If you own a free standing home in Sunnybank Hills, QLD 4109, you've probably noticed that home insurance premiums can vary wildly depending on who you ask. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom brick veneer property in the suburb — and puts it in context against local, state, and national benchmarks so you can judge whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes to $2,752 per year (or $264/month) for combined home and contents cover, with a building sum insured of $700,000 and contents valued at $100,000. The building excess sits at $5,000 and the contents excess at $2,000.

Our price rating for this quote is Expensive (Above Average).

To understand why, it helps to look at what other homeowners in Sunnybank Hills are paying. Based on 77 quotes collected for the suburb, the suburb average premium is $2,095/yr and the median is $1,954/yr. This quote lands above the 75th percentile of $2,581/yr, meaning it's pricier than roughly three-quarters of comparable quotes in the area.

That said, "expensive" is relative. The building sum insured here is $700,000 — which is on the higher end for the suburb — and the contents cover adds another $100,000 to the equation. A higher insured value naturally pushes premiums up, so the gap between this quote and the suburb median isn't necessarily a red flag on its own. However, it does suggest there's room to shop around.

---

How Sunnybank Hills Compares

One thing that immediately stands out when you zoom out is just how affordable South East Queensland suburbs like Sunnybank Hills are compared to the broader state picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Sunnybank Hills (suburb) | $2,095/yr | $1,954/yr |

| Brisbane LGA | $16,277/yr avg | — |

| Queensland (state) | $9,129/yr avg | $3,903/yr |

| National | $5,347/yr avg | $2,764/yr |

The Queensland state average of $9,129/yr is heavily skewed by high-risk coastal and cyclone-prone regions in North Queensland, where premiums can be eye-watering. Similarly, the national average of $5,347/yr is dragged upward by flood-prone areas and bushfire-risk zones across the country.

The Brisbane LGA average of $16,277/yr looks alarming at first glance, but this figure is almost certainly influenced by premium outliers in flood-affected suburbs closer to the river. Sunnybank Hills, sitting in the southern suburbs, benefits from relatively benign risk conditions by comparison.

In short: at $2,752/yr, this quote is above the local suburb norm — but it's a far cry from what homeowners in higher-risk parts of Queensland are paying.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on what insurers charge.

