when pricing. A property this age in good condition generally doesn't attract significant age-related loadings.

---

Tips for Homeowners in Sharon

Whether you're renewing your policy or shopping around for the first time, here are some practical steps to get the most out of your home insurance:

- Review your sum insured regularly. Building costs have risen sharply in recent years. An $870,000 sum insured needs to reflect what it would actually cost to rebuild your home from scratch — including the pool, solar system, and ducted air conditioning. Use a building cost calculator or speak to a quantity surveyor if you're unsure. Being under-insured can leave you seriously out of pocket after a major claim.

- Check what's included for your pool and solar panels. These are two areas where policy wording varies significantly between insurers. Confirm that your pool structure, pump, and filtration equipment are covered under building, and that your solar panels and inverter are explicitly included. Don't assume — ask.

- Consider your excess strategically. Both the building and contents excess on this policy are set at $1,000. Opting for a higher excess (say, $2,000 or $2,500) can reduce your annual premium meaningfully. If you have a good claims history and solid emergency savings, this trade-off can make financial sense.

- Compare quotes at renewal time. The insurance market is competitive, and loyalty doesn't always pay. Even if your current premium seems fair, running a comparison at renewal can reveal better value — or confirm you're already well-placed. Use CoverClub to compare home insurance quotes in minutes.

---

Get a Quote That Works for You

Whether you're a long-term Sharon resident or new to the area, making sure your home and contents insurance is both adequate and competitively priced is one of the smartest financial moves you can make. CoverClub makes it easy to compare real quotes from multiple insurers, so you can see exactly where your premium sits and whether there's a better deal available.

Start comparing home insurance quotes at CoverClub — it takes just a few minutes and could save you hundreds every year.