Shell Cove is one of the Illawarra region's most sought-after coastal suburbs, sitting within the Shellharbour local government area just south of Wollongong. It's a relatively modern, master-planned community, which means the housing stock tends to be newer, well-built, and increasingly valuable. For owners of a free standing home in this suburb, getting the right home and contents insurance — and making sure you're not overpaying for it — is an important part of protecting what is likely your most significant asset.

This article breaks down a real insurance quote for a four-bedroom, three-bathroom free standing home in Shell Cove, compares it against local, state, and national benchmarks, and offers practical guidance for homeowners looking to get better value from their cover.

---

Is This Quote Fair?

The quote in question comes in at $3,402 per year (or $326/month) for combined home and contents insurance, covering a building sum insured of $950,000 and contents valued at $150,000, each with a $1,000 excess.

Our price rating for this quote is Expensive (Above Average).

To put that in context: the average home insurance premium in Shell Cove sits at $1,943/yr, with a median of $1,662/yr. This quote is roughly 75% above the suburb average and more than double the median — a significant gap that warrants closer inspection.

That said, it's worth noting that the suburb sample includes a range of property types, sizes, and cover levels. A 235 sqm home with above-average fittings, a $950,000 building sum insured, and $150,000 in contents is likely sitting at the higher end of the local market. Higher insured values naturally attract higher premiums, so some of this gap is expected. Even so, the magnitude of the difference suggests there may be room to shop around.

---

How Shell Cove Compares

Understanding where Shell Cove sits within the broader insurance landscape helps frame whether this suburb is inherently expensive to insure — or whether this particular quote is an outlier.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Shell Cove (suburb) | $1,943/yr | $1,662/yr |

| Shellharbour LGA | $1,744/yr | — |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Shell Cove and the broader Shellharbour LGA are actually well below both state and national averages — a reassuring sign that the area doesn't carry the kind of elevated risk profile (think flood plains, cyclone zones, or bushfire corridors) that can send premiums soaring in other parts of the country.

The NSW state average of $9,528/yr is heavily skewed by high-risk and high-value properties elsewhere in the state, while the national average of $5,347/yr reflects similar distortion. The median figures — $3,770/yr for NSW and $2,764/yr nationally — are more representative of what most homeowners actually pay.

At $3,402/yr, this quote sits below the NSW median and is approaching the national median, which is a more reasonable position given the property's size and insured values. Still, compared to what neighbours in Shell Cove are typically paying, there's a clear case for comparing alternatives.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium, both positively and negatively.

