Nestled in Melbourne's northern growth corridor, South Morang is a well-established suburban community popular with families seeking space and modern amenities. If you own a large free standing home in the area — particularly a six-bedroom property built in the early 2000s — understanding what you should be paying for home and contents insurance is essential. This article breaks down a recent quote of $2,754 per year for a property in South Morang (postcode 3752), comparing it against local, state, and national benchmarks to help you decide whether it stacks up.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated Fair (Around Average), which means it sits in a reasonable range — not a standout bargain, but not overpriced either.

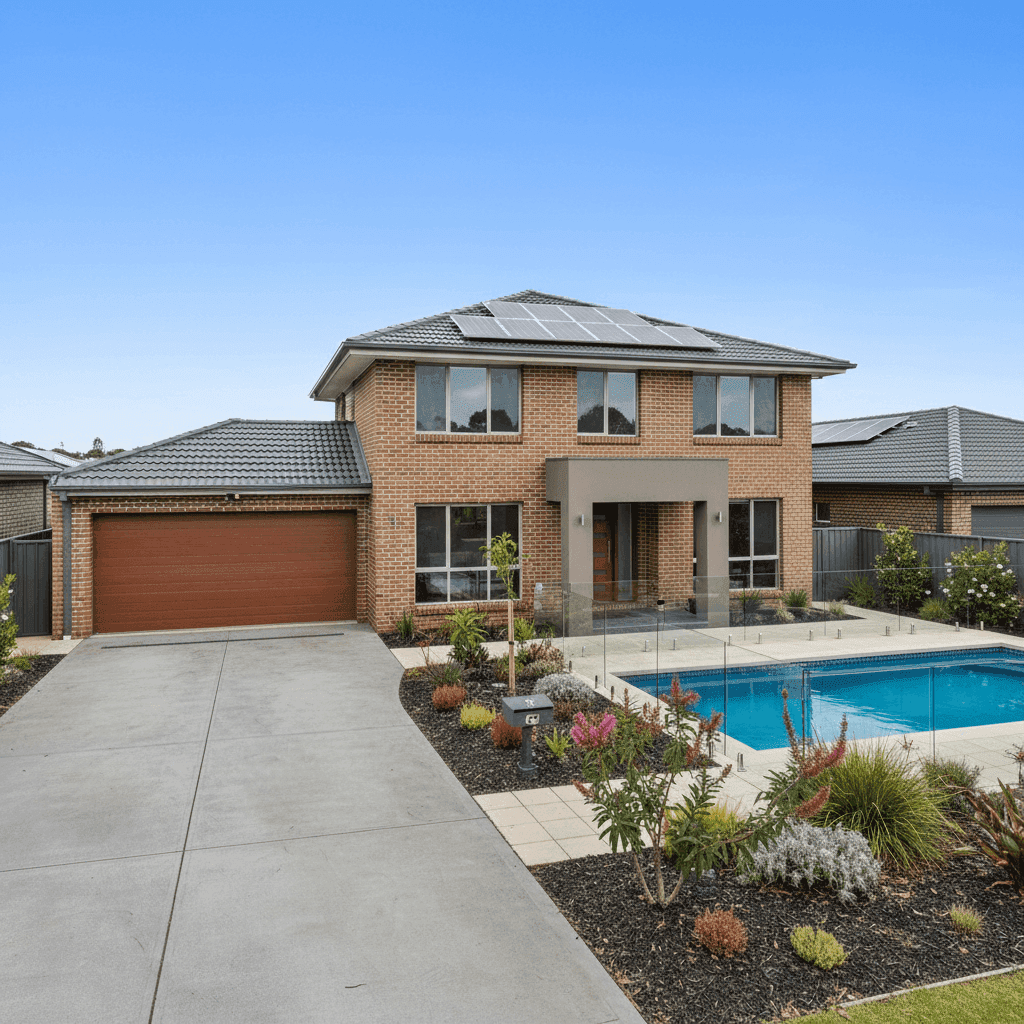

At $2,754 per year (or approximately $257 per month), this premium covers both building (sum insured: $900,000) and contents ($170,000), with a $1,000 excess applying to each. For a 462 sqm home with a pool, solar panels, and ducted climate control, these are meaningful coverage amounts that reflect the true replacement cost of a substantial property.

