Springbrook is a picturesque hinterland community nestled in the Gold Coast's lush ranges, and like many semi-rural Queensland locations, it comes with its own unique set of insurance considerations. This article takes a close look at a recent building insurance quote for a three-bedroom, free-standing home in Springbrook (QLD 4213) — breaking down whether the price stacks up, how local costs compare to the broader market, and what homeowners in the area can do to keep their premiums in check.

---

Is This Quote Fair?

The quoted annual premium for this property is $2,252 per year (or approximately $216 per month), covering building only with a $1,000 excess. CoverClub's pricing analysis rates this quote as FAIR — around average for the area.

To put that in context: the suburb average premium in Springbrook sits at $3,378 per year, with a median of $3,078. That means this quote is comfortably below both the average and the median, coming in closer to the 25th percentile of $1,976 — the lower end of what people in the suburb are paying. In practical terms, this homeowner is paying less than most of their neighbours for comparable cover, which is a positive outcome.

That said, "fair" doesn't necessarily mean "the best available." There's still a meaningful gap between this quote and the 25th percentile benchmark, suggesting there may be room to shop around further. The 75th percentile for Springbrook reaches $4,163 per year, so the spread across the suburb is quite wide — a reflection of how much individual property characteristics and insurer pricing models can vary.

---

How Springbrook Compares

One of the more striking findings in this data is just how differently Springbrook fares compared to the rest of Queensland and the country at large.

| Benchmark | Premium |

|---|---|

| This quote | $2,252/yr |

| Springbrook suburb average | $3,378/yr |

| Springbrook suburb median | $3,078/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| Gold Coast LGA average | $8,161/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

The Queensland state average of $9,129 per year is eye-watering by comparison — more than four times this particular quote. Much of that is driven by high-risk coastal and cyclone-prone areas in Far North Queensland, which dramatically skew the state average upward. The Gold Coast LGA average of $8,161 tells a similar story, with beachside and flood-prone suburbs pulling figures well above what hinterland properties typically attract.

At the national level, the average sits at $5,347 per year, though the median of $2,764 is a more representative figure for typical Australian homeowners. This quote of $2,252 sits just below that national median — a solid result.

Springbrook's relatively moderate premiums (compared to coastal Gold Coast) reflect its inland elevation, lower flood exposure, and the fact that it falls outside designated cyclone risk zones. You can explore more localised pricing data on the Springbrook suburb stats page.

> Note: The suburb sample size for this analysis is 20 quotes, which is a reasonable but modest dataset. As more data is collected, these benchmarks will become increasingly precise.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth understanding in the context of insurance pricing:

