If you own a free standing home in Springvale, NSW 2650, you've probably wondered whether you're paying a fair price for building insurance — or quietly overpaying while your insurer quietly profits. This article breaks down a real building-only insurance quote for a four-bedroom, three-bathroom home in Springvale, compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $3,294 per year (or $309/month) for building-only cover on a free standing home with a sum insured of $800,000 and a $1,000 excess. Our independent price rating for this quote is FAIR — Around Average.

That rating reflects a quote that isn't a bargain, but it's also not cause for alarm. It sits comfortably within the normal range for this suburb, meaning the homeowner isn't being stung with an unusually high premium, but there's still room to shop around and potentially do better.

To put the number in context: the suburb average premium in Springvale is $3,693/year, and the median sits at $3,602/year. This quote of $3,294 comes in below both the average and median, which is an encouraging sign. It also falls just above the 25th percentile ($3,249/year), meaning roughly three-quarters of comparable quotes in the area are more expensive. That's a reasonably competitive result.

---

How Springvale Compares

Understanding where Springvale sits in the broader insurance landscape helps put any individual quote in perspective. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Springvale (2650) | $3,693/yr | $3,602/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Narrandera LGA | $2,038/yr | — |

(Based on 29 quotes sampled in the Springvale suburb area.)

A few things stand out here. The NSW state average of $9,528/year looks eye-watering at first glance, but it's heavily skewed by high-risk and high-value properties across the state — the state median of $3,770/year is a far more representative figure, and Springvale sits just below it. This suggests that Springvale is a relatively affordable area to insure within NSW.

Nationally, the median premium of $2,764/year is actually lower than what Springvale homeowners are typically paying, which reflects the higher rebuilding costs and risk profiles in regional NSW compared to some other parts of Australia.

Perhaps most striking is the Narrandera LGA average of just $2,038/year — significantly lower than the Springvale suburb average. This could reflect differences in property values, construction types, or risk profiles across the broader LGA. It's worth keeping in mind that suburb-level data (based on 29 quotes) gives a more granular and relevant picture than LGA-wide figures.

For a deeper look at local pricing trends, visit the Springvale NSW 2650 insurance stats page, or explore NSW-wide home insurance data and national benchmarks.

---

Property Features That Affect Your Premium

Every home is different, and insurers price risk based on a detailed picture of your property. Here's how the features of this particular home likely influence the premium:

