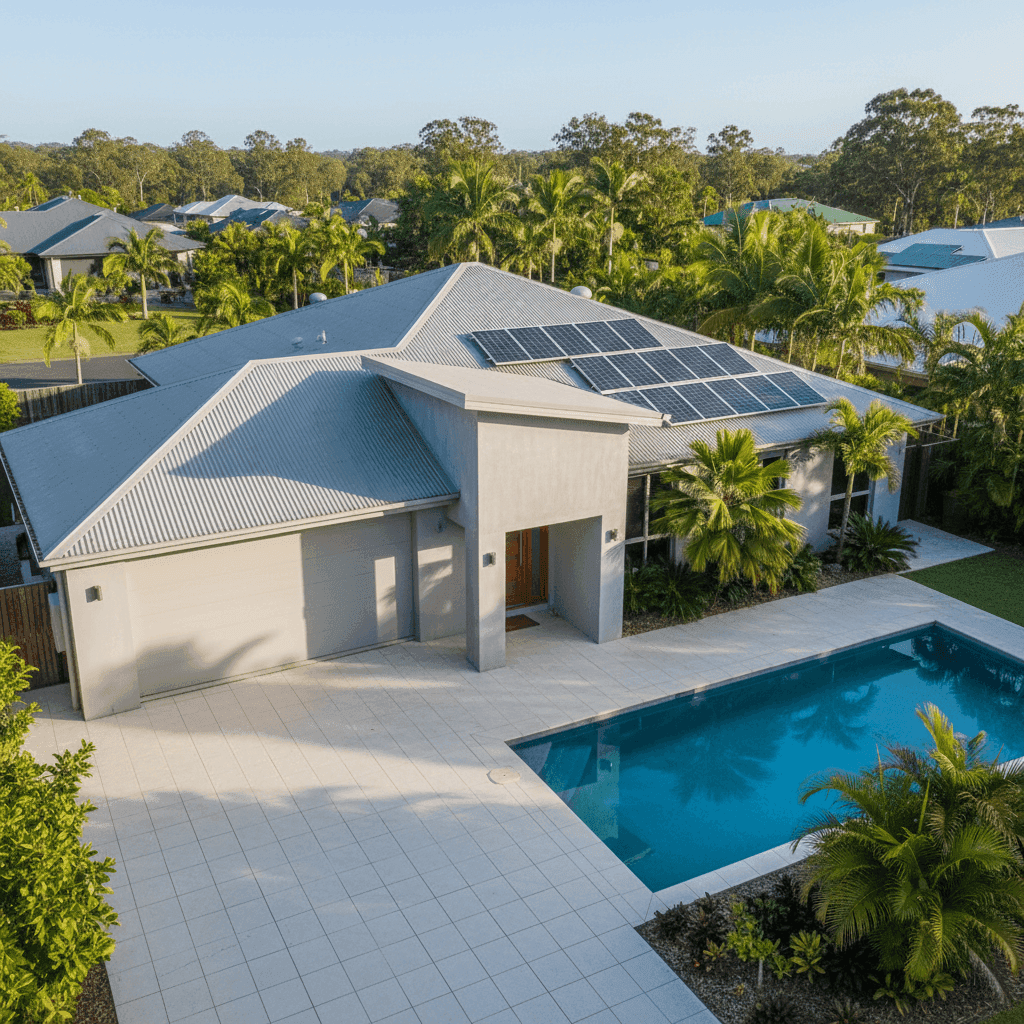

Smithfield is a leafy suburb on the northern outskirts of Cairns, popular with families for its proximity to James Cook University, the Smithfield Shopping Centre, and the stunning rainforest hinterland. It's also a suburb where home insurance premiums deserve careful attention — sitting as it does within a designated cyclone risk zone and the broader Cairns Local Government Area (LGA), where average premiums are among the highest in the country. This article breaks down a recent building-only insurance quote for a three-bedroom, three-bathroom free-standing home in Smithfield, and puts the numbers into context so you can make a more informed decision about your own cover.

---

Is This Quote Fair?

The quoted annual premium of $3,422 (or $328/month) for building-only cover on a $353,000 sum insured has been rated Fair — Around Average. That's a reasonable assessment when you look at the local data.

The suburb average for Smithfield (4878) sits at $3,596 per year, with a median of $3,374. This quote lands almost exactly between those two figures — close enough to the median to be considered competitive, yet below the suburb average. In practical terms, you're not getting a bargain, but you're also not being overcharged relative to what most Smithfield homeowners are paying.

The building excess of $2,000 is worth noting. A higher excess generally reduces your premium, so if this policy were structured with a lower excess, the annual cost could be meaningfully higher. That's an important lever to understand when comparing quotes side by side.

