Spreyton is a quiet residential suburb nestled in Tasmania's Latrobe municipality, sitting just minutes from Devonport along the lush Mersey River corridor. It's the kind of place where established family homes on generous blocks are the norm — and protecting one of those homes with the right insurance cover is a decision worth getting right. This article takes a close look at a real home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Spreyton, unpacking what's driving the price and how it stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $4,312 per year (or $421 per month), covering both building and contents. Our price rating for this quote is Expensive — Above Average.

To put that in perspective: the suburb average for Spreyton sits at $2,982 per year, and the median is even lower at $2,765 per year. This quote is roughly 45% above the suburb average and sits well above the 75th percentile of $3,806 — meaning it's pricier than at least three-quarters of comparable quotes collected in the area.

That said, "expensive" doesn't automatically mean "wrong." A number of property-specific factors — which we'll explore below — can legitimately push a premium higher than the neighbourhood norm. The key question is whether the cover on offer justifies the cost, and whether there's room to shop around for a better deal.

---

How Spreyton Compares

Understanding where Spreyton sits in the broader insurance landscape helps put this quote in context. Here's a snapshot:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Spreyton (7310) | $2,982/yr | $2,765/yr |

| Latrobe LGA (TAS) | $2,263/yr | — |

| Tasmania | $2,814/yr | $2,326/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out. First, Spreyton's average is actually above the broader Latrobe LGA average of $2,263, suggesting that homes within the suburb itself may carry slightly higher risk profiles or higher insured values than the wider council area. Second, Tasmania as a whole is a relatively affordable state for home insurance — the state average of $2,814 is well below the national average of $5,347, which is heavily influenced by high-risk regions in Queensland and Western Australia.

The national median of $2,764 is almost identical to Spreyton's median, suggesting that when it comes to typical properties, Spreyton is broadly in line with the rest of the country. You can explore more local data on the Spreyton suburb stats page, compare it against the full Tasmanian picture, or see where it sits on the national insurance landscape.

