If you own a free standing home in Springfield Lakes, QLD 4300, you've probably wondered whether your home insurance premium is reasonable — or whether you're quietly overpaying. This article breaks down a real home and contents insurance quote for a four-bedroom property in the suburb, comparing it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

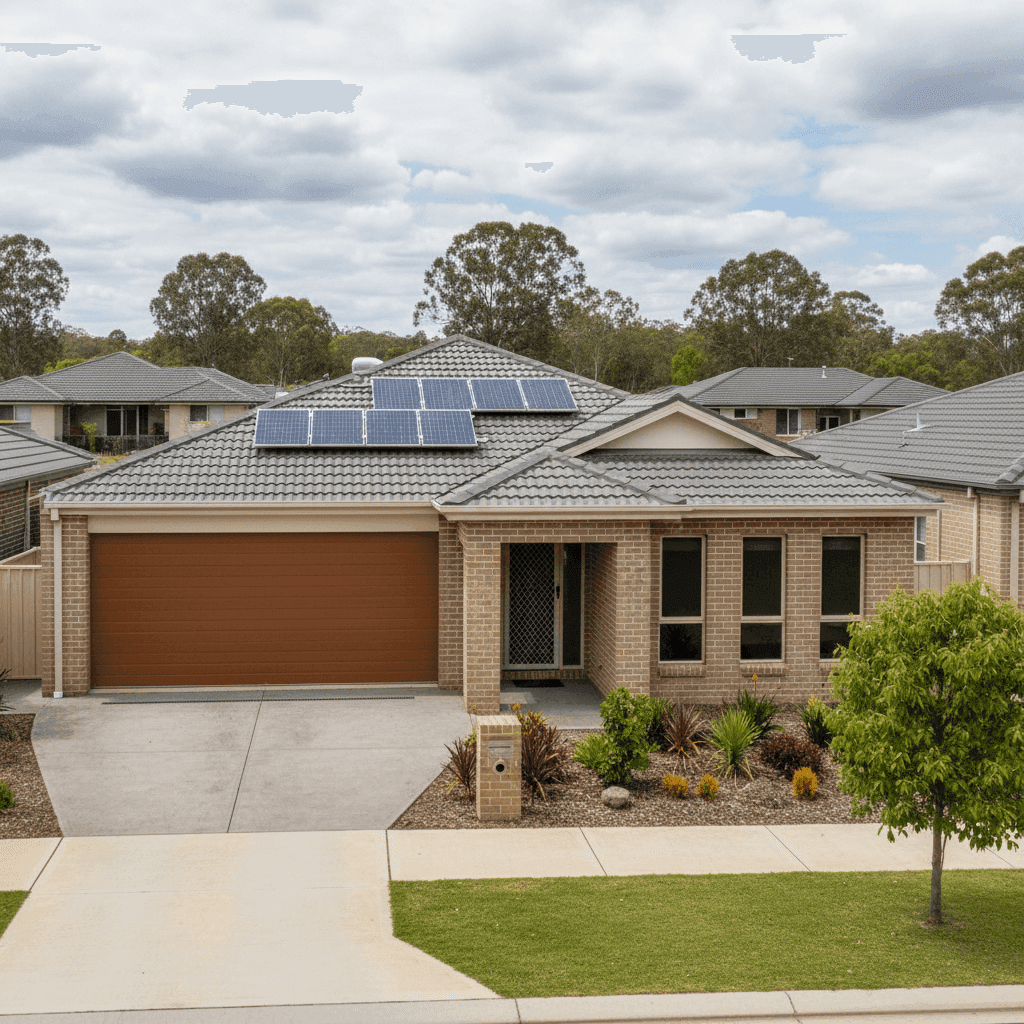

The short answer: yes — and then some. This quote came in at $1,550 per year (or around $149 per month), covering both building and contents for a 214 sqm brick veneer home with a $584,000 building sum insured and $15,000 in contents cover.

Our pricing analysis rates this quote as CHEAP — Below Average, meaning it sits well below what most Springfield Lakes homeowners are paying for comparable cover. Based on a sample of 41 quotes from the suburb, the average annual premium is $2,470, and the median sits at $2,126. Even the 25th percentile — the cheapest quarter of quotes — lands at $1,721 per year. At $1,550, this quote undercuts even that lower benchmark.

In practical terms, this homeowner is saving roughly $576 per year compared to the cheapest quarter of their neighbours, and more than $920 per year against the suburb median. That's a meaningful difference — enough to cover a family holiday or a decent home maintenance fund.