---

How Smithfield Compares

To truly appreciate where this quote sits, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This quote | $3,422/yr |

| Smithfield suburb average | $3,596/yr |

| Smithfield suburb median | $3,374/yr |

| Smithfield 25th percentile | $2,432/yr |

| Smithfield 75th percentile | $4,435/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Cairns LGA average | $12,404/yr |

A few things stand out immediately. The QLD state average of $9,129 per year looks alarming at first glance, but it's heavily skewed by extremely high-risk coastal and far-north Queensland properties — the kind of outliers that pull averages well above the median. The state median of $3,903 is a far more representative figure, and this quote sits comfortably below it.

Similarly, the national average of $5,347 is distorted by high-premium regions, while the national median of $2,764 reflects the reality for lower-risk areas in southern states. Smithfield homeowners will almost always pay more than the national median simply due to cyclone exposure — so a premium in the low-to-mid $3,000s is genuinely reasonable for this location.

Perhaps the most striking figure is the Cairns LGA average of $12,404 per year. This is a stark reminder that within the same local government area, premiums can vary enormously depending on exact location, construction type, and insurer. A quote of $3,422 in this context looks quite favourable.

The 25th–75th percentile range for Smithfield ($2,432–$4,435) gives a useful sense of the spread. This quote falls in the lower half of that middle band — meaning roughly half of comparable Smithfield properties are paying more. Based on a sample of 40 quotes, that's a meaningful data set for a suburb of this size.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted.

Cyclone risk area: This is the single biggest factor. Smithfield falls within a designated cyclone risk zone, which insurers price carefully. Cyclone cover typically comes with specific sub-limits and conditions, and it's one reason why far-north Queensland premiums are structurally higher than the rest of the country.

Concrete external walls: This is actually a premium-reducing feature. Concrete construction is highly resistant to wind, fire, and impact damage — all key perils in this region. Compared to timber-framed homes, concrete-walled properties are generally viewed more favourably by underwriters.

Steel/Colorbond roof: Another resilient choice. Colorbond roofing performs well in high-wind events and is resistant to corrosion in the humid, tropical climate of Cairns. It's a common and practical choice for the region.

Slab foundation and tiled flooring: Both are low-maintenance, durable choices that reduce the likelihood of claims related to subfloor moisture or flooring damage. Slab foundations are standard in this part of Queensland and present minimal additional risk.

Swimming pool: Pools add to the replacement cost of a property and can introduce liability considerations. Insurers factor this into the sum insured and overall risk profile.

Solar panels: Rooftop solar adds to the rebuilding cost and introduces some risk around electrical systems and storm damage. It's worth confirming with your insurer that panels are explicitly covered under your building policy.

Ducted climate control: A ducted system is a significant built-in asset. Like solar panels, it contributes to the overall replacement value and should be accounted for in your sum insured calculation.

214 sqm building size and standard fittings: At 214 square metres with standard-quality fittings, the $353,000 sum insured works out to roughly $1,649 per square metre — a reasonable estimate for concrete construction in regional Queensland, though it's always worth verifying this against current building cost data for your area.

---

Tips for Homeowners in Smithfield

1. Review your sum insured annually. Building costs in Queensland have risen significantly in recent years due to labour shortages and material costs. A sum insured that was accurate in 2022 may leave you underinsured today. Use a building cost calculator or speak with a quantity surveyor to ensure your coverage reflects current rebuild costs — not just the original construction price.

2. Check your cyclone-specific policy conditions. Not all home insurance policies treat cyclone damage the same way. Some policies have separate cyclone excess amounts (often calculated as a percentage of the sum insured rather than a flat dollar figure), waiting periods, or exclusions for certain types of damage. Read the Product Disclosure Statement carefully and ask your insurer directly about cyclone cover terms.

3. Confirm that solar panels and ducted systems are covered. These are significant assets that are sometimes excluded or sub-limited under standard building policies. Ask your insurer explicitly whether rooftop solar panels (including inverters) and ducted air conditioning systems are covered, and for how much.

4. Compare quotes before your renewal date. The 40-quote sample for Smithfield shows a wide premium range — from $2,432 at the 25th percentile to $4,435 at the 75th. That's a $2,000 annual difference for broadly similar properties. Shopping around at renewal time is one of the most effective ways to ensure you're not paying more than you need to.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the smartest move you can make. Get a home insurance quote at CoverClub and see how your premium stacks up against what other Smithfield homeowners are paying. You can also explore detailed suburb-level insurance statistics for Smithfield 4878 to benchmark your own cover with confidence.