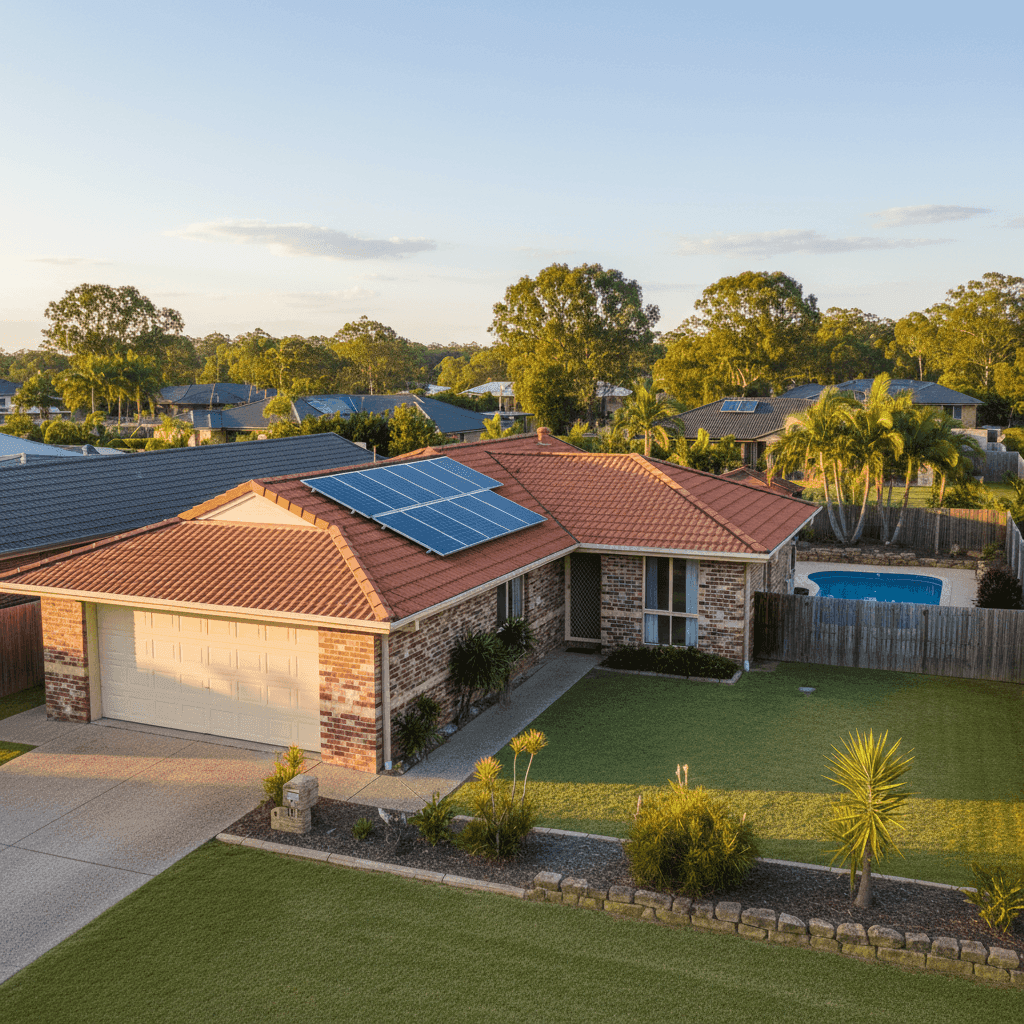

Home insurance costs can vary dramatically depending on where you live — and Steiglitz in Queensland's postcode 4207 is a great example of a suburb where getting the right quote really matters. This article breaks down a recent home and contents insurance quote for a three-bedroom, free-standing brick veneer home in Steiglitz, comparing it against local, state, and national benchmarks so you can see exactly how it stacks up.

---

Is This Quote Fair?

The short answer: yes — and then some. This particular quote came in at $2,078 per year (or around $203 per month), covering both building (insured at $399,000) and contents ($50,000), each with a $2,000 excess. Our price rating for this quote is CHEAP, meaning it sits well below average for the area.

