Skennars Head is a relaxed coastal community nestled between Ballina and Lennox Head on the NSW Far North Coast — and like many beachside suburbs, it comes with its own unique insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in the area, helping you understand what's driving the price and whether it stacks up against the market.

---

Is This Quote Fair?

The annual premium for this property came in at $5,365 per year (or $514/month), covering a building sum insured of $814,000 and contents valued at $98,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average for Skennars Head sits at just $2,696 per year, with a median of $2,647. This quote lands nearly double the local median, which is a significant gap worth unpacking.

That said, context matters. The building sum insured of $814,000 is likely higher than many comparable properties in the area, and a larger insured value directly lifts the premium. The contents cover of $98,000 adds further to the base cost. If the sum insured reflects the true rebuild cost of this home — which, at 214 sqm with quality fittings and modern construction, it very well might — then the higher premium has a logical foundation.

Still, being above average is a signal worth taking seriously. It's worth comparing quotes across multiple insurers to make sure you're not overpaying for the same level of protection.

---

How Skennars Head Compares

Here's how this quote sits relative to broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Skennars Head (suburb) | $2,696/yr | $2,647/yr |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Ballina LGA | $23,241/yr | — |

A few things stand out here. The NSW state average of $9,528 is heavily skewed by high-risk and high-value properties across the state — the median of $3,770 is a much more reliable indicator of what typical NSW homeowners pay. Compared to the state median, this quote of $5,365 is above average but not dramatically so.

At the national level, the average premium is $5,347 — almost identical to this quote — while the national median sits at $2,764. This reinforces that the quote is on the higher end, but not unusual for a well-insured coastal property.

The Ballina LGA average of $23,241 looks alarming at first glance, but this figure is likely skewed by a small number of very high-value or high-risk properties and shouldn't be taken as a typical benchmark. The suburb-level data from Skennars Head's 55-quote sample is a far more reliable comparison point.

