Shell Cove is one of the Illawarra region's most sought-after coastal suburbs, sitting within the Shellharbour local government area just south of Wollongong. Known for its marina precinct, modern housing estates, and proximity to the beach, it attracts families and sea-changers alike. If you own a free standing home here, understanding what drives your insurance premium — and whether you're paying a fair price — is well worth your time.

This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom free standing home in Shell Cove, and benchmarks it against local, state, and national data to help you make an informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,366 per year (or $323 per month) for combined home and contents cover, with a building sum insured of $718,000 and contents valued at $235,000. Both the building and contents excess are set at $1,000.

Our analysis rates this quote as Expensive — Above Average for the area.

To put that in perspective, the suburb average for Shell Cove sits at just $1,943 per year, with a median of $1,662. That means this particular quote is running roughly 73% above the suburb average and more than double the local median. Even at the 75th percentile — meaning only one in four quotes in the suburb are more expensive — premiums sit at $2,363 per year, still well below the $3,366 being quoted here.

That said, context matters. The sum insured on the building ($718,000) is substantial, and the contents cover ($235,000) adds meaningful weight to the total premium. Higher insured values naturally push premiums upward, and a direct comparison to suburb averages doesn't always account for differences in coverage levels. Still, the gap is wide enough to warrant shopping around.

---

How Shell Cove Compares

Zooming out to a broader view, Shell Cove actually sits in a relatively affordable part of the country when it comes to home insurance.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Shell Cove (suburb) | $1,943/yr | $1,662/yr |

| Shellharbour LGA | $1,744/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 per year is heavily skewed by high-risk and high-value properties across the state — think flood-prone areas, bushfire zones, and prestige suburbs. The state median of $3,770 is a more representative figure, and even that is higher than what most Shell Cove homeowners are paying.

Nationally, the average premium across Australia sits at $5,347, with a median of $2,764. Again, Shell Cove compares favourably — the suburb's median of $1,662 is well below the national median, suggesting the area carries relatively moderate risk in the eyes of insurers.

The quote being analysed here, at $3,366, falls below both the NSW and national averages, but sits noticeably above the local suburb benchmarks. It's not an alarming figure in a broader sense, but there's a reasonable chance a comparable policy could be found at a lower price point.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers calculate the premium.

