Shoalwater is a quiet coastal suburb in the City of Rockingham, about 47 kilometres south of Perth's CBD. Known for its proximity to the Shoalwater Islands Marine Park and relaxed seaside lifestyle, it's a popular choice for families seeking space without the inner-city price tag. But what does it actually cost to insure a home here — and is the quote you've been given a fair one?

This article takes a close look at a recent building insurance quote for a four-bedroom, two-bathroom free-standing home in Shoalwater (postcode 6169), breaking down the premium against local, state, and national benchmarks so you can make a more informed decision.

---

Is This Quote Fair?

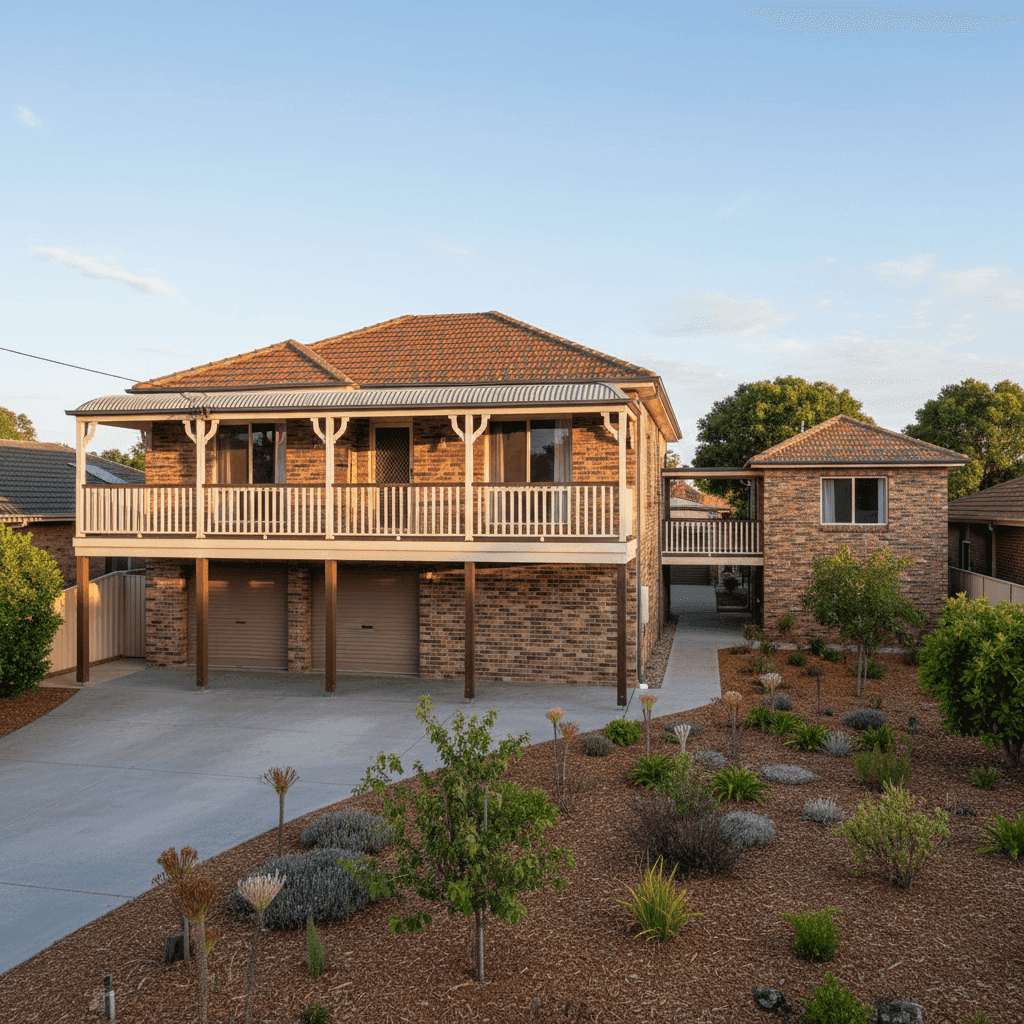

The quote in question is $2,589 per year (or $248 per month) for building-only cover on a 214 sqm brick veneer home, with a $1,000 building excess and a sum insured of $719,000.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the suburb average premium in Shoalwater sits at just $1,260 per year, with a median of $1,024. This quote comes in at more than double the local median — a significant gap that's worth interrogating before you sign on the dotted line.

