St Leonards is a relaxed coastal township on the Bellarine Peninsula, popular with families, retirees, and holiday homeowners drawn to its bay beaches and easy access to Geelong. If you own a free-standing home here, you've likely noticed that home insurance premiums can vary enormously — and understanding why your quote lands where it does is the first step to making sure you're not overpaying.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in St Leonards (VIC 3223), compares it against local, state, and national benchmarks, and offers practical tips to help you get better value on your cover.

---

Is This Quote Fair?

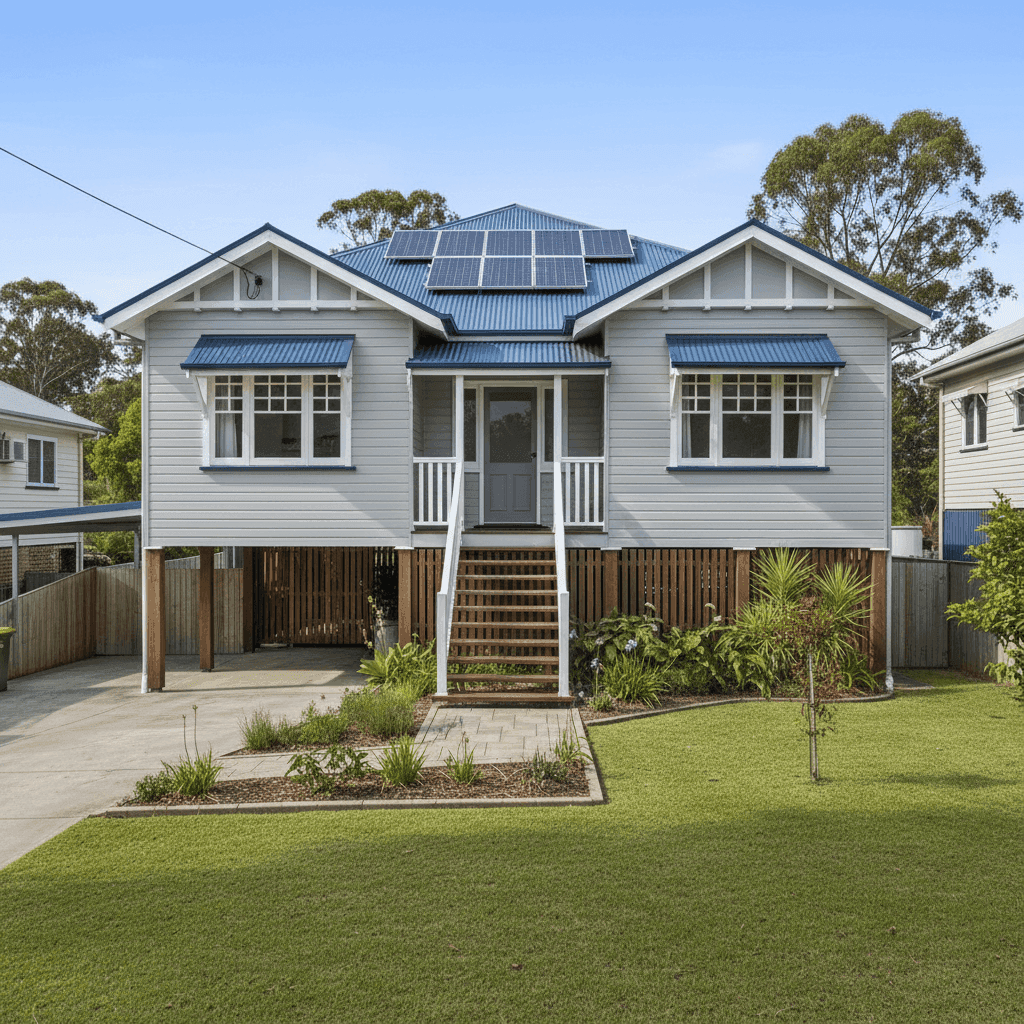

The annual premium for this property came in at $2,544 per year ($244/month), covering a building sum insured of $600,000 and contents valued at $160,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — Above Average for the St Leonards area.

To put that in context: the suburb average premium sits at $1,740 per year, and the median is even lower at $1,683. That means this quote is roughly 46% above the suburb average and about 51% above the suburb median. It does, however, fall within the suburb's 75th percentile of $2,321 — so while it's on the higher end, it's not completely out of the ordinary for properties with elevated replacement values and additional features.

It's worth noting that the $600,000 building sum insured is a significant figure. Larger sums insured directly drive premiums upward, and a 214 sqm home with quality fittings in a coastal location will naturally attract higher rebuild costs than a smaller or more basic dwelling.

