If you own a free standing home in South Kempsey, NSW 2440, you already know that finding the right home insurance can feel like navigating a maze. Premiums vary enormously depending on your property's characteristics, location risk profile, and the insurer you choose. In this article, we break down a real home and contents insurance quote for a 3-bedroom, 2-bathroom property in South Kempsey — and help you understand whether it represents fair value.

---

Is This Quote Fair?

The quote in question comes in at $7,370 per year (or $699/month) for combined home and contents cover, with a building sum insured of $704,000 and contents valued at $100,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is Expensive — above average.

To put that in perspective, the average premium paid by homeowners in the South Kempsey suburb sits at just $2,422 per year, with the 75th percentile reaching only $2,543. That means this quote is nearly three times the local suburb average — a significant gap that warrants a closer look.

It's worth noting, however, that the suburb sample size is relatively small (15 quotes), so local averages may not capture the full spectrum of property types and risk profiles in the area. Higher sums insured, older construction, and specific building materials can all push premiums well above the suburb median.

---

How South Kempsey Compares

Understanding where a premium sits relative to broader benchmarks is key to evaluating its fairness. Here's how South Kempsey stacks up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| South Kempsey (suburb) | $2,422/yr | $2,422/yr |

| Port Macquarie-Hastings LGA | $7,001/yr | — |

| NSW (state) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. While the suburb average looks low, the LGA average for Port Macquarie-Hastings is $7,001/yr — much closer to the quoted premium of $7,370. This suggests that when you zoom out from the suburb to the broader local government area, this quote starts to look more in line with what other homeowners in the region are paying.

The NSW state average of $9,528 is heavily skewed upward by high-value and high-risk properties, which is why the state median of $3,770 is a more reliable reference point. Similarly, the national average of $5,347 is pulled up by outliers, while the national median sits at $2,764.

You can explore local pricing trends in more detail on the South Kempsey suburb stats page, compare against the NSW state overview, or check out national home insurance benchmarks.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the elevated premium. Here's a breakdown of the key factors at play:

