South Grafton is a well-established residential suburb on the southern bank of the Clarence River in northern New South Wales. It's home to a mix of older character properties and more modern builds, and like much of regional NSW, home insurance costs here can vary significantly depending on a property's age, construction, and risk profile. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in South Grafton (NSW 2460), examines how it stacks up against local, state, and national benchmarks, and offers practical guidance for homeowners in the area.

---

Is This Quote Fair?

The annual premium for this property came in at $1,970 per year (or around $198 per month), covering both building (sum insured: $781,000) and contents ($50,000). Our pricing analysis rates this quote as CHEAP — below average — and it's easy to see why.

To put it in perspective:

- The suburb average for South Grafton is $4,278/yr, meaning this quote is less than half what many locals are paying.

- Even the 25th percentile — the cheapest quarter of quotes in the area — sits at $2,297/yr, which is still well above this premium.

- At the state level, the average NSW home and contents premium is $3,801/yr, and nationally the figure sits at $2,965/yr.

By any measure, this is a competitive result. The building excess of $3,000 is on the higher side (which does help reduce the premium), while the contents excess of $1,000 is fairly standard. Homeowners who can comfortably absorb a larger out-of-pocket cost in the event of a claim will often find that accepting a higher excess is a smart way to keep ongoing premiums down.

---

How South Grafton Compares

Understanding where South Grafton sits in the broader insurance landscape is useful context for any homeowner in the area. According to data from CoverClub's South Grafton suburb stats, based on a sample of 34 quotes:

| Benchmark | Premium |

|---|---|

| South Grafton 25th percentile | $2,297/yr |

| South Grafton median | $3,261/yr |

| South Grafton average | $4,278/yr |

| South Grafton 75th percentile | $5,385/yr |

| NSW average | $3,801/yr |

| National average | $2,965/yr |

One figure that stands out is the Richmond Valley LGA average of $7,188/yr — considerably higher than the South Grafton suburb average. This suggests that while South Grafton itself sits in a more moderate risk zone within the LGA, other parts of the Richmond Valley — particularly those with greater flood or storm exposure — are driving up that regional figure substantially.

You can explore broader NSW home insurance statistics and national benchmarks to see how your own property compares across different geographies.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in its favour from an insurance pricing perspective — and a few introduce considerations worth being aware of.