---

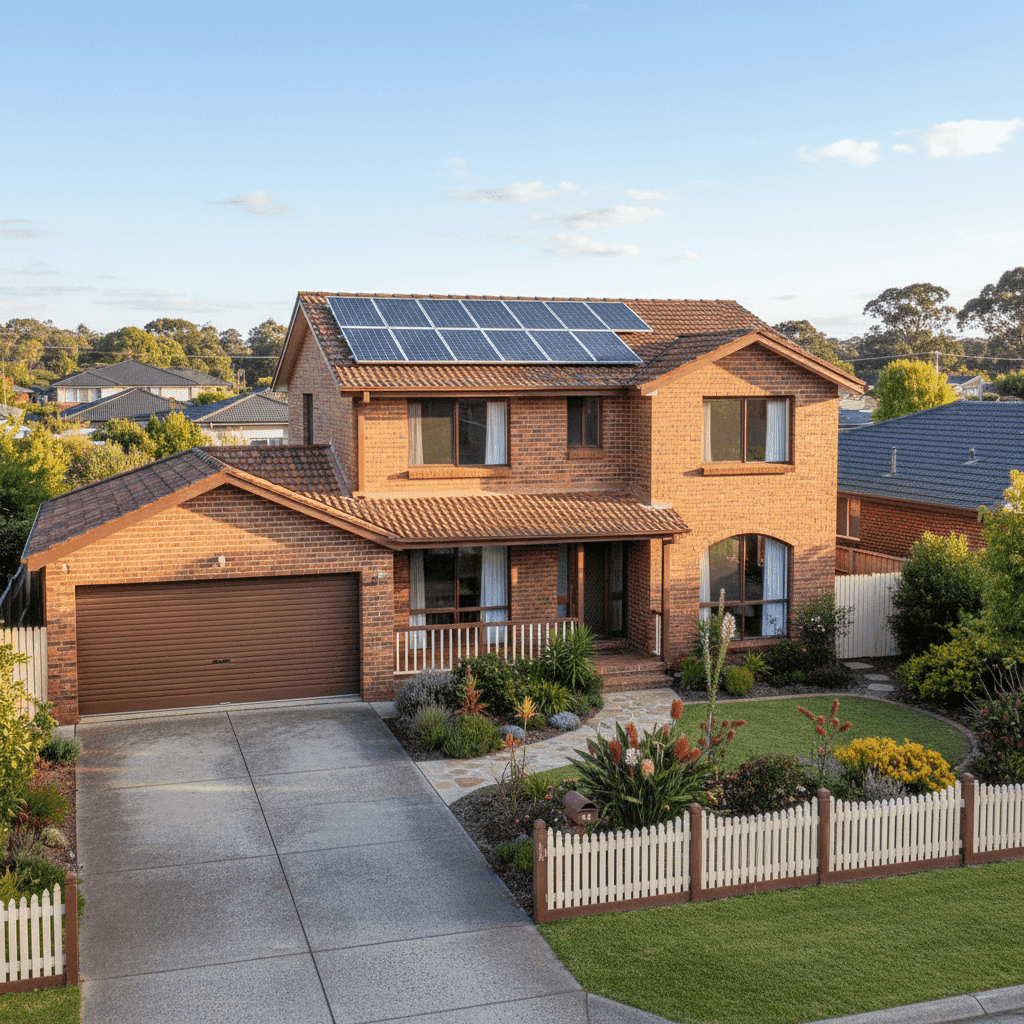

Property Features That Affect Your Premium

Several characteristics of this particular property help explain why the quote lands above the suburb average.

High Sum Insured

The building is insured for $1,630,000 — a substantial figure that reflects the cost of rebuilding a large, well-appointed home. At 244 square metres with top-of-the-range fittings, this isn't a standard cookie-cutter build. Premium quality fixtures, finishes, and fittings cost significantly more to replace, and insurers price accordingly.

Construction Era and Materials

Built in 1985, this home falls into a bracket that insurers pay close attention to. Homes from this era can have ageing plumbing, wiring, and roofing systems that increase the likelihood of claims. The brick veneer external walls are generally viewed favourably — they offer solid fire resistance and structural durability — but the tiled roof, while durable, can be costly to repair or replace if damaged by storm or hail.

Slab Foundation and Timber/Laminate Flooring

A concrete slab foundation is generally considered lower risk than older stumped or pier-and-beam foundations, as it reduces the likelihood of subsidence-related claims. However, the timber and laminate flooring throughout the home adds to the contents replacement value and can be susceptible to water damage — something insurers factor into their pricing.

Solar Panels

This property has solar panels installed, which adds a layer of complexity to both building and contents cover. Solar systems can be damaged by hail, storms, or fire, and their replacement cost is non-trivial. It's worth confirming with your insurer exactly how your solar system is covered — whether it falls under building, contents, or requires a separate endorsement.

Ducted Climate Control

Ducted heating and cooling systems are expensive to install and repair, and their inclusion in a home of this size adds to the overall replacement cost. This is another feature that can nudge premiums upward, particularly when the system spans a large floor area.

Contents Value

With $181,000 in contents insured, this is a well-furnished home. Top-of-the-range fittings typically go hand-in-hand with high-value furniture, appliances, and personal belongings — all of which contribute to the contents premium component.

---

Tips for Homeowners in Spreyton

If you're a homeowner in Spreyton looking to get the best value from your insurance, here are four practical steps worth taking:

- Review your sum insured regularly. Building costs have risen sharply in recent years, and being underinsured can be just as costly as overpaying. Use a professional quantity surveyor or an online rebuild cost calculator to make sure your $1,630,000 building cover reflects current construction costs — not what it would have cost five years ago.

- Ask about solar panel coverage specifically. Not all policies treat solar panels the same way. Some include them as part of the building, others require them to be listed separately, and a few exclude them altogether unless specified. Get clarity in writing before you sign.

- Compare quotes annually. The insurance market shifts, and loyalty doesn't always pay. With a premium at the expensive end of the local range, it's worth getting at least two or three competing quotes each renewal cycle. Even a 15–20% saving would put hundreds of dollars back in your pocket each year.

- Consider your excess strategically. Both the building and contents excess on this policy sit at $2,000. Opting for a higher voluntary excess can reduce your annual premium — but make sure you could comfortably cover that amount out of pocket if you needed to make a claim.

---

Ready to Compare?

Whether this quote is the right fit or not, the smartest move any homeowner can make is to compare. At CoverClub, we make it easy to see how your current premium stacks up and to explore alternatives — all in one place. Get a home insurance quote today and find out if you could be paying less for the same level of protection.