If you own a free standing home in Springwood, QLD 4127, you may be wondering whether your home insurance premium is competitive — or whether you're quietly overpaying year after year. This article breaks down a real home and contents insurance quote for a three-bedroom property in the suburb, benchmarking it against local, state, and national data so you can see exactly where it sits.

---

Is This Quote Fair?

The quote in question comes in at $1,019 per year (or roughly $95 per month) for combined home and contents cover, with a building sum insured of $454,000 and contents covered to $50,000. The building excess is $2,000 and the contents excess is $600.

Our pricing engine rates this quote as CHEAP — below average for the area. That's a meaningful distinction. It doesn't just mean the quote is slightly under the suburb average; it places this premium well into the lower tier of what Springwood homeowners are currently paying.

To put it plainly: this is a genuinely competitive result. For a property of this size and specification, a sub-$1,100 annual premium for both building and contents cover represents solid value — provided the policy terms and coverage limits meet the homeowner's needs.

---

How Springwood Compares

To understand just how favourable this quote is, it helps to look at the broader pricing landscape.

According to data from Springwood's suburb insurance stats, based on a sample of 26 quotes in postcode 4127:

| Benchmark | Premium |

|---|---|

| This quote | $1,019/yr |

| Suburb 25th percentile | $1,271/yr |

| Suburb average | $2,282/yr |

| Suburb median | $2,400/yr |

| Suburb 75th percentile | $3,182/yr |

This quote sits below the 25th percentile for Springwood — meaning it's cheaper than at least 75% of quotes collected in the area. That's a strong result.

Zooming out further, the picture becomes even more striking. Across Queensland as a whole, the average home insurance premium sits at $4,547 per year, with a median of $3,931. The Brisbane LGA average is similarly elevated at $4,485 per year — reflecting the wide range of risk profiles across the greater metro area, including flood-prone and cyclone-affected regions.

At the national level, Australians pay an average of $2,965 per year for home insurance, with a median of $2,716.

This quote at $1,019 is:

- 55% below the Springwood suburb average

- 78% below the Queensland state average

- 66% below the national average

These are not marginal differences. They reflect how significantly individual property characteristics — and the right insurer match — can influence what you pay.