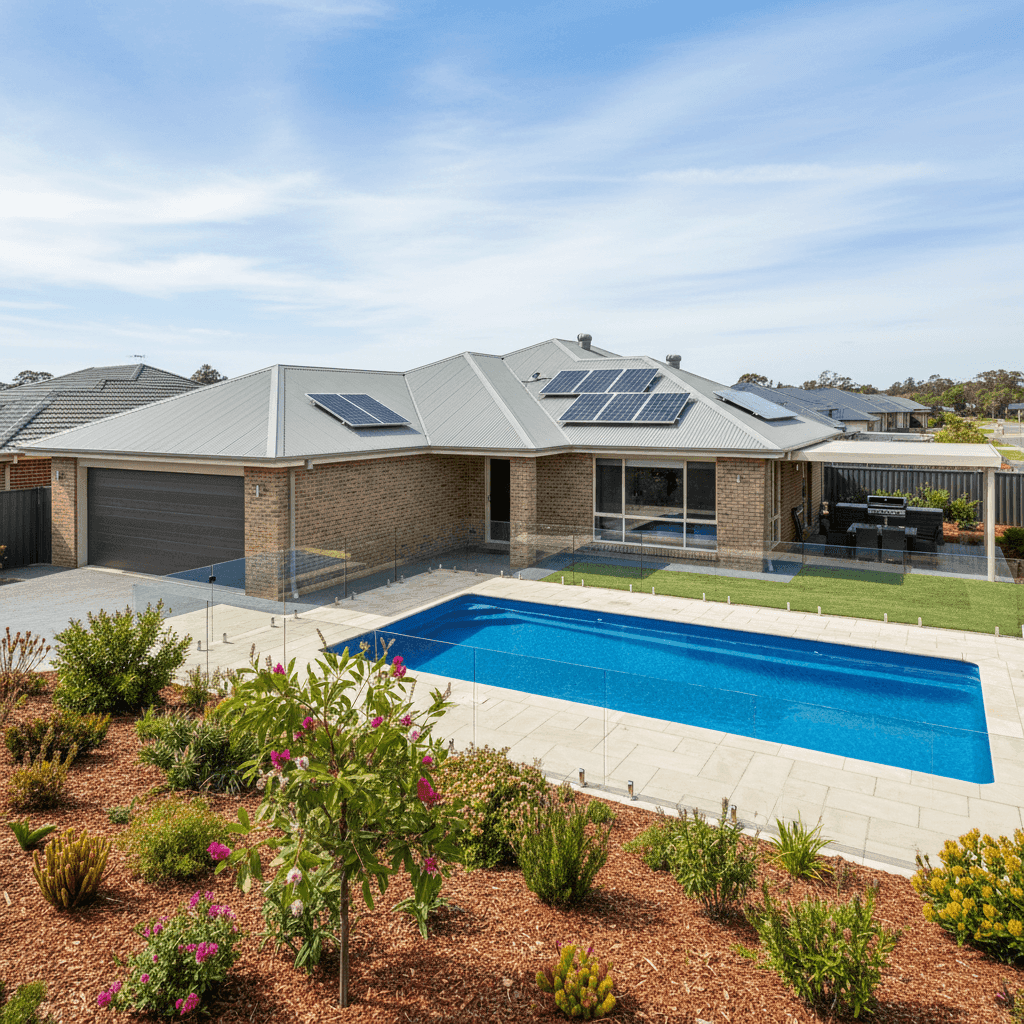

Brick Veneer Walls Brick veneer is one of the most common external wall types in Australian suburbia, and insurers generally view it favourably. It offers solid fire resistance and structural durability, which can help keep premiums moderate compared to more vulnerable materials like weatherboard or lightweight cladding.

Steel/Colorbond Roof Colorbond roofing is widely regarded as a premium roofing choice in Australia — it's durable, low-maintenance, and performs well in both heat and moderate weather events. Insurers tend to price Colorbond roofs competitively, as they're less prone to storm damage than older tile roofs.

Slab Foundation A concrete slab foundation is standard for homes built in the late 1990s and is considered a low-risk foundation type. It's not susceptible to the same subsidence or termite-related issues that can affect older pier-and-beam foundations.

Swimming Pool The presence of a pool adds a layer of liability risk and increases the overall replacement cost of the property, which can nudge premiums upward. Insurers factor in the cost of pool fencing, equipment, and potential liability associated with pool ownership.

Solar Panels Solar panels are an increasingly common feature on Australian homes, but they do add to the insured value of the property. Ensuring your sum insured accounts for the replacement cost of your solar system is important — underinsurance is a real risk if panels aren't factored in correctly.

Ducted Climate Control Ducted air conditioning systems are expensive to replace and are typically included in building cover. Their presence contributes to a higher sum insured, which is appropriate given the cost of full system replacement.

Construction Year: 1999 A home built in 1999 is relatively modern by Australian standards and would have been constructed under building codes that improved significantly through the 1990s. This generally results in a more favourable risk profile compared to pre-1970s homes.

No Cyclone Risk Springvale is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums lower than they would be for comparable homes in northern Queensland or coastal NT.

---

Tips for Homeowners in Springvale

1. Review your sum insured regularly At $800,000, this home's sum insured needs to reflect the true cost of rebuilding — not the market value of the land. Building costs have risen sharply in recent years, and many homeowners are unknowingly underinsured. Use a building cost calculator or speak to a quantity surveyor to make sure your figure is current.

2. Consider bundling contents cover This quote covers building only. If you don't have a separate contents policy, it's worth exploring whether adding contents cover to the same policy (or bundling with the same insurer) delivers savings. Many insurers offer multi-policy discounts that can make the overall package better value.

3. Shop around at renewal time Insurers often reserve their best pricing for new customers, meaning loyalty doesn't always pay. With a suburb average of $3,693/year, there's a reasonable spread of pricing in Springvale — comparing quotes at renewal could easily save you a few hundred dollars annually.

4. Check your excess settings A $1,000 excess is fairly standard, but increasing your excess (if you can comfortably self-insure smaller claims) can reduce your annual premium. Conversely, if cash flow is a concern, it's worth confirming that the excess amount is manageable in the event of a claim.

---

Compare Quotes for Your Springvale Home

Whether you're renewing an existing policy or insuring a new purchase, it pays to see what the market is offering. CoverClub makes it easy to compare building and contents insurance quotes for homes across NSW. Get a quote today and find out whether your current insurer is giving you a fair deal — or whether it's time to switch.