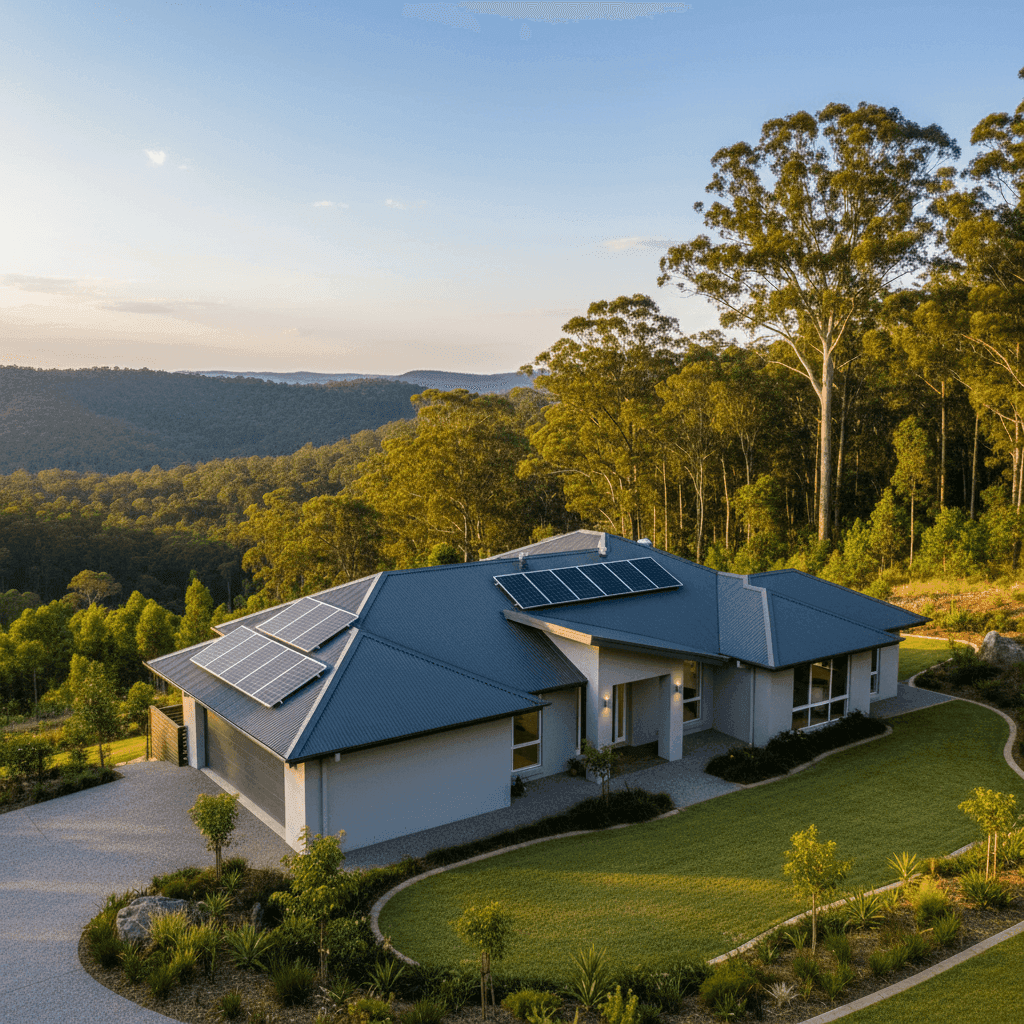

Hebel (AAC) External Walls Autoclaved Aerated Concrete (Hebel) is generally viewed favourably by insurers. It's non-combustible, resistant to termites, and holds up well in severe weather. This can contribute to more competitive premiums compared to timber-framed homes in bushfire-adjacent areas like Springbrook.

Steel / Colorbond Roof A steel Colorbond roof is another tick in the right column. It's durable, fire-resistant, and low-maintenance — all qualities that reduce the likelihood of weather-related claims. Insurers tend to price steel roofs more favourably than older tile or corrugated iron alternatives.

Slab Foundation Concrete slab foundations are straightforward to insure and don't carry the same risks as elevated or timber subfloor constructions, which can be more vulnerable to moisture, termites, and storm damage.

Solar Panels This property includes solar panels, which are typically covered under building insurance as a fixed structure. It's worth confirming with your insurer that the panels and associated inverter are explicitly included in your sum insured — not all policies treat them the same way.

Ducted Climate Control Ducted air conditioning systems are a fixed building feature and should be accounted for in the sum insured. At $594,000, the building cover here appears to reflect the inclusion of these higher-value fittings.

Building Size & Sum Insured At 169 sqm with a sum insured of $594,000, the implied rebuild cost rate is approximately $3,515 per sqm. For a Hebel-constructed home with ducted climate control and three bathrooms, this is within a plausible range for Queensland, though homeowners should periodically review their sum insured against current construction costs, which have risen significantly in recent years.

---

Tips for Homeowners in Springbrook

1. Review your sum insured annually Construction costs across Queensland have increased substantially since 2020. A sum insured set a few years ago may no longer reflect what it would actually cost to rebuild your home today. Consider getting an independent building valuation or using an online rebuild cost calculator to make sure you're not underinsured.

2. Confirm solar panels are explicitly covered Ask your insurer directly whether your solar panel system — including the inverter and any battery storage — is included in your building policy. Some policies require you to list them separately or increase your sum insured to account for them.

3. Compare quotes at renewal time Even if your current premium feels reasonable, insurers frequently adjust their pricing models. Shopping around at renewal — rather than simply auto-renewing — can uncover meaningfully better deals. Use a comparison tool like CoverClub to benchmark your quote against the market quickly.

4. Understand your bushfire and storm exposure Springbrook sits in a lush rainforest environment, but the surrounding Gold Coast hinterland does carry some bushfire risk during dry periods. Make sure your policy includes adequate cover for fire damage and check whether any exclusions apply to your specific location. Storm and water damage coverage is equally important given Queensland's summer storm season.

---

Compare Your Home Insurance Today

Whether you're a Springbrook local or considering a property in the Gold Coast hinterland, understanding what you should be paying is the first step to making sure you're not overpaying. CoverClub makes it easy to compare building and contents insurance quotes from a range of insurers — so you can see exactly where your premium sits relative to your neighbours and the broader market.