If you own a free standing home in Southside, QLD 4570, you've probably wondered whether you're paying a fair price for home and contents insurance — or leaving money on the table. In this article, we break down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in the suburb, comparing it against local, state, and national benchmarks to give you a clear picture of where things stand.

---

Is This Quote Fair?

The quote in question comes in at $2,713 per year (or $269/month) for combined home and contents cover, with a building sum insured of $681,000 and contents valued at $100,000. Both the building and contents excess are set at $1,000.

Our independent price rating for this quote is FAIR — Around Average.

That rating holds up well under scrutiny. The annual premium sits just below the national median of $2,716/yr and is meaningfully lower than both the Queensland state average of $4,547/yr and the Fraser Coast LGA average of $4,810/yr. For a property of this size and specification, paying close to the national median while being well under regional norms is a solid result.

That said, "fair" doesn't mean you can't do better. There's still a reasonable spread of pricing in the Southside market, and a targeted comparison could reveal more competitive options.

---

How Southside Compares

The Southside (4570) suburb insurance data tells an interesting story. Based on 57 quotes collected in the area:

| Benchmark | Premium |

|---|---|

| Southside 25th percentile | $2,532/yr |

| This quote | $2,713/yr |

| Southside median | $3,152/yr |

| Southside average | $5,426/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| Fraser Coast LGA average | $4,810/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

A few things stand out here. First, the Southside suburb average ($5,426/yr) is dramatically higher than the median ($3,152/yr), which suggests a skewed distribution — likely driven by a handful of high-value or high-risk properties pushing the average upward. The median is a more reliable indicator of what most homeowners in the area are actually paying.

At $2,713/yr, this quote sits comfortably between the suburb's 25th percentile ($2,532/yr) and its median ($3,152/yr). That means it's cheaper than at least half of all quotes collected in Southside, and only modestly above the cheapest quarter of the market. Compared to the national picture, it's virtually on the median — a strong result given Queensland's generally elevated insurance costs.

The 75th percentile for Southside sits at $5,946/yr, so there are homeowners in this suburb paying more than double this quote for similar cover. That's a significant gap and a reminder of how much variation exists in the market.

---

Property Features That Affect Your Premium

Several characteristics of this property influence where its premium lands — both positively and negatively.