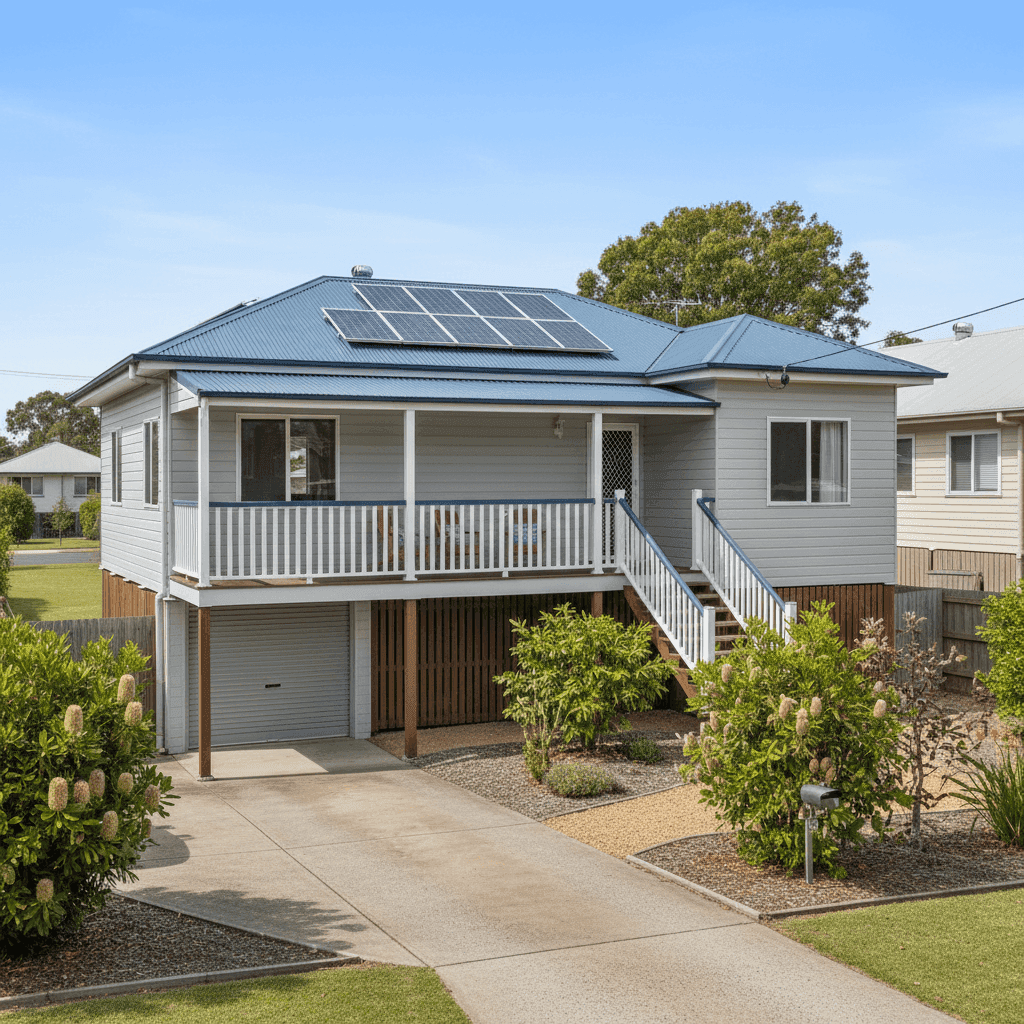

Building Age and Construction Materials

Built in 1985, this home is approaching 40 years old. Older properties often attract higher premiums due to the increased likelihood of wear-related claims — think ageing plumbing, electrical systems, and structural components. The Hardiplank/Hardiflex external walls are a fibre cement cladding product that performs reasonably well in terms of fire resistance, but can be more costly to repair or replace than brick veneer, which may influence the insurer's pricing model.

Roof Type

The steel/Colorbond roof is a popular and durable choice across regional NSW. Colorbond is generally well-regarded by insurers for its resilience in moderate weather conditions, though it can be susceptible to hail damage — a relevant consideration in the Macleay Valley region.

Elevated Foundation

The home sits on stumps and is elevated by less than 1 metre. While this style of construction — common in older regional Queensland and northern NSW homes — can offer some protection against minor flooding, it also introduces specific risks around subfloor maintenance and potential storm-related movement. Elevated homes can sometimes attract slightly higher premiums depending on how the insurer models structural risk.

Solar Panels

This property has solar panels installed, which adds to the replacement cost of the building and is a factor some insurers price into their building sum insured calculations. It's important to ensure your building sum insured adequately covers the cost of reinstating your solar system.

Ducted Climate Control

Ducted climate control is a higher-end fitting that increases the overall replacement value of the home. Standard fittings are noted for this property, but the presence of a ducted system still adds to the insured value.

High Building Sum Insured

At $704,000, the building sum insured is substantial. This figure directly drives premium cost — the more it would cost to rebuild your home from scratch, the more you'll pay to insure it. Ensuring this figure is accurate (neither over- nor under-insured) is one of the most important steps any homeowner can take.

---

Tips for Homeowners in South Kempsey

If you're a homeowner in South Kempsey and you're concerned about the cost of your insurance, here are four practical steps worth considering:

- Review your building sum insured carefully. Use a professional building cost estimator or ask your insurer how they calculated the rebuild cost. Over-insurance is surprisingly common and can add hundreds of dollars to your annual premium unnecessarily.

- Compare quotes from multiple insurers. Premiums for the same property can vary by thousands of dollars between providers. The best way to know whether you're getting a competitive rate is to compare — tools like CoverClub make this straightforward.

- Consider your excess level. Both the building and contents excess on this quote are set at $2,000. Opting for a higher voluntary excess can reduce your annual premium, provided you're comfortable covering that amount out of pocket in the event of a claim.

- Check what's actually covered. Flood cover, accidental damage, and contents away from home are examples of optional extras that can significantly affect your premium. Make sure you're not paying for cover you don't need — or going without cover you do.

---

Get a Better Deal on Your Home Insurance

Whether you're renewing your policy or shopping around for the first time, it pays to compare. Premiums in the Port Macquarie-Hastings region can vary widely, and the difference between the cheapest and most expensive quote for the same property can be thousands of dollars per year.

Compare home insurance quotes at CoverClub — it's free, fast, and designed specifically for Australian homeowners. Enter your address to see how your current premium stacks up against the market.