Springfield Lakes is one of Ipswich's most popular master-planned communities, offering families a blend of modern amenities, parklands, and easy access to Brisbane. If you own a free-standing home here, you already know the suburb is a great place to live — but are you paying a fair price for your home insurance? This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom weatherboard home in Springfield Lakes (QLD 4300) and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question sits at $4,873 per year (or $467/month) for combined home and contents cover, with a building sum insured of $1,003,000 and contents valued at $103,000. Both the building and contents excess are set at $1,000.

Based on CoverClub's pricing data, this quote is rated Expensive — above average for the area. To put that into perspective:

- The suburb average for Springfield Lakes is $2,470/yr

- The suburb median is just $2,126/yr

- The 75th percentile sits at $2,712/yr — meaning this quote is well above what 75% of comparable properties in the area are paying

In short, this premium is roughly double the suburb median, which is a significant gap worth investigating. While factors like the high building sum insured ($1,003,000 for a 214 sqm home) and the presence of solar panels and ducted climate control can push premiums upward, the scale of the difference still warrants shopping around.

---

How Springfield Lakes Compares

Understanding where Springfield Lakes sits in the broader insurance landscape is useful context for any homeowner. You can explore the full data on the Springfield Lakes suburb stats page.

| Benchmark | Annual Premium |

|---|---|

| Springfield Lakes average | $2,470 |

| Springfield Lakes median | $2,126 |

| QLD average | $9,129 |

| QLD median | $3,903 |

| Ipswich LGA average | $8,901 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. Queensland as a whole carries some of the highest home insurance premiums in the country — largely driven by extreme weather risk in northern and coastal regions. The QLD state average of $9,129/yr reflects just how costly insurance can be in cyclone-prone and flood-affected areas. Springfield Lakes, sitting in the Ipswich LGA, benefits from not being in a cyclone risk zone, which keeps premiums considerably lower than the state average.

That said, the Ipswich LGA average of $8,901/yr is surprisingly high — likely skewed by flood-prone pockets within the broader LGA. Springfield Lakes itself tends to fare better due to its newer, planned infrastructure, but flood risk in neighbouring areas can still influence insurer pricing models.

Compared to the national median of $2,764/yr, the quote in this example is notably above average, reinforcing the "expensive" rating.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays a role:

