Silkwood is a small rural township in Far North Queensland, nestled in the Cassowary Coast region between Innisfail and Tully. It's a quiet community surrounded by sugarcane and banana farms — but when it comes to home insurance, its tropical location means premiums can be anything but quiet. This article breaks down a real home and contents insurance quote for a 1-bedroom free standing home in Silkwood (postcode 4856), rated CHEAP against local and national benchmarks, and explains what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $4,477 per year (or $429/month) for combined home and contents cover, with a building sum insured of $270,000 and contents valued at $20,000. The building excess is $2,000 and the contents excess is $500.

This quote has been rated CHEAP — Below Average, meaning it sits well below what most comparable properties in Silkwood are paying. That's genuinely good news for the homeowner.

To put it in perspective:

- The suburb average for Silkwood is $6,690/yr — meaning this quote is roughly $2,213 cheaper than the typical policy in the area.

- The suburb median sits even higher at $7,118/yr, and three-quarters of quotes in the suburb come in above $5,805/yr (the 25th percentile).

- Against the Queensland state average of $9,129/yr, this quote looks extremely competitive — though it's worth noting the QLD median of $3,903/yr reflects a wide spread of risk across the state, from low-risk southern suburbs to high-cyclone-risk coastal communities like Silkwood.

In short: this is a well-priced policy for the location and property type. That said, it's always worth comparing to make sure you're not sacrificing coverage quality for cost.

---

How Silkwood Compares

Home insurance in Silkwood is expensive by most Australian standards — and for good reason. The area sits within a designated cyclone risk zone, which insurers treat as a major pricing factor. Understanding where this quote sits relative to broader benchmarks helps put the premium in context.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,477 |

| Silkwood Suburb Average | $6,690 |

| Silkwood Suburb Median | $7,118 |

| Cassowary Coast LGA Average | $5,573 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

You can explore more localised data on the Silkwood suburb stats page, or zoom out to see how QLD compares statewide and how it tracks against national figures.

One important observation: the QLD state average ($9,129) is dramatically higher than the national average ($5,347), which reflects the disproportionate cyclone and flood exposure across much of Far North and North Queensland. Silkwood, sitting in the wet tropics, is a prime example of this elevated risk environment.

The fact that this particular quote comes in below both the suburb average and the national average is noteworthy — it suggests the insurer has assessed the specific property features favourably.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the quote — some pushing the premium up, others helping to bring it down.

🔴 Factors That Increase Risk (and Cost)