The "fair" rating is supported by where this quote sits within the local distribution. The suburb's 25th percentile sits at $1,654/yr, while the 75th percentile reaches $3,010/yr — meaning this quote lands comfortably within the middle of the market for South Morang. Homeowners paying less are likely insuring smaller properties, carrying higher excesses, or accepting narrower cover. Those paying more may have higher-value homes or additional risk factors.

---

How South Morang Compares

To put this quote into proper context, it helps to look at the numbers side by side.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| South Morang (3752) | $2,412/yr | $2,433/yr |

| Victoria (VIC) | $2,921/yr | $2,694/yr |

| National | $2,965/yr | $2,716/yr |

| LGA (Whittlesea) | $1,850/yr | — |

A few things stand out here. First, South Morang's average premium of $2,412 is notably lower than both the Victorian average ($2,921) and the national average ($2,965). This suggests the suburb benefits from relatively favourable risk conditions — no cyclone exposure, lower flood risk compared to many coastal or riverine areas, and a predominantly modern housing stock.

Second, the LGA average for Whittlesea ($1,850/yr) is considerably lower than the suburb average. This likely reflects the mix of property sizes and cover levels across the broader council area, where many homes are smaller or carry lower sums insured.

At $2,754/yr, this particular quote sits $342 above the suburb average — but that gap is easily explained by the property's size, features, and the substantial building sum insured of $900,000. Based on 53 quotes sampled in the suburb, this result is consistent with what larger, well-appointed homes in the area typically attract.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Understanding these factors can help you assess whether your cover is appropriately priced.

Size and Sum Insured At 462 sqm with six bedrooms and three bathrooms, this is a large home by any measure. A building sum insured of $900,000 reflects the genuine cost to rebuild a property of this scale, and insurers price accordingly. Larger homes simply cost more to reinstate.

Construction: Brick Veneer and Tiles Brick veneer walls and a tiled roof are among the most common and insurer-friendly construction types in Victoria. They offer solid fire and weather resistance, which generally attracts more competitive premiums compared to timber weatherboard or older construction methods.

Slab Foundation A concrete slab foundation is standard for homes built in this era and is generally viewed positively by insurers. It reduces the risk of subsidence and pest-related structural damage compared to older pier-and-beam foundations.

Swimming Pool The presence of a pool adds to the insured value of the property and introduces some liability considerations. Pool equipment, surrounds, and associated structures all contribute to the overall rebuild cost and can nudge premiums upward.

Solar Panels Solar panels represent a meaningful capital asset — and a potential liability. Insurers consider both the replacement cost of the panels themselves and the risk of roof damage during installation or from weather events. Ensuring your policy explicitly covers solar panels is important.

Ducted Climate Control Ducted heating and cooling systems are expensive to replace and are typically factored into the building sum insured. Their inclusion is another reason why a higher-than-suburb-average premium is entirely reasonable here.

---

Tips for Homeowners in South Morang

1. Review your building sum insured regularly Construction costs have risen significantly in recent years. A sum insured set two or three years ago may no longer reflect the true cost to rebuild your home. Use a building cost calculator or speak to a quantity surveyor to ensure you're not underinsured — especially for a large home like this one.

2. Confirm your solar panels and pool are explicitly covered Not all standard home insurance policies automatically extend full cover to solar panel systems or pool equipment. Read your Product Disclosure Statement (PDS) carefully and ask your insurer to confirm what's included. Gaps in cover here could be costly.

3. Consider your excess strategically A $1,000 excess is fairly standard, but increasing it to $2,000 or more can reduce your annual premium meaningfully. If you have a solid emergency fund and are unlikely to make small claims, a higher excess may offer better value over time.

4. Compare quotes before renewing Loyalty doesn't always pay in insurance. Insurers frequently offer better rates to new customers than to existing ones. Before your renewal date, run a fresh comparison at CoverClub to make sure you're still getting a competitive deal — particularly as your property's circumstances change over time.

---

Find a Better Deal on CoverClub

Whether you're reviewing your current policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up. Get a home insurance quote today and compare real prices for properties in South Morang and across Victoria. With transparent data and suburb-level benchmarks, you'll know exactly where you stand — and whether there's room to do better.