---

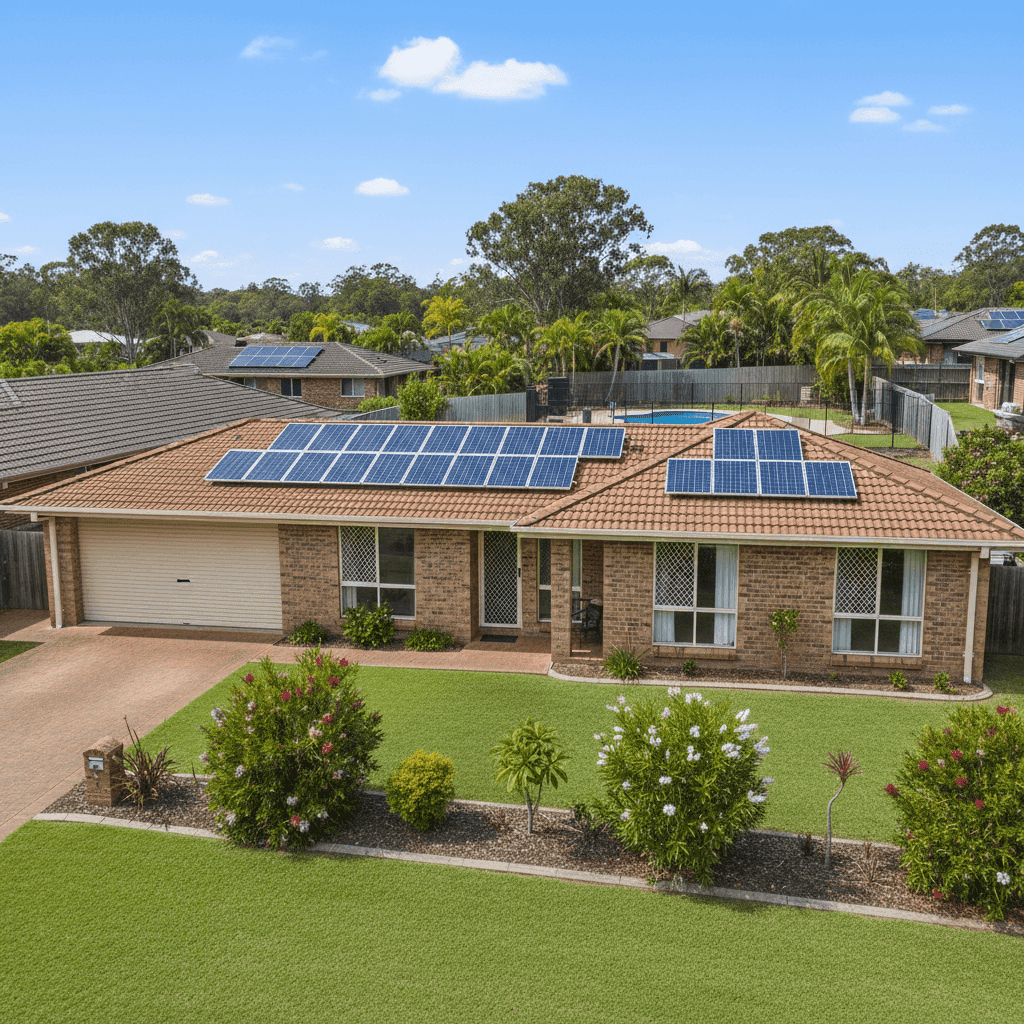

Property Features That Affect Your Premium

Several features of this particular property work in favour of a lower premium. Here's how each one plays a role:

Double Brick External Walls

Double brick construction is highly regarded by insurers. It's fire-resistant, structurally robust, and holds up well in storms. Compared to timber-framed or clad homes, double brick typically attracts lower building premiums because the risk of catastrophic structural damage is reduced.

Concrete Roof

Like double brick walls, a concrete roof (as opposed to terracotta tiles or Colorbond) is considered durable and low-maintenance by most insurers. It's resistant to hail and wind damage, which is a meaningful factor in South East Queensland where storm activity is not uncommon.

Slab Foundation

A concrete slab foundation eliminates the underfloor space that can create problems in flood-prone areas or attract pest-related claims. Insurers generally view slab homes favourably, particularly in suburban Queensland settings.

1995 Construction Year

Homes built in the mid-1990s benefit from modern building standards without the age-related risks of older properties. Wiring, plumbing, and structural elements are likely to be in reasonable condition, reducing the likelihood of claims tied to deterioration.

No Cyclone Risk Area

Springwood sits outside designated cyclone risk zones, which is a significant premium factor in Queensland. Properties in cyclone-prone areas (particularly Far North Queensland) can face dramatically higher premiums due to the elevated risk of wind and storm damage.

Pool and Solar Panels

A swimming pool adds some liability exposure and can marginally increase premiums. Solar panels, while increasingly common, can also add a small amount to the insured value of the home. In this case, both features appear to have had a limited impact on the final premium — likely because the property's other low-risk characteristics offset them.

Standard Fittings and 130 sqm Building Size

A 130 sqm home with standard fittings sits comfortably in the mid-range for rebuild cost estimation. High-end finishes and larger floor areas push rebuild costs — and therefore premiums — higher. Standard fittings keep the sum insured grounded and the premium proportionate.

---

Tips for Homeowners in Springwood

Whether you're reviewing your existing policy or shopping for new cover, here are some practical steps to ensure you're getting the best outcome:

- Review your sum insured annually. Building costs in South East Queensland have risen significantly in recent years. Make sure your $454,000 sum insured still reflects the true cost to rebuild — not just the market value of the property. Underinsurance is one of the most common and costly mistakes homeowners make.

- Don't overlook your contents value. $50,000 in contents cover may be appropriate, but it's worth doing a proper stocktake of your belongings — furniture, appliances, clothing, electronics, and jewellery — to confirm the figure is accurate. Both over- and under-insuring contents can be costly in different ways.

- Ask about discounts for your home's features. Double brick construction and a concrete roof are genuine risk-reducing features. If your insurer isn't already factoring these in, it may be worth shopping around. Some insurers reward low-risk builds more generously than others.

- Consider your excess levels carefully. This policy carries a $2,000 building excess and a $600 contents excess. A higher excess typically lowers your premium, but make sure you can comfortably cover that amount out of pocket if you need to make a claim. For most homeowners, having three to six months of living expenses in accessible savings makes a higher excess a reasonable trade-off.

---

Compare Your Own Quote at CoverClub

Insurance premiums vary enormously — even within the same suburb — depending on the insurer, the property, and the level of cover. If you're a homeowner in Springwood or anywhere across Australia, it's worth taking a few minutes to see what's available to you. Get a home insurance quote at CoverClub and find out how your current premium stacks up against the market. You might be paying more than you need to.