To put that into perspective, the suburb average for Steiglitz sits at $4,585 per year, and the median is $3,034. Even the 25th percentile — meaning the cheapest quarter of quotes in the suburb — comes in at $2,575. This quote beats even that threshold, landing below the cheapest tier of local pricing. For a homeowner in this area, that's a genuinely strong result.

It's worth noting that our suburb sample size for Steiglitz QLD 4207 is currently 10 quotes, so while the data is directionally useful, a larger sample would give us even more confidence. That said, the gap between this quote and the suburb average is significant enough to be meaningful.

---

How Steiglitz Compares

To understand just how competitive this quote is, it helps to zoom out and look at the broader picture.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,078 |

| Steiglitz Suburb Average | $4,585 |

| Steiglitz Suburb Median | $3,034 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

| Gold Coast LGA Average | $8,161 |

The figures paint a striking picture. Queensland home insurance premiums are among the highest in the country, largely driven by the state's exposure to cyclones, floods, and severe storms. The QLD state average of $4,547 is well above the national average of $2,965, reflecting that elevated risk environment.

What makes this quote particularly noteworthy is that it also comes in below the national average — not just the local one. For a Queensland property, that's uncommon. The Gold Coast LGA average of $8,161 per year further illustrates how wide the spread can be even within the same region; coastal and low-lying properties in the LGA can attract significantly higher premiums due to flood and storm surge exposure.

Steiglitz itself sits in the hinterland, away from the coastline, which likely contributes to the more favourable pricing seen here.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour from an insurance pricing perspective.

Brick veneer construction is generally well-regarded by insurers. It offers solid fire resistance and structural durability compared to timber-framed or clad alternatives, which can translate to lower building premiums. Paired with a tiled roof, the property presents a fairly resilient profile — tiles are considered more fire-resistant than Colorbond or corrugated iron in some assessments, though they can be more expensive to repair after hail damage.

The slab foundation is another positive signal. Slab homes tend to be less susceptible to certain types of subsidence and pest ingress compared to raised or suspended floor systems, which insurers typically view favourably.

Tiled flooring throughout the home is also worth noting. Tiles are durable and water-resistant, reducing the likelihood of claims related to water damage or floor replacement — a factor some insurers consider when pricing contents and building cover.

On the flip side, the property does have a swimming pool, which introduces some liability considerations. Pools can add to the cost of a policy due to the potential for injury claims and the cost of pool-related repairs. Similarly, solar panels add to the replacement value of the building and may slightly influence the sum insured calculation — though at $399,000 for a 130 sqm home, the building sum insured appears reasonable for the area.

The home is not in a cyclone risk zone, which is a meaningful factor in Queensland. Properties in cyclone-prone regions of QLD can attract significant premium loadings, so being outside that zone is a genuine pricing advantage.

---

Tips for Homeowners in Steiglitz

Whether you're reviewing your existing policy or shopping for the first time, here are a few practical steps worth considering.

1. Review your sum insured regularly Building costs have risen sharply in recent years. A 130 sqm brick veneer home insured at $399,000 may be appropriate today, but construction costs shift — make sure your sum insured reflects current rebuild costs, not what you paid for the property or what it was worth a few years ago. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Consider your excess carefully This policy carries a $2,000 excess on both building and contents. A higher excess typically lowers your premium, but make sure it's an amount you could genuinely afford to pay out of pocket in the event of a claim. If cash flow is a concern, a lower excess with a slightly higher premium might offer better peace of mind.

3. Don't overlook your pool and solar panels Make sure your policy explicitly covers your pool equipment and solar panel system. Some standard policies include these as part of the building sum insured, but others treat them as optional extras or exclude certain types of damage. It's worth reading the Product Disclosure Statement (PDS) carefully or asking your insurer directly.

4. Compare quotes at renewal Even if you're happy with your current premium, the insurance market changes every year. The wide spread in Steiglitz pricing — from $2,078 to well over $4,500 — shows that different insurers assess this suburb very differently. Shopping around at renewal could save you hundreds of dollars without sacrificing cover quality.

---

Ready to Compare Home Insurance in Steiglitz?

Whether you're a first-time buyer or a long-time local, comparing quotes is the single most effective way to make sure you're not overpaying. CoverClub makes it easy to see real quotes side by side, tailored to your property. Get a home insurance quote today and find out how your current premium stacks up — you might be surprised by what's available.