For a full breakdown of insurance pricing trends in the area, visit the Springfield Lakes suburb stats page.

---

How Springfield Lakes Compares

Springfield Lakes sits in a relatively favourable position when viewed against broader Queensland and national figures — and those contrasts are stark.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,550 |

| Suburb 25th Percentile | $1,721 |

| Suburb Median | $2,126 |

| Suburb Average | $2,470 |

| National Median | $2,764 |

| National Average | $5,347 |

| QLD State Median | $3,903 |

| QLD State Average | $9,129 |

| Ipswich LGA Average | $8,901 |

The Queensland state average of $9,129 per year might look alarming at first glance, but it's heavily skewed by high-risk coastal and cyclone-prone regions in Far North Queensland. The state median of $3,903 is a more representative figure for most south-east Queensland homeowners — and even that is more than double what this quote delivers.

The Ipswich LGA average of $8,901 per year is similarly elevated, likely pulled upward by flood-affected suburbs within the council area. Springfield Lakes, being a master-planned community built predominantly from the late 1990s onwards, tends to benefit from more modern infrastructure and better flood mitigation than older Ipswich suburbs.

Nationally, the average premium of $5,347 reflects the growing pressure of extreme weather events, rising construction costs, and reinsurance pressures across the industry. You can explore how Queensland stacks up on the QLD state stats page or view the full picture on the national stats page.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an underwriting perspective.

Brick Veneer Construction & Tiled Roof Brick veneer walls paired with a tiled roof is one of the more insurer-friendly combinations in Australia. Both materials offer solid fire resistance and durability, and they're generally cheaper to repair than timber weatherboard or metal roofing alternatives. Insurers tend to reward this with lower base premiums.

Concrete Slab Foundation A slab foundation is standard for homes of this era in south-east Queensland and is generally viewed positively by insurers. It reduces the risk of subsidence and pest-related structural damage compared to older raised foundations.

Built in 2012 The construction year matters. A home built in 2012 is relatively modern, meaning it was constructed under the updated Queensland Development Code introduced after the 2011 floods. These standards include improved stormwater management and structural requirements, which can translate to lower risk in insurers' eyes.

Solar Panels This property has solar panels installed, which adds a modest layer of complexity for insurers — panels need to be covered for damage from hail, storms, or fire. However, most standard home insurance policies include solar panels as part of the building sum insured, provided they're properly declared. It's worth confirming with your insurer that the $584,000 building sum includes replacement of the solar system.

Ducted Climate Control Ducted air conditioning systems are a fixed installation and are typically covered under the building component of a home insurance policy. Their inclusion adds to the overall replacement value of the home, so ensuring your building sum insured is adequate is important.

No Pool The absence of a swimming pool removes one source of liability and maintenance-related claims from the equation — a small but real factor in keeping premiums lean.

Tile Flooring Tiled floors throughout are durable and less susceptible to water damage than carpet or timber, which can be a minor positive from a contents and building damage perspective.

---

Tips for Homeowners in Springfield Lakes

1. Review Your Building Sum Insured Regularly Construction costs in Queensland have risen sharply over the past few years. A building sum insured of $584,000 for a 214 sqm home works out to roughly $2,730 per sqm — which is within a reasonable range for 2025/26, but worth reviewing annually. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm Solar Panels Are Covered Check your policy schedule to ensure your solar panel system is explicitly included in your building cover. Some policies require separate declaration or have sub-limits on solar equipment. Given the cost of a quality solar system, this is worth a quick call to your insurer.

3. Don't Overlook Contents Cover A contents value of $15,000 is on the lower end for a four-bedroom home. Take the time to do a proper contents inventory — furniture, appliances, clothing, electronics, and white goods add up quickly. Many homeowners discover they're significantly underinsured when they actually sit down and calculate replacement values.

4. Compare at Renewal Even with a competitive premium like this one, it pays to shop around at renewal time. Insurers regularly adjust their pricing models, and the market can shift meaningfully from year to year. A quote that was excellent last year may not be the best available this year — and vice versa.

---

Ready to Compare Home Insurance in Springfield Lakes?

Whether you're a first-time buyer or a long-term Springfield Lakes resident, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to see what other homeowners in your area are paying and find cover that suits your property and budget.

Get a home insurance quote today and see how your premium stacks up against the suburb, state, and national benchmarks.