If you own a free standing home in South Nanango, QLD 4615, you've probably noticed that insurance premiums in regional Queensland can feel like a moving target. This article takes a close look at a recent home and contents insurance quote for a two-bedroom, one-bathroom weatherboard home in the area — and breaks down whether the price stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,189 per year (or $299/month) for combined home and contents cover, with a building sum insured of $550,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up.

Looking at suburb-level statistics for South Nanango (QLD 4615), the average premium sits at $2,695/yr and the median at $3,011/yr. This quote of $3,189 lands just above the suburb median, placing it comfortably within the interquartile range — between the 25th percentile of $1,970/yr and the 75th percentile of $3,381/yr. In plain terms, roughly half of comparable quotes in the suburb fall between those two figures, and this one sits well within that band.

So while it's not the cheapest quote available, it's far from an outlier. For a property with several risk-influencing features (more on those shortly), landing near the median is a reasonable outcome.

---

How South Nanango Compares

Context is everything when it comes to insurance pricing, and the numbers here tell an interesting story.

| Benchmark | Premium |

|---|---|

| This Quote | $3,189/yr |

| Suburb Average (South Nanango) | $2,695/yr |

| Suburb Median (South Nanango) | $3,011/yr |

| LGA Average (Gympie) | $5,581/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

A few things stand out immediately. The QLD state average of $9,129/yr is dramatically higher than both the suburb average and this quote — a reflection of just how expensive insurance has become in high-risk coastal and cyclone-prone parts of Queensland. South Nanango, sitting inland in the South Burnett region, benefits from not being in a designated cyclone risk zone, which keeps premiums considerably more grounded.

Compared to the national average of $5,347/yr, this quote is well below the mark — nearly $2,200 cheaper per year. Even against the national median of $2,764/yr, the difference is modest, suggesting this property's risk profile is broadly in line with the typical Australian home.

The Gympie LGA average of $5,581/yr is worth noting too. South Nanango sits within the Gympie Regional Council area, yet this quote comes in at roughly 57% of the LGA average — a meaningful saving that likely reflects the inland location and absence of some high-risk features common elsewhere in the region.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Understanding them helps make sense of the pricing.