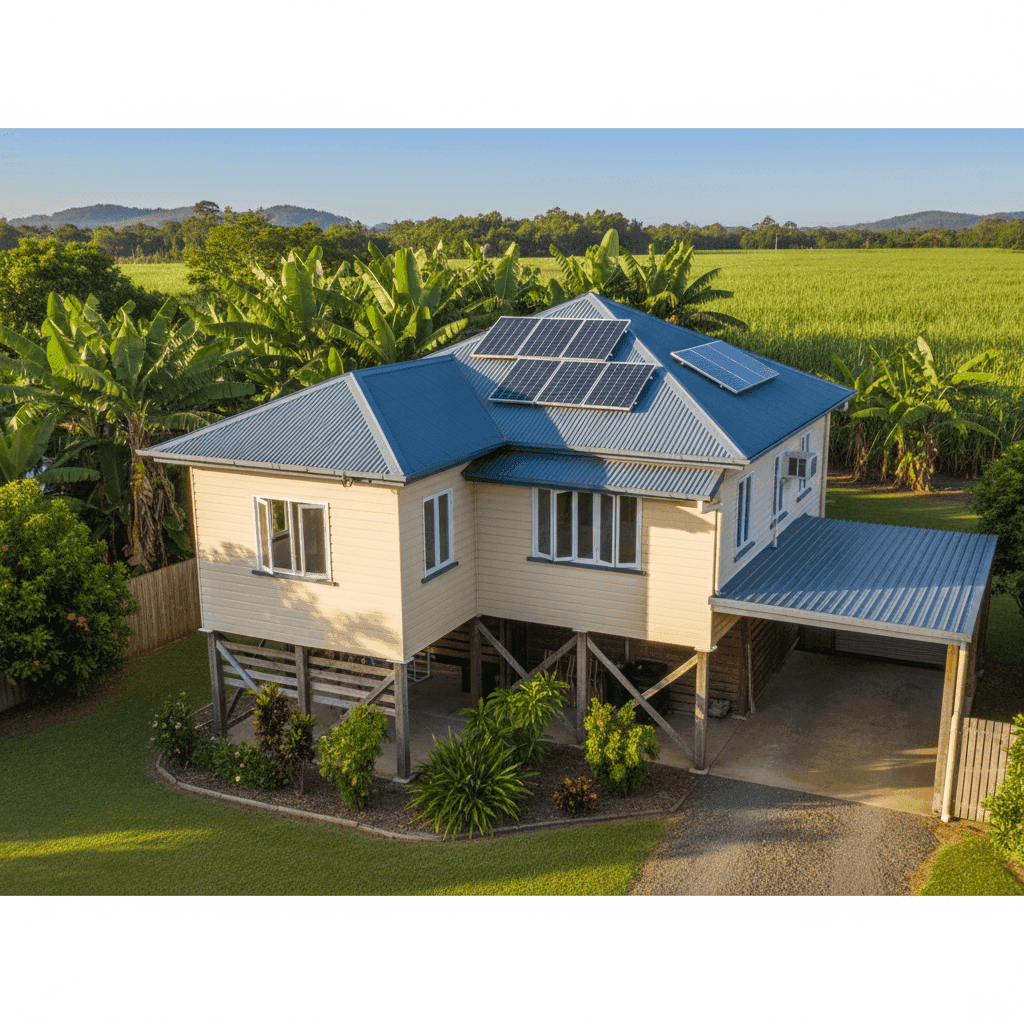

Cyclone Risk Area Silkwood is located in a cyclone-prone region of Far North Queensland. This is the single biggest driver of elevated premiums in this postcode. Insurers apply significant loadings to properties in cyclone zones, regardless of individual property quality.

Age of Construction (1930) At nearly 100 years old, this home is well beyond what most insurers consider "modern construction." Older homes carry higher rebuild risk — ageing plumbing, wiring, and structural elements can all contribute to more costly claims.

Weatherboard Timber Walls Timber weatherboard is considered a higher-risk wall material compared to brick or rendered masonry. It's more susceptible to fire, moisture damage, and wind-driven rain — all of which are particularly relevant in a tropical, cyclone-prone climate.

Stump Foundation Homes on stumps (a classic Queenslander feature) can be more vulnerable to underfloor flooding and storm damage. However, as noted below, elevation also carries a benefit.

🟢 Factors That May Reduce Risk (and Cost)

Elevated By At Least 1 Metre Being elevated is a genuine advantage in flood-prone areas. Many insurers offer more favourable terms to homes raised off the ground, as it significantly reduces the risk of inundation damage — a major claims driver in the wet tropics.

Steel/Colorbond Roof Colorbond roofing is generally regarded as more cyclone-resilient than older tile or fibrous cement roofs. It's a positive attribute in a high-wind risk area.

Solar Panels Solar panels add replacement value and are typically included in the building sum insured. Their presence is noted but unlikely to be a major pricing factor on a standard residential policy.

Ducted Climate Control Ducted air conditioning adds to the insured value of the home but is standard in many QLD properties and generally priced in without dramatic impact.

Small Property Footprint (85 sqm) At 85 square metres, this is a compact home. A lower building size generally correlates with a lower rebuild cost, which may help keep the sum insured — and therefore the premium — more manageable.

---

Tips for Homeowners in Silkwood

If you own or are considering insuring a property in Silkwood, here are some practical steps to get the best outcome:

1. Review Your Sum Insured Regularly Construction costs in regional Queensland have risen sharply in recent years. A $270,000 building sum insured may be appropriate now, but it's worth reassessing annually to ensure you wouldn't be underinsured in the event of a total loss. Use a building cost calculator or speak with a local builder to sense-check the figure.

2. Ask About Cyclone Excess Separately Many insurers in cyclone-prone areas apply a separate cyclone excess on top of the standard building excess. This isn't always clearly disclosed upfront. Make sure you understand exactly what you'd pay out-of-pocket if a cyclone event triggered a claim — it can be significantly higher than the standard $2,000 excess listed here.

3. Maintain Your Home's Cyclone Resilience Insurers and loss assessors pay close attention to roof fixings, guttering, and structural connections when assessing cyclone claims. Regular maintenance — including checking that roof screws are secure, gutters are clear, and any loose structures (like pergolas or garden sheds) are properly anchored — can both reduce claim risk and support your case if you ever need to lodge one.

4. Don't Over-Insure Contents in a Small Home With a 1-bedroom, 85 sqm property, a $20,000 contents sum may be appropriate — but it's worth doing a proper contents inventory to avoid paying for cover you don't need. Equally, make sure high-value items like electronics or jewellery are specifically listed if they exceed standard sublimits.

---

Compare Quotes and Find the Right Cover

Whether this quote is right for your situation depends on more than just the price. Coverage terms, cyclone-specific conditions, and claim handling reputation all matter. The good news is that comparing is easier than ever — get a home insurance quote at CoverClub to see how different insurers price your property and what's included in the fine print. A cheap premium is only valuable if the policy actually pays out when you need it.