---

Property Features That Affect Your Premium

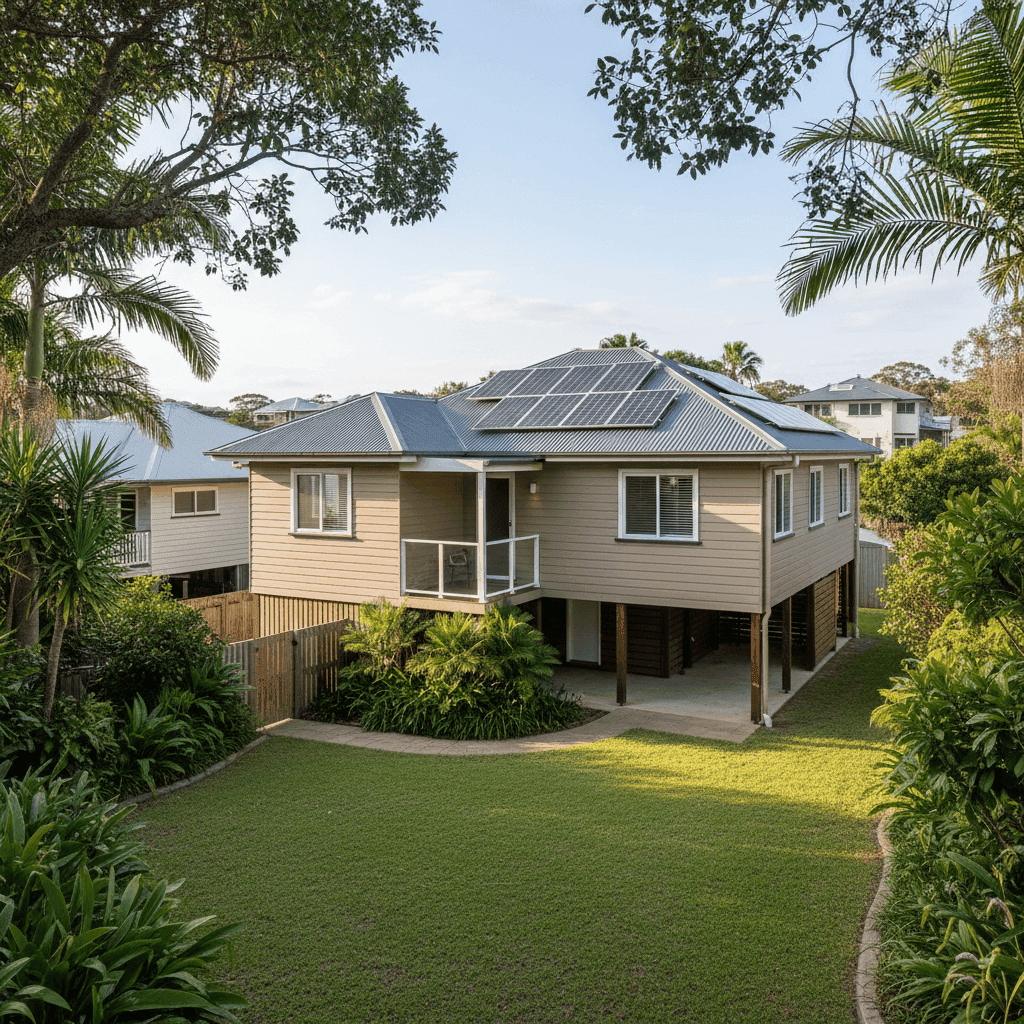

Several characteristics of this property have a direct bearing on the premium quoted:

Weatherboard timber walls are a key risk factor for insurers. Timber-clad homes are more susceptible to fire spread and can be more costly to repair or rebuild than brick veneer or double-brick construction. This typically results in a higher base premium.

Stump foundations are common in coastal and flood-prone areas of northern NSW and can be viewed as a positive or negative depending on the insurer. On one hand, stumps allow airflow and can reduce flood damage to the main structure. On the other, they may indicate an older or more complex build, which some insurers price conservatively.

Timber and laminate flooring is generally considered a standard risk, though it can be costlier to repair after water ingress compared to tile.

Solar panels are an increasingly common inclusion in home insurance, but they do add to the insured value of the property. Panels need to be covered for storm damage, hail, and accidental breakage — all of which contribute to a slightly higher premium.

Ducted climate control is another high-value fixture that increases the overall replacement cost of the home. Systems like these are expensive to repair or replace and are factored into building sum insured calculations.

The 2011 construction year is a positive signal for insurers. Homes built after 2000 generally meet more stringent building codes, particularly around cyclone and storm resistance — relevant even in areas not formally classified as cyclone zones. This property is not in a designated cyclone risk area, which also helps keep the premium lower than it might otherwise be in the broader northern NSW region.

---

Tips for Homeowners in Skennars Head

1. Review your building sum insured annually Construction costs in regional coastal NSW have risen sharply in recent years. Make sure your $814,000 sum insured still reflects the true cost to rebuild — not just the market value of the land and home. Underinsurance is a serious risk, but overinsurance means you're paying more premium than necessary.

2. Compare quotes across multiple insurers With this quote rated as above average, it's worth shopping around. Insurers assess timber-clad, stump-foundation homes differently, and you may find a materially lower premium for equivalent cover. Get a quote through CoverClub to compare options side by side.

3. Ask about discounts for security and safety features Some insurers offer discounts for homes with monitored alarm systems, deadbolts, or fire-resistant upgrades. If you've made any improvements since the policy was last reviewed, it's worth flagging these with your insurer.

4. Consider your excess carefully Both the building and contents excess are set at $1,000. Opting for a higher excess — say $2,500 or $5,000 — can meaningfully reduce your annual premium. If you have the savings to cover a larger out-of-pocket cost in the event of a claim, this can be a smart trade-off.

---

Ready to Compare?

Whether you're renewing your existing policy or shopping for the first time, it pays to see what else is on the market. CoverClub makes it easy to compare home and contents insurance quotes for properties across Skennars Head and the broader Ballina region. Start your comparison today and make sure your home is protected at a price that makes sense.

For more local data, explore the Skennars Head insurance stats page or browse NSW-wide benchmarks to see how your suburb stacks up.