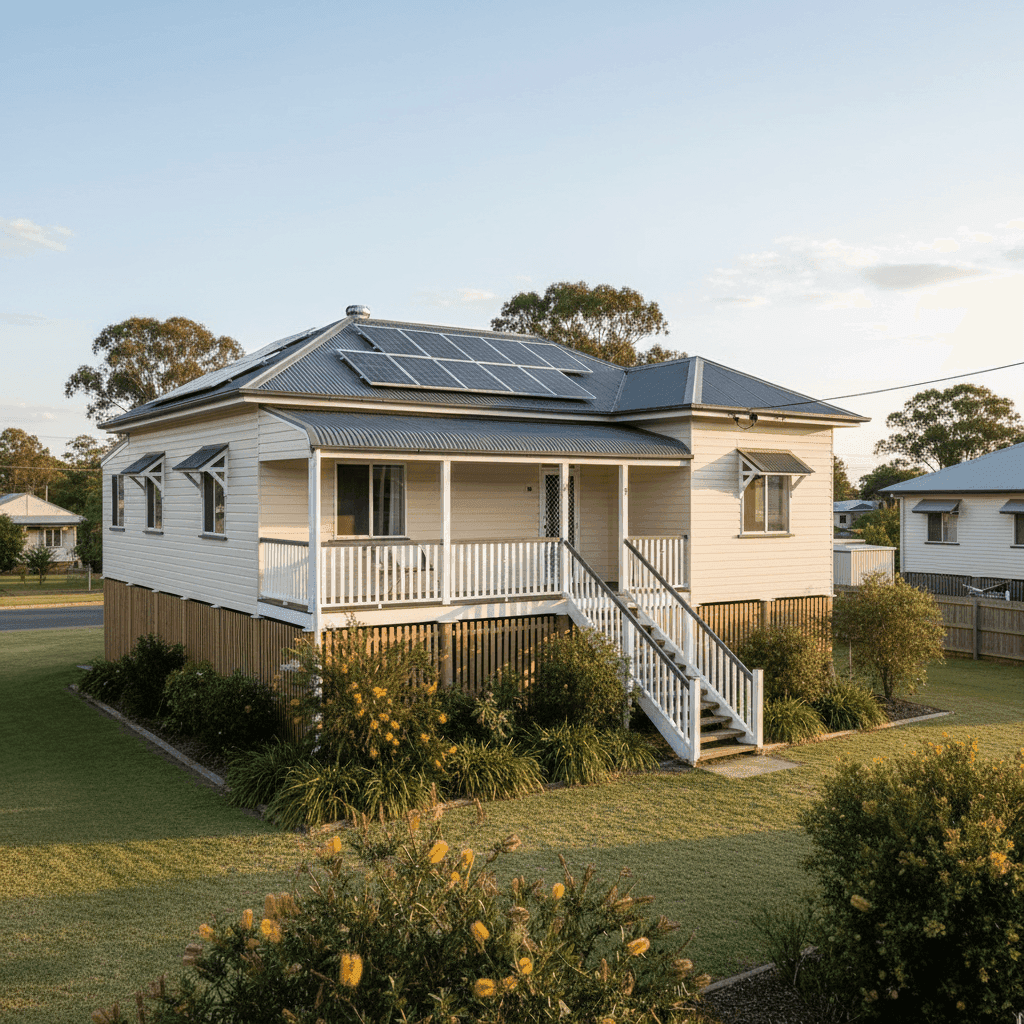

Weatherboard timber construction is one of the most significant factors. Older timber homes — this one was built in 1965 — are generally considered higher risk by insurers due to their susceptibility to fire, rot, and the higher cost of like-for-like repairs. Sourcing matching weatherboards for a heritage-era home isn't cheap, and insurers price that in.

Stump foundations and elevated design add another layer of complexity. Homes elevated by at least one metre (a classic Queenslander trait) can be more expensive to repair after events like storms or flooding, as access and structural work are more involved. That said, elevation also offers some protection against minor flooding, which can work in the homeowner's favour in certain risk assessments.

The 1965 construction year means the home is over 60 years old. Ageing electrical wiring, plumbing, and structural elements are all considerations that can push premiums upward, as the likelihood of a claim — and the cost of repairs — tends to increase with property age.

Solar panels are a positive modern addition, but they do add to the replacement cost of the home. Insurers factor in the cost of reinstating panels after a storm or hail event, which can nudge premiums slightly higher.

Timber and laminate flooring throughout the home is another cost consideration for claims involving water damage or fire, as these materials can be expensive to replace and match.

On the plus side, the absence of a pool removes one liability risk factor, and the property is not located in a cyclone risk zone — a significant saving compared to coastal Queensland properties.

---

Tips for Homeowners in South Nanango

1. Review your sum insured regularly A building sum insured of $550,000 is substantial for a two-bedroom home in South Nanango. Make sure this figure reflects the actual cost to rebuild — not the market value of the property. Overcovering can mean you're paying more in premiums than necessary, while undercovering leaves you exposed at claim time. Use a building cost estimator or speak with a local builder to sense-check the figure.

2. Consider bundling building and contents This quote already combines home and contents cover, which is often more cost-effective than holding two separate policies. If you're currently insuring them separately, it's worth getting a combined quote to see if you can save.

3. Increase your excess to reduce your premium Both the building and contents excess on this policy are set at $1,000. Many insurers will offer a lower annual premium in exchange for a higher voluntary excess. If you're unlikely to make small claims, opting for a $2,000 excess could meaningfully reduce what you pay each year.

4. Shop around at renewal time Insurance loyalty rarely pays. Insurers regularly offer better rates to new customers than they extend to existing ones. Even if your current premium feels reasonable, comparing quotes annually — particularly through a platform like CoverClub — ensures you're not quietly drifting above market rate.

---

Compare Your Own Quote

Whether you're renewing an existing policy or insuring a property for the first time, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home insurance quotes across multiple insurers in minutes — so you can see exactly what's available for your property in South Nanango and beyond. Don't just accept the first number you're given.