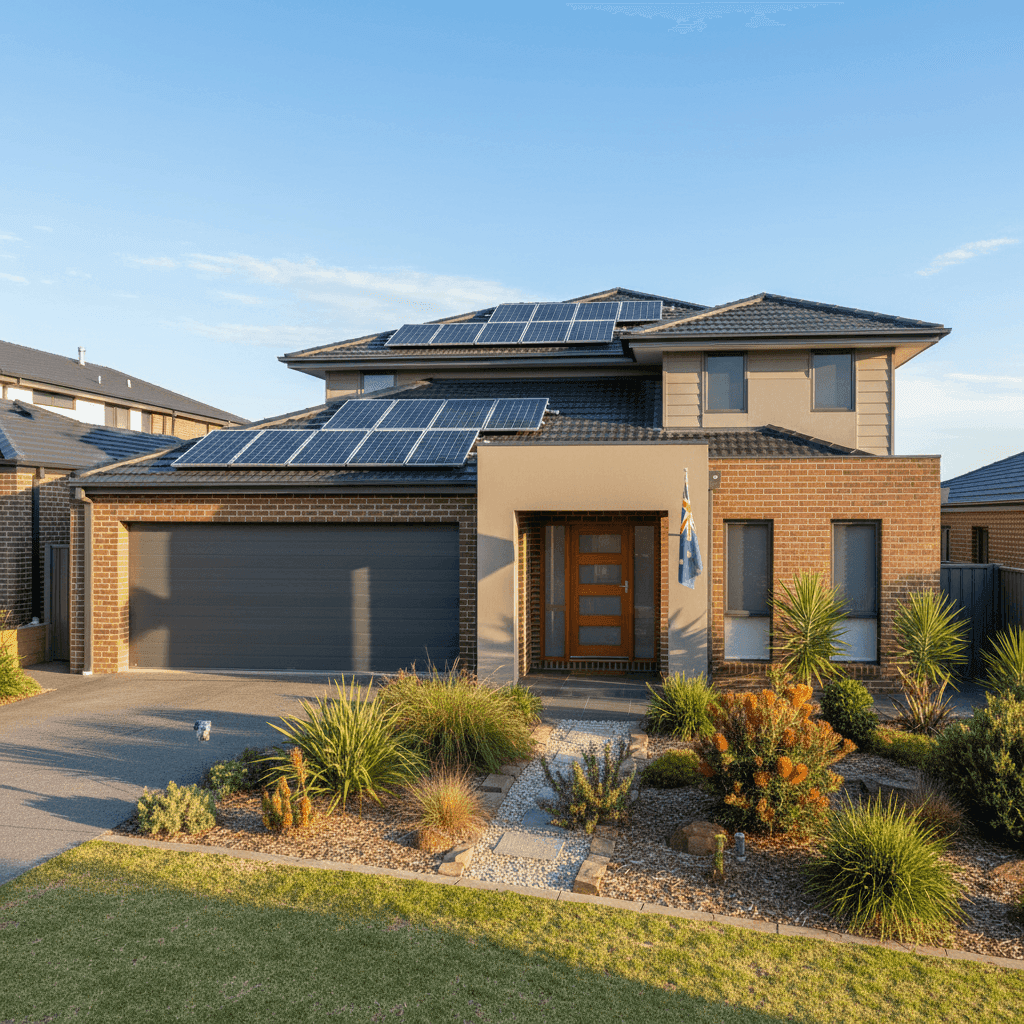

Brick veneer construction and tiled roof are generally viewed favourably by insurers. Brick veneer walls offer solid fire resistance and durability, while tiled roofs are considered low-maintenance and long-lasting compared to alternatives like Colorbond or fibrous cement. These factors can contribute to more competitive premiums.

Slab foundation is standard for homes of this era and construction type in coastal NSW. It's straightforward for insurers to assess and doesn't carry the subsidence or moisture risks sometimes associated with older suspended timber floors.

Construction year of 2009 means the home is relatively modern — built to contemporary Australian Standards for structural integrity and energy efficiency. Newer homes typically attract lower premiums than older ones, as the risk of electrical faults, plumbing failures, and structural issues is reduced.

Above-average fittings are a notable factor. Kitchens with stone benchtops, premium appliances, designer bathrooms, and high-end flooring all increase the cost to rebuild or repair — which is reflected in both the building sum insured and the premium. This is appropriate and important: underinsuring a well-appointed home is a common and costly mistake.

Solar panels add modest complexity to an insurance assessment. They increase the replacement value of the home and can be a source of electrical risk if damaged. Homeowners should confirm that their policy explicitly covers solar panels — both the panels themselves and any damage they might cause to the roof.

Ducted climate control is another above-average feature that contributes to the overall replacement cost. Like solar panels, it's worth verifying that your policy covers the full system, including ducting and the compressor unit.

---

Tips for Homeowners in Shell Cove

1. Review your building sum insured carefully. A $950,000 building sum insured is substantial, but it needs to reflect the actual cost of rebuilding your home from scratch — not its market value. Given the property's size (235 sqm), above-average fittings, and coastal location (which can affect material and labour costs), it's worth using a professional quantity surveyor or an online rebuild cost calculator to validate this figure annually.

2. Confirm solar panel and ducted AC coverage. Not all standard home insurance policies automatically cover solar panel systems or ducted air conditioning under their default terms. Read the Product Disclosure Statement carefully, or ask your insurer directly, to ensure these assets are fully covered for both damage and liability.

3. Compare at least three quotes before renewing. Given that this quote is priced above the suburb average, shopping around is strongly recommended. Insurers use different risk models, and the same property can attract meaningfully different premiums across providers. Use CoverClub to compare quotes quickly and without the hassle of contacting insurers individually.

4. Consider whether your contents sum is right. $150,000 in contents cover is a reasonable starting point for a well-furnished four-bedroom home, but it's easy to underestimate. Do a room-by-room audit of your furniture, electronics, clothing, jewellery, and appliances. Many homeowners are surprised to find their contents are worth significantly more — or less — than their current cover level suggests.

---

Compare Your Home Insurance Today

Whether you're reviewing an existing policy or shopping for cover for the first time, getting multiple quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to compare home and contents insurance options tailored to your property in Shell Cove.

Get a quote now at CoverClub and see how your premium stacks up against what other homeowners in your suburb are paying.