South Hedland is a residential suburb of the Port Hedland local government area in the Pilbara region of Western Australia — and if you own a free standing home here, you already know that insurance isn't cheap. Cyclone season, remote location, and the cost of rebuilding in a regional mining town all push premiums well above what most Australians pay. That makes it all the more important to understand exactly what you're paying, and whether the quote in front of you is genuinely competitive.

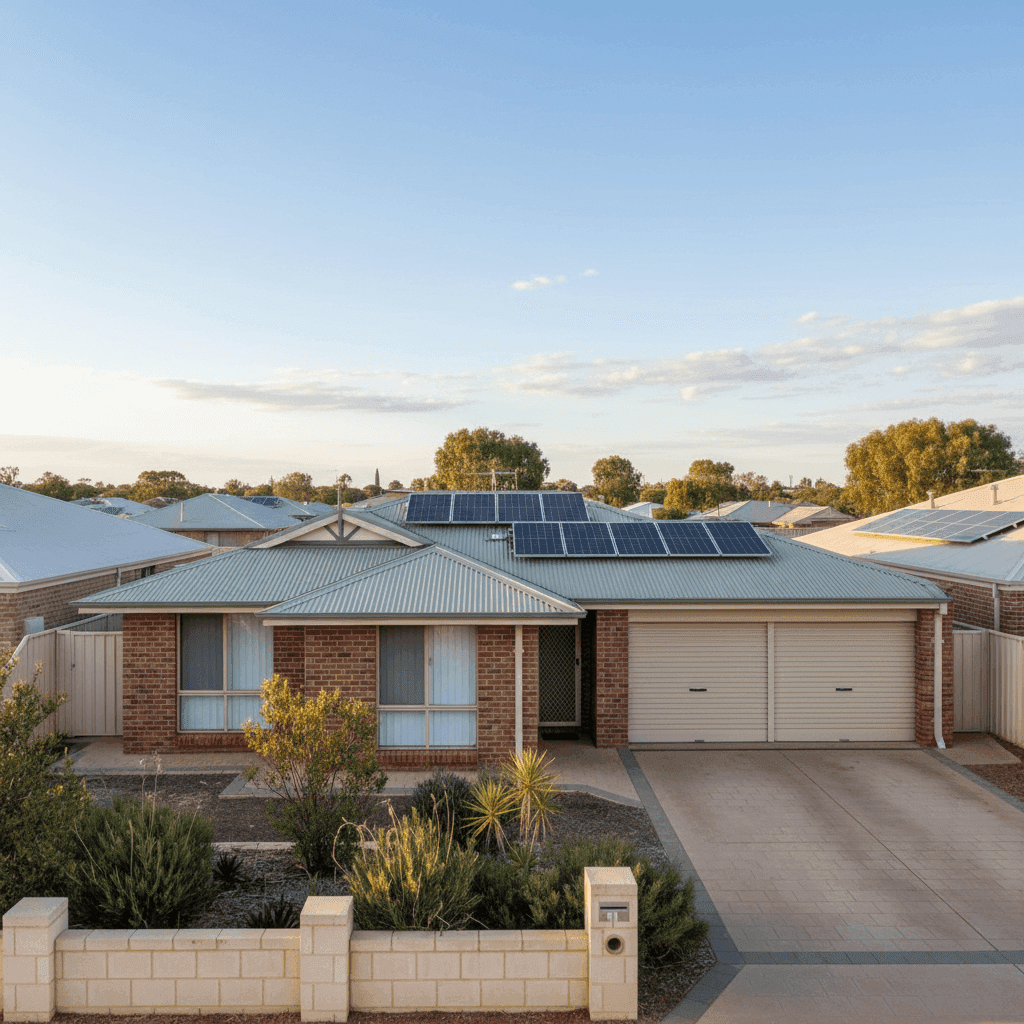

This article breaks down a real home and contents insurance quote for a 4-bedroom, 1-bathroom free standing home in South Hedland (postcode 6722), built in 1986 with brick veneer walls and a Colorbond steel roof. The building is insured for $520,000 with $50,000 in contents cover, carrying a $1,000 excess on each. The annual premium comes in at $4,383 (or roughly $413 per month).

---

Is This Quote Fair?

In short — yes, and then some. This quote has been rated CHEAP, meaning it sits well below the average for the area. Based on a sample of 45 quotes collected for South Hedland (postcode 6722), the suburb average premium is $7,643 per year and the median sits at $6,892 per year. Even the cheapest quarter of quotes in the area (the 25th percentile) come in at around $6,166 per year.