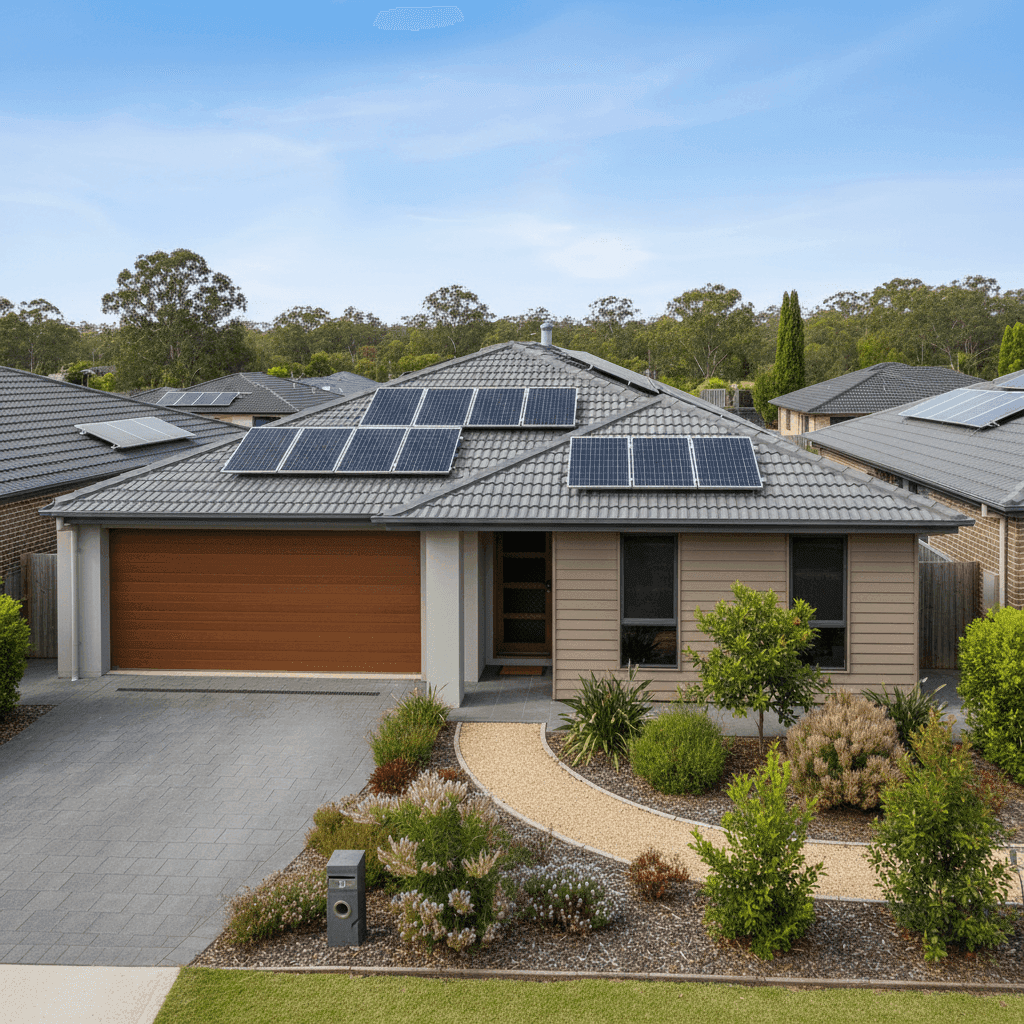

Weatherboard Timber Walls Timber-framed, weatherboard homes are generally considered higher risk by insurers than brick or rendered masonry construction. Wood is more susceptible to fire, rot, and storm damage, which typically results in a higher premium compared to brick veneer or double-brick equivalents.

Tiled Roof A tiled roof is viewed favourably by most insurers. Tiles are durable, fire-resistant, and perform well in hail events compared to corrugated iron or Colorbond. This is a neutral-to-positive factor for pricing.

Concrete Slab Foundation Slab-on-ground construction is standard for homes built in this era and region. It's generally considered lower risk than raised timber stumps, as there's no underfloor space to harbour moisture or pests.

Solar Panels Solar panels add replacement value to a property, and most insurers include them under building cover — but their presence can marginally increase the sum insured and therefore the premium. It's worth confirming with your insurer that panels are explicitly covered under your policy.

Ducted Climate Control Ducted air conditioning is a significant fixed asset. Like solar panels, it contributes to the overall replacement cost of the building and can nudge premiums upward, particularly if the system is a newer or larger capacity unit.

Construction Year: 2005 At around 20 years old, this home is relatively modern by Australian standards. Homes built post-2000 in Queensland generally comply with updated building codes, which can work in your favour with some insurers. However, components like roofing, plumbing, and electrical systems are now approaching the age where maintenance becomes increasingly important.

Building Sum Insured: $1,003,000 This is one of the most influential factors in the premium. At over $1 million for a 214 sqm home, the sum insured is on the higher end. While it's important to ensure you're not underinsured, it's equally worth double-checking that this figure accurately reflects your home's rebuild cost — not its market value. Overcalculating the sum insured is a common and costly mistake.

---

Tips for Homeowners in Springfield Lakes

1. Review your building sum insured carefully A sum insured of $1,003,000 for a 214 sqm weatherboard home may be higher than necessary. Use a reputable building cost calculator (such as the Cordell Sum Sure tool) to estimate your actual rebuild cost. Overcovering your home means you're paying a premium on cover you may never need.

2. Compare quotes from multiple insurers Given that this premium is well above the suburb median, comparing quotes is the single most effective way to reduce your costs. Head to CoverClub's quote tool to see what different insurers would charge for the same level of cover.

3. Consider your excess settings Both the building and contents excess are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have a solid emergency fund, this is often a smart trade-off.

4. Check what's covered for your solar panels and ducted AC These are significant assets. Review your policy's Product Disclosure Statement (PDS) to confirm both are explicitly listed under building cover and that the sum insured accounts for their replacement value. Some insurers treat them as optional extras or have sub-limits that may leave you exposed.

---

Ready to Find a Better Deal?

If your home insurance premium is sitting above the suburb average, it's worth taking a few minutes to compare. CoverClub makes it easy to benchmark your current quote against real data from homes in your area — and to get fresh quotes from a range of Australian insurers. Start comparing today at CoverClub and make sure you're getting the right cover at the right price.