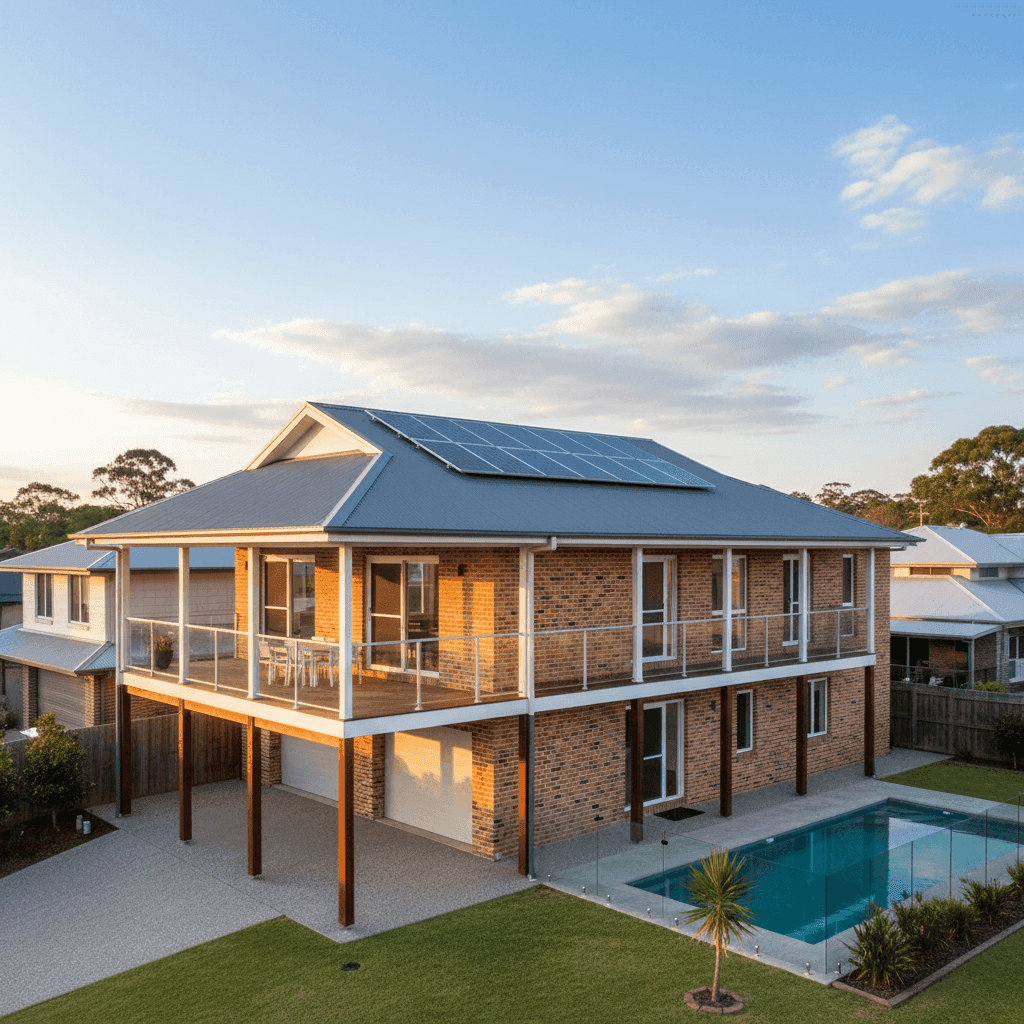

Brick veneer construction with a Colorbond roof is generally viewed favourably by insurers. Brick veneer offers solid fire resistance and structural durability, while steel Colorbond roofing is lightweight, low-maintenance, and performs well in storm conditions — all of which can moderate risk in the insurer's eyes.

Stumps foundation is worth noting. Homes on stumps (also called pier foundations) are more common in older builds and certain coastal or hilly areas. They can be associated with slightly higher risk of structural movement and subfloor moisture issues, which some insurers factor into their pricing.

Timber and laminate flooring can be a consideration for contents and building claims alike. Timber floors can be costly to repair or replace after water damage events, which may nudge the premium slightly higher compared to tile-floored homes.

The swimming pool adds liability exposure to the policy. Pool-related accidents are a real risk, and insurers price this in — particularly for family homes.

Solar panels represent a significant asset on the roof. Depending on the policy, solar systems may or may not be automatically included in building cover, and their replacement value can be considerable. Homeowners should confirm their panel system is explicitly covered.

Ducted climate control is another high-value fixed asset. Ducted systems can cost tens of thousands of dollars to repair or replace, and their inclusion in the sum insured is important to verify.

The property is elevated by less than one metre, which provides some modest benefit in terms of flood resilience compared to ground-level homes, though it's unlikely to dramatically shift the premium on its own.

---

Tips for Homeowners in Shell Cove

1. Review your sum insured carefully At $718,000, the building sum insured is the single biggest driver of this premium. Make sure it reflects the actual cost to rebuild — not the market value of the property. Overinsuring pushes your premium up unnecessarily, while underinsuring leaves you exposed. A quantity surveyor can provide an accurate rebuild estimate.

2. Confirm what's included in your building cover Solar panels and ducted air conditioning are fixed to the building but aren't always automatically covered under standard building policies. Read the Product Disclosure Statement carefully and ask your insurer directly whether these assets are included in your sum insured.

3. Shop around — the market varies significantly With a suburb average of $1,943 and this quote coming in at $3,366, there's clearly a wide spread of premiums in the market. Comparing multiple quotes for the same level of cover is the most effective way to ensure you're not overpaying. Even adjusting your excess slightly can make a meaningful difference to your annual premium.

4. Check for discounts on bundled cover Many insurers offer a discount when you combine home and contents cover under the one policy — which this quote already does. However, it's still worth asking whether additional loyalty discounts, security system discounts, or claims-free bonuses apply to your situation.

---

Compare Your Quote with CoverClub

Whether you're renewing your current policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up against real data from your suburb and beyond. Get a home insurance quote today and find out if you could be paying less for the same level of cover. You can also explore detailed Shell Cove insurance statistics to see exactly where your premium sits in the local market.