---

How St Leonards Compares

Looking at the broader picture, St Leonards actually fares quite well relative to Victorian and national benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| St Leonards (3223) | $1,740/yr | $1,683/yr |

| Greater Geelong LGA | $1,754/yr | — |

| Victoria (VIC) | $3,000/yr | $2,718/yr |

| National | $5,347/yr | $2,764/yr |

The suburb average of $1,740 is significantly below the Victorian state average of $3,000 — nearly half the cost. Compared to the national average of $5,347 (which is heavily skewed by high-risk areas in Queensland and Northern Australia), St Leonards looks very affordable indeed.

This suggests that, as a suburb, St Leonards presents a relatively moderate risk profile to insurers. The absence of cyclone risk, combined with its location outside major flood and bushfire zones, helps keep the baseline cost of cover lower than many other parts of the country.

The quote in question, at $2,544, sits above the local averages but below the Victorian state average — meaning it's elevated for the suburb but not unreasonable in the broader Victorian context, particularly given the property's size and features.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how each one plays into the final premium:

Hardiplank / Hardiflex External Walls Fibre cement cladding like Hardiplank is generally viewed favourably by insurers. It's durable, fire-resistant, and less susceptible to rot and termite damage than timber weatherboards. This material choice can help moderate premiums compared to older or more vulnerable wall types.

Steel / Colorbond Roof Colorbond roofing is widely regarded as one of the most insurer-friendly roofing materials in Australia. It's long-lasting, resistant to fire and high winds, and less prone to storm damage than terracotta or concrete tiles. This is a positive factor for the premium.

Stump Foundation (Elevated by at Least 1m) Being elevated on stumps by at least one metre is a double-edged sword. On the positive side, it significantly reduces flood and inundation risk — water is less likely to enter the living areas of the home during heavy rain or storm surge events. However, elevated homes can be more vulnerable to wind uplift, and the subfloor space introduces additional complexity for insurers when calculating rebuild costs.

Construction Year: 1988 A home built in 1988 is now nearly 40 years old. Older homes may carry higher premiums due to the potential for ageing wiring, plumbing, and structural components that can increase the likelihood of certain claims. Insurers factor in the cost of bringing materials and systems up to current building codes during a rebuild.

Solar Panels The presence of solar panels adds to the insured value of the property and introduces some additional risk (e.g., storm or hail damage to panels). Make sure your policy explicitly covers solar panels — not all standard policies do, or they may apply sub-limits.

Ducted Climate Control Ducted systems are a significant fixed asset and add to the overall replacement cost of the home. This is appropriately reflected in the building sum insured.

Tile Flooring Tiled flooring is relatively low-maintenance and durable, presenting minimal additional risk to insurers compared to carpet or hardwood.

---

Tips for Homeowners in St Leonards

1. Review your building sum insured regularly Rebuild costs have risen sharply across Australia in recent years due to labour shortages and elevated material costs. A $600,000 sum insured may feel substantial, but it's worth running the numbers through a professional building cost estimator — or asking your insurer — to ensure it accurately reflects today's rebuild costs for a 214 sqm home in coastal Victoria. Being underinsured is a far costlier mistake than paying a slightly higher premium.

2. Compare quotes across multiple insurers With 31 quotes sampled in the St Leonards area, there's meaningful variation in what different insurers are willing to charge for similar properties. The gap between the 25th percentile ($1,004/yr) and the 75th percentile ($2,321/yr) is enormous — proof that shopping around can deliver real savings. Use CoverClub's free quote comparison tool to see what's available for your specific property.

3. Confirm your solar panels are covered Solar panel coverage varies widely between policies. Some insurers include panels under the building sum insured automatically; others require an endorsement or apply strict sub-limits. Given the cost of a quality solar system, it's worth a direct conversation with your insurer to confirm exactly what's covered and under what circumstances.

4. Consider a higher excess to reduce your premium Both the building and contents excesses on this quote are set at $1,000. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. This strategy works best if you have an emergency fund to cover the excess in the event of a claim, and if you're unlikely to make small or frequent claims.

---

Compare Your Home Insurance Today

Whether this quote reflects good value for your situation depends on your property's specific characteristics, your insurer's risk appetite, and how aggressively you've shopped the market. The best way to know if you're getting a fair deal is to compare.

CoverClub makes it easy to benchmark your current premium against real quotes from across the market — no jargon, no pressure, just clear data to help you make a confident decision. Enter your address today and see how your premium stacks up.