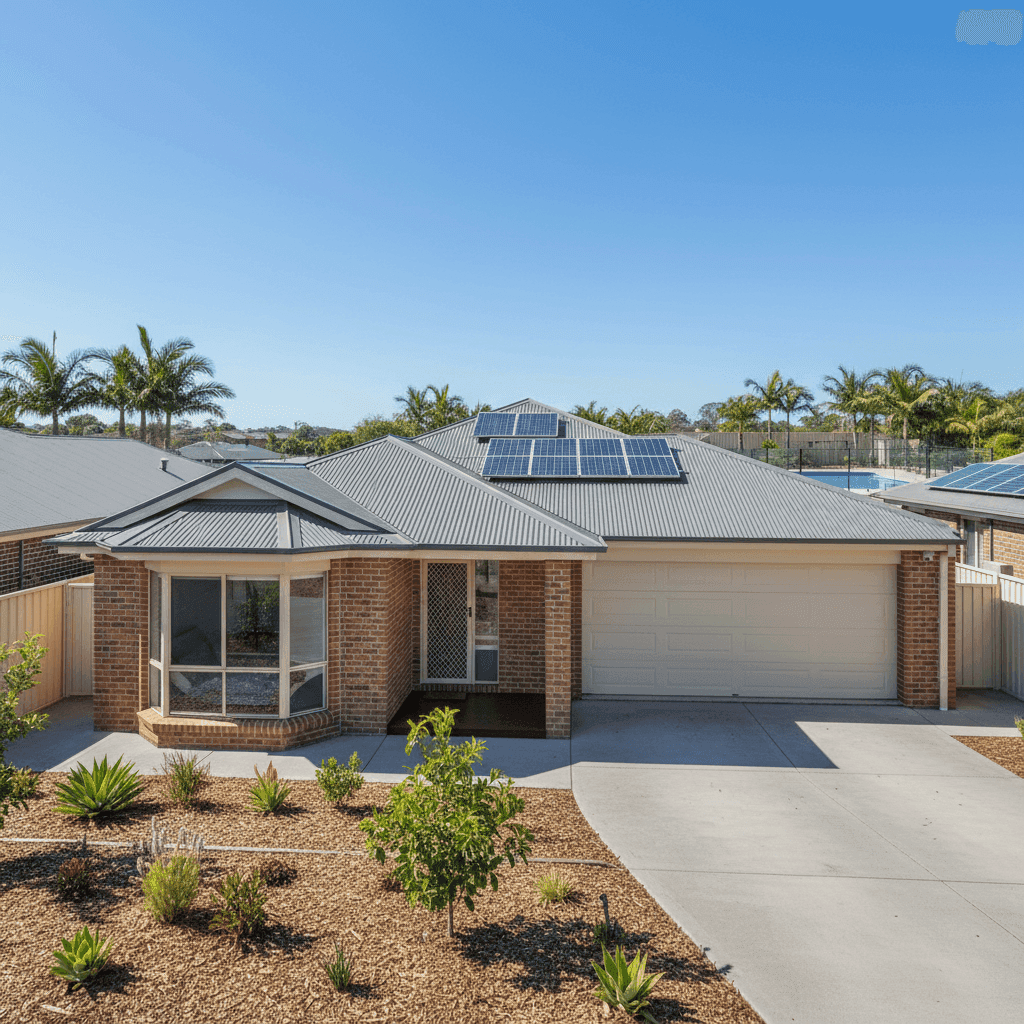

Brick Veneer Walls & Colorbond Roof

Brick veneer is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms. Combined with a steel Colorbond roof — which is lightweight, corrosion-resistant, and performs well in high-wind conditions — this construction profile typically attracts more competitive premiums than, say, weatherboard or fibrous cement cladding.

Concrete Slab Foundation

A slab foundation is the standard in Queensland and is considered low-risk by most insurers. It reduces the likelihood of subsidence-related claims and provides a stable base in the region's subtropical climate.

Swimming Pool

A pool is a feature that can nudge premiums upward. Insurers factor in the liability risk associated with pools, as well as the cost of repairing or replacing pool infrastructure in the event of damage. Homeowners with pools should ensure their policy explicitly covers pool-related structures and check whether public liability cover is adequate.

Solar Panels

Solar panels are increasingly common on Queensland rooftops, but they do add complexity to insurance. Panels represent a meaningful replacement cost (often $10,000–$20,000 or more), and not all policies cover them as standard. It's worth confirming that your building sum insured accounts for the full replacement value of your system, including inverters and mounting hardware.

214 sqm Building Size

At 214 square metres, this is a comfortably sized family home. The building sum insured of $681,000 translates to roughly $3,182 per square metre — broadly in line with current construction cost estimates for Queensland, though it's always worth reviewing this figure annually as building costs continue to rise.

No Cyclone Risk

Southside falls outside designated cyclone risk zones, which is a meaningful factor in Queensland where cyclone-affected areas can face significantly higher premiums. This property benefits from that lower-risk classification.

---

Tips for Homeowners in Southside

1. Review your building sum insured annually Construction costs in Queensland have risen sharply in recent years. If your building sum insured hasn't kept pace, you could be underinsured — meaning you'd fall short in a total loss scenario. Use a building cost calculator or speak to a quantity surveyor to validate your figure.

2. Confirm solar panels are covered Ask your insurer directly whether solar panels are included under your building cover, and whether there are any sub-limits. Some policies treat panels as a separate item or exclude them from storm damage claims. Given Queensland's severe weather, this is a critical detail to clarify.

3. Check your pool liability cover Ensure your policy includes adequate public liability protection — ideally $20 million or more. Pool-related accidents are a real risk, and standard liability limits may not be sufficient if a serious incident occurs on your property.

4. Shop the market at renewal time The wide spread between the 25th percentile ($2,532/yr) and 75th percentile ($5,946/yr) in Southside shows that insurers price this suburb very differently. Loyalty rarely pays in home insurance — comparing quotes at renewal could save hundreds of dollars without reducing your cover.

---

Compare Your Home Insurance at CoverClub

Whether you're renewing soon or just curious about what the market looks like, CoverClub makes it easy to see how your current premium stacks up. We analyse real quotes across Australia so you can make an informed decision — not just accept whatever your insurer sends at renewal. Get a home insurance quote today and find out if you're getting a fair deal.