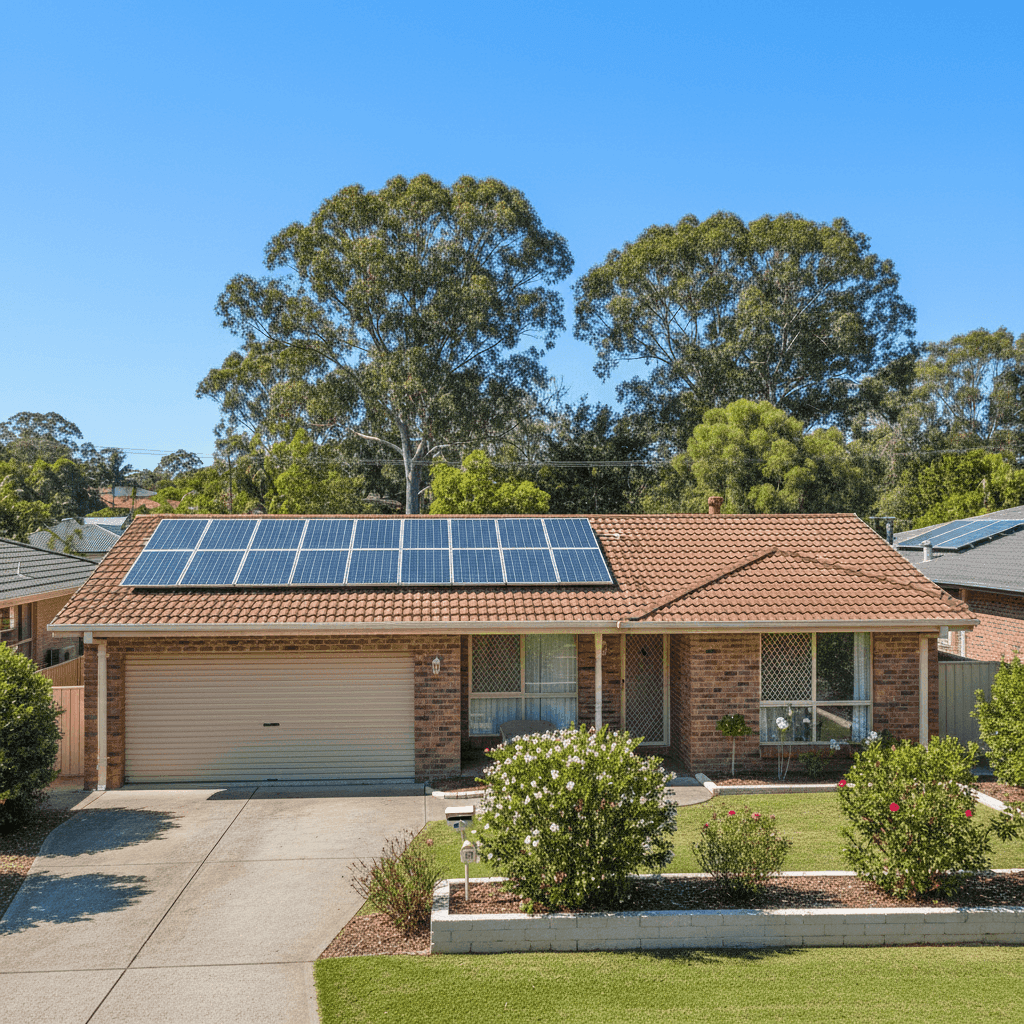

Brick Veneer Walls & Tiled Roof Brick veneer construction is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms. Combined with a tiled roof, this property sits in a construction category that typically attracts lower premiums than timber-framed or clad homes. That's a plus for the policyholder.

Slab Foundation A concrete slab foundation is standard for homes of this era in Queensland and doesn't carry the same subsidence or moisture risks associated with raised timber stumps. Insurers generally treat slab foundations as low-risk.

Construction Year: 1985 At roughly 40 years old, this home is well past its new-build phase. Older properties can attract slightly higher premiums due to the potential for ageing plumbing, wiring, or roofing materials — though a well-maintained 1985 brick home is unlikely to be penalised heavily.

Solar Panels The presence of solar panels adds a modest layer of complexity for insurers. Panels need to be covered for storm damage, hail, and electrical faults, which can nudge premiums upward slightly. It's worth confirming with your insurer exactly what solar-related events are covered under your policy.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and adds to the overall replacement cost of the home. This is factored into the building sum insured and contributes to a higher premium compared to a property without it.

No Pool, No Cyclone Risk Zone The absence of a pool removes a liability and maintenance risk that some insurers price in. And being outside a designated cyclone risk area means this property avoids the significant premium loading that affects homes in North Queensland — a meaningful saving.

Building Size: 214 sqm At 214 square metres, this is a comfortably sized family home. The building sum insured of $700,000 works out to roughly $3,270/sqm, which is broadly in line with current construction costs in South East Queensland when you factor in ducted systems, tiled flooring, and standard-quality fittings.

---

Tips for Homeowners in Sunnybank Hills

1. Compare quotes before renewing Insurers often apply "loyalty tax" — quietly increasing premiums at renewal without a corresponding change in your risk profile. With 77 quotes on record for Sunnybank Hills, there's enough market data to benchmark your renewal price. If your premium is above $2,581/yr (the 75th percentile), it's worth getting at least two or three competing quotes.

2. Review your sum insured regularly Construction costs have risen sharply in recent years. If your building sum insured is based on an older valuation, you may be underinsured — meaning a total loss payout might not cover a full rebuild. Conversely, if your sum insured is too high, you're paying more premium than necessary. Consider a professional building replacement cost assessment every few years.

3. Ask about your excess options This policy carries a $5,000 building excess and a $2,000 contents excess — both on the higher side. While a higher excess reduces your annual premium, it also means a larger out-of-pocket cost when you do make a claim. Make sure the excess level genuinely reflects what you could comfortably afford to pay in an emergency.

4. Check your solar panel coverage If you have solar panels (as this property does), read the fine print carefully. Some policies cover panels as part of the building, others treat them separately, and some exclude certain types of damage altogether. Confirm whether your policy covers panel replacement after hail, storm, or electrical surge.

---

Ready to Find a Better Deal?

Whether this quote is the right fit depends on your circumstances — but you shouldn't accept it without checking what else is available. At CoverClub, we make it easy to compare home and contents insurance quotes for properties across Australia, including right here in Sunnybank Hills.

Get a free quote comparison at CoverClub →

You can also explore detailed premium data for Sunnybank Hills, Queensland, and nationally to see exactly where your premium sits in the market.