At $4,383 annually, this quote is approximately $2,509 below the suburb median — a saving of around 36%. That's a meaningful difference, particularly given the relatively high sum insured of $520,000 for the building alone. Homeowners in South Hedland who haven't shopped around recently may well be paying thousands more than they need to.

You can explore the full pricing data for this suburb at the South Hedland insurance stats page.

---

How South Hedland Compares

To put this quote in broader context, it helps to look beyond the suburb and compare against state and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| South Hedland (6722) | $7,643/yr | $6,892/yr |

| Western Australia | $2,811/yr | $2,127/yr |

| Australia (National) | $5,347/yr | $2,764/yr |

A few things stand out here. South Hedland premiums are nearly three times the Western Australian state average, which reflects the outsized impact of cyclone risk and regional rebuild costs on pricing in the Pilbara. Interestingly, South Hedland also sits above the national average of $5,347 per year — a figure that itself is inflated by high-risk areas across the country.

The national median of $2,764 gives perhaps the clearest picture: the typical Australian homeowner pays less than half what South Hedland residents are quoted. This isn't a reflection of poor value — it's simply the reality of insuring property in a cyclone-prone, remote region where construction and repair costs are significantly elevated.

Explore WA home insurance statistics or national home insurance data to see how your own premium stacks up.

---

Property Features That Affect Your Premium

Several characteristics of this particular property will influence how insurers assess and price the risk.

Cyclone Risk Area This is the single biggest premium driver in South Hedland. The Pilbara sits within a recognised cyclone risk zone, and insurers price this in heavily. Policies in these areas often include specific cyclone-related conditions, higher excesses for storm damage, or separate cyclone sub-limits. It's essential to read the Product Disclosure Statement (PDS) carefully to understand exactly what's covered during a cyclone event.

Brick Veneer Construction with Colorbond Roof Brick veneer is a common construction type in Australian suburban homes and is generally viewed favourably by insurers — it offers solid fire resistance and reasonable structural durability. A Colorbond steel roof is well-suited to the harsh Pilbara climate, offering good resistance to heat, corrosion, and wind uplift. Together, these materials present a relatively low-risk construction profile.

Age of the Property (1986) At nearly 40 years old, this home is approaching an age where insurers may factor in the likelihood of older plumbing, wiring, or structural components needing attention. Keeping up with maintenance and being able to demonstrate the home is well-cared-for can help avoid complications at claim time.

Solar Panels The presence of solar panels adds a layer of complexity to home insurance. Panels need to be included in the sum insured or covered under a specific provision, as they can be costly to replace — particularly if damaged during a cyclone or severe storm. It's worth confirming with your insurer whether panels are covered under the building policy and to what limit.

Ducted Climate Control Ducted air conditioning is a significant fixed asset in a home. Like solar panels, it should be factored into your building sum insured to avoid being underinsured in the event of a total loss or major damage.

Slab Foundation Slab-on-ground foundations are standard in WA and generally straightforward for insurers to assess. There's no elevated subfloor that could be vulnerable to flooding or pest damage, which is a modest positive from a risk perspective.

---

Tips for Homeowners in South Hedland

1. Review your sum insured annually Building costs in regional WA — especially in a mining hub like Port Hedland — can rise quickly. With a sum insured of $520,000, it's important to ensure this figure reflects the true cost of rebuilding your home from scratch, including labour, materials, and any site-specific costs like debris removal. Underinsurance is a serious risk and one of the most common issues at claim time.

2. Understand your cyclone excess Many policies in cyclone-prone areas apply a separate, higher excess specifically for cyclone or storm damage claims. This can be $2,500, $5,000, or more — quite different from the standard $1,000 excess on this policy. Make sure you know what you'd actually be out of pocket if a cyclone caused significant damage.

3. Check your solar panels are covered Confirm in writing with your insurer that your solar panel system is included in your building cover and up to what value. If the system has been upgraded or expanded since the policy was first taken out, it may be worth getting a current valuation and updating your policy accordingly.

4. Compare quotes at renewal time Given that this quote came in well below the suburb average, it's clear that premiums in South Hedland can vary enormously between insurers. Don't assume your renewal price is competitive — shopping around at each renewal can potentially save you thousands of dollars per year.

---

Compare Your Own Quote

Whether you're buying, renewing, or just curious about what you should be paying, CoverClub makes it easy to compare home and contents insurance quotes for properties across Australia — including high-risk areas like South Hedland. Get a quote today and see how your premium stacks up against real data from your suburb, your state, and the national average.