That said, "expensive" doesn't necessarily mean "wrong." Several property-specific factors can legitimately push a premium above the suburb average, and this particular home has a few characteristics that insurers tend to price carefully. We'll get into those shortly.

---

How Shoalwater Compares

Understanding where Shoalwater sits in the broader pricing landscape helps frame whether this quote is an outlier or simply reflects the market.

| Benchmark | Premium |

|---|---|

| Shoalwater suburb average | $1,260/yr |

| Shoalwater suburb median | $1,024/yr |

| Shoalwater 25th percentile | $777/yr |

| Shoalwater 75th percentile | $1,785/yr |

| Rockingham LGA average | $1,561/yr |

| WA state average | $2,811/yr |

| WA state median | $2,127/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 37 quotes sampled for the Shoalwater suburb.)

Interestingly, while this quote looks steep compared to the local suburb data, it actually sits below the WA state average of $2,811 and well below the national average of $5,347. At the state level, a $2,589 annual premium is quite close to the median — suggesting that this property's features are being priced more like a typical Western Australian home than a typical Shoalwater home.

The relatively low suburb averages in Shoalwater (compared to WA broadly) likely reflect a concentration of smaller or lower-value homes in the area. A 214 sqm property with a $719,000 sum insured and a granny flat sits at the higher end of the local spectrum, which goes some way to explaining the premium gap.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely contributing to the above-average premium. Here's what insurers are probably weighing up:

Elevated Foundation on Stumps

This home is elevated by at least one metre on a stump foundation — a construction style more commonly associated with older Queensland-style homes, though found across coastal and semi-coastal WA as well. Elevated homes can be more expensive to repair after events like storms or subsidence, and stumped foundations require specific assessment when calculating rebuild costs.

Older Construction (1967)

At nearly 60 years old, this property is well beyond the age range many insurers consider "modern." Older homes may have ageing plumbing, wiring, and structural elements that increase the likelihood and cost of a claim. Insurers factor this into their risk modelling.

Granny Flat on the Property

The presence of a granny flat adds to the overall insurable value of the property and increases the complexity of a potential claim. Even under building-only cover, the granny flat structure would typically be included in the sum insured, contributing to the higher rebuild cost — and therefore the higher premium.

Brick Veneer Walls with Tiled Roof

Brick veneer with a tiled roof is a fairly standard and resilient construction combination in WA. These materials are generally viewed favourably by insurers compared to, say, weatherboard or asbestos cement. However, tiled roofs on older homes can be more costly to repair or replace if individual tiles crack or shift.

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and adds to the overall rebuild and replacement cost of the home. Insurers typically factor this into their building sum insured calculations.

No Pool, No Solar Panels

On the positive side, the absence of a pool and solar panels removes two common sources of claim risk and complexity. These omissions may be keeping the premium lower than it might otherwise be.

---

Tips for Homeowners in Shoalwater

If you're looking to get better value on your home insurance — whether you're reviewing this quote or shopping around — here are four practical steps worth taking:

- Review your sum insured carefully. A $719,000 sum insured on a 214 sqm home is substantial. Make sure this figure reflects the actual rebuild cost (not the market value) of your home, including the granny flat. Overinsuring drives up your premium unnecessarily, while underinsuring leaves you exposed.

- Ask about discounts for security features. Homes with monitored alarms, deadbolts, and security screens often attract lower premiums. If your home has these features and they weren't captured in your quote, it's worth flagging them with your insurer.

- Consider a higher excess to reduce your premium. A $1,000 excess is fairly standard, but opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium — particularly useful if you're unlikely to make small claims.

- Compare quotes annually. The home insurance market in WA is competitive, and premiums can shift significantly from year to year. Don't assume your renewal quote is the best available. Use a comparison tool to benchmark your premium against the suburb average for Shoalwater and shop around before auto-renewing.

---

Find a Better Deal with CoverClub

Whether this quote is the right one for your home or you're simply curious what else is out there, CoverClub makes it easy to compare home insurance options across Australia. Enter your property details and get a clear picture of what you should be paying — not just what you've been quoted. Get a home insurance quote today and see how your premium stacks up.