Double Brick Construction

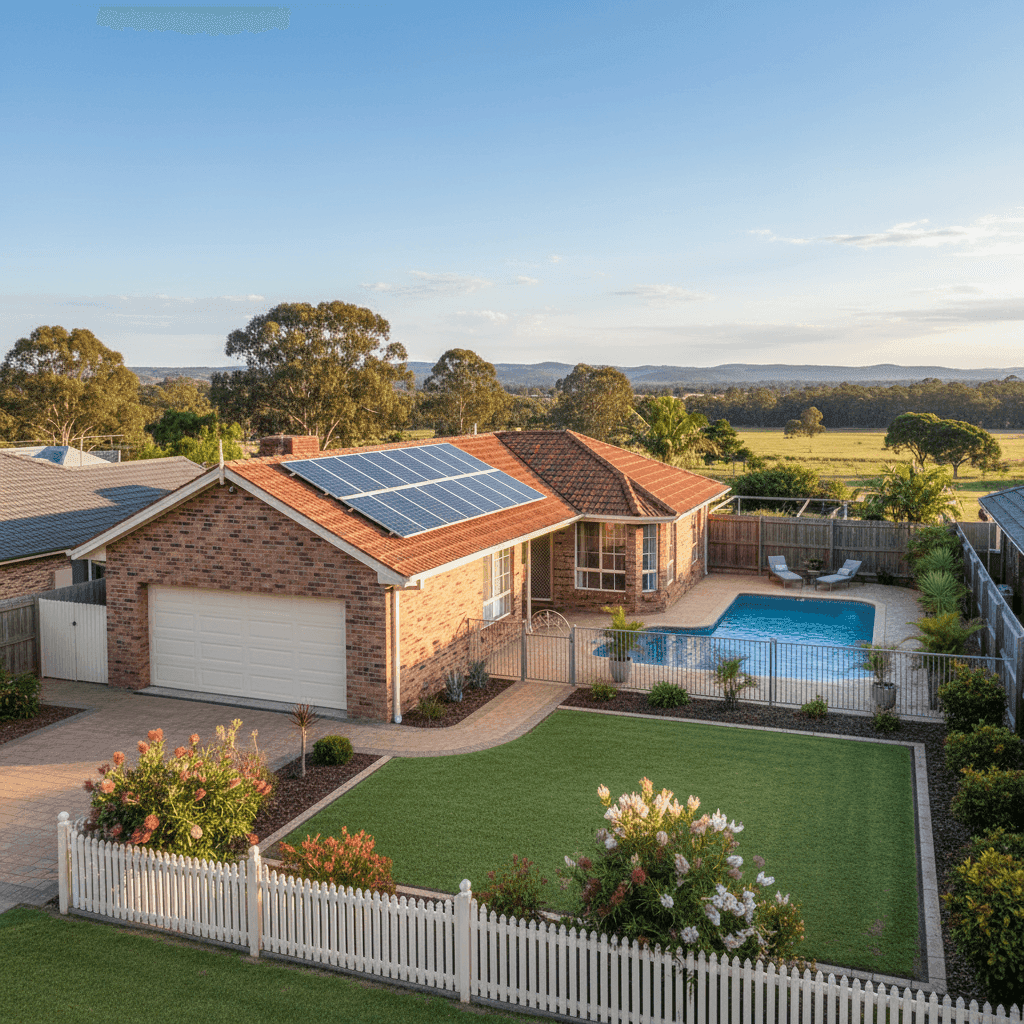

Double brick is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to structural damage than timber-framed homes. For a home built in 1985, double brick construction also means the building has likely aged well and is less prone to the kind of deterioration that can affect other wall types.

Tiled Roof

Terracotta or concrete tiles are among the more resilient roofing materials available. They perform well in storms and have a long lifespan, which reduces the likelihood of weather-related claims — a key factor in premium calculations.

Stump Foundation

The property sits on stumps, which is common for homes of this era in northern NSW. While stumped foundations offer good ventilation and some flexibility in flood-prone areas, insurers may assess them differently depending on the specific flood risk of the location. It's worth confirming your policy covers damage to the subfloor structure.

Swimming Pool

A pool adds to the replacement cost of the property and is factored into the building sum insured. It also introduces some liability considerations. Make sure your policy adequately covers pool-related structures (fencing, pumps, filtration systems) and that your liability cover is sufficient.

Solar Panels

Solar panels are increasingly common on Australian rooftops, but they're not always automatically covered under standard building policies. It's important to confirm that your insurer includes solar panels as part of the building sum insured — or whether they need to be listed separately.

Vinyl Flooring

Vinyl is a practical, cost-effective flooring choice that's relatively straightforward to replace. It doesn't significantly inflate the building sum insured the way premium hardwood or stone flooring might.

Building Size and Sum Insured

At 214 sqm and a building sum insured of $781,000, the per-square-metre rebuild cost works out to roughly $3,650/sqm — a reasonable figure for a double brick home in regional NSW, though homeowners should periodically review this to ensure it keeps pace with rising construction costs.

---

Tips for Homeowners in South Grafton

1. Review your sum insured annually Construction costs across Australia have risen sharply in recent years. A sum insured that was accurate two or three years ago may no longer reflect the true cost to rebuild your home. Underinsurance is a significant risk — if your home is destroyed and the payout doesn't cover the full rebuild, you'll be out of pocket for the difference.

2. Confirm solar panel and pool coverage These are two features that can easily fall through the cracks in a standard policy. Before renewing, ask your insurer specifically whether solar panels are covered as part of the building and what pool-related structures are included. Get it in writing.

3. Consider your flood risk South Grafton sits near the Clarence River, and parts of the suburb have experienced flooding historically. Check whether your policy includes flood cover (not just storm or rainwater damage) and whether your specific property falls within a mapped flood zone. Some insurers exclude or heavily load premiums for flood-prone addresses.

4. Shop around at renewal time This quote demonstrates that there's a wide spread of premiums available in South Grafton — from under $2,300 at the cheaper end to over $5,385 at the top of the range. Loyalty doesn't always pay in insurance. Comparing quotes annually is one of the simplest ways to avoid overpaying.

---

Compare Your Own Quote

Whether you're renewing soon or just curious about what you should be paying, CoverClub makes it easy to benchmark your premium against real data from your suburb and beyond. Get a home insurance quote today and see how your current cover stacks up — you might be surprised by what's available.