If you own a free standing home in Sunset, QLD 4825, you're likely curious about what a fair home insurance premium looks like — and whether the quote sitting in your inbox is competitive. In this article, we break down a real building insurance quote for a five-bedroom, three-bathroom home in Sunset, compare it against local, state, and national benchmarks, and share some practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,075 per year (or $199 per month) for building-only cover on a free standing home with a sum insured of $1,004,000 and a $1,000 building excess. Our rating? Cheap — below average. That's a strong result for the homeowner.

To put it in perspective, the Queensland state average premium sits at $9,129 per year, with a median of $3,903/yr. This quote comes in at roughly 77% below the state average and nearly 47% below the state median — a significant saving by any measure.

Compared to national figures, where the average annual premium is $5,347 and the median is $2,764, this quote still holds up well, sitting below both benchmarks. For a home of this size and value, a sub-$2,100 annual premium represents genuinely competitive pricing.

It's worth noting that Queensland as a whole tends to carry elevated insurance premiums due to the state's exposure to severe weather events — cyclones, flooding, and storms. The fact that this property falls below even the national median is a notable outcome.

---

How Sunset Compares

While suburb-level data isn't available for Sunset (4825) at this time, we can still draw meaningful comparisons using broader datasets. You can explore available Sunset suburb insurance statistics here as data becomes available.

Here's how this quote stacks up across the key benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,075 |

| LGA (Carpentaria) Average | $5,066 |

| QLD State Median | $3,903 |

| National Median | $2,764 |

| QLD State Average | $9,129 |

| National Average | $5,347 |

The Carpentaria LGA average of $5,066 per year is a particularly useful local reference point. This quote comes in at 59% below the LGA average — a remarkable gap that suggests the property's specific characteristics are working strongly in the homeowner's favour.

Queensland's elevated state average is largely driven by high-risk postcodes in cyclone-prone coastal and far-north regions. Properties in areas with lower natural hazard exposure, like those not classified as cyclone risk zones, can attract meaningfully lower premiums even within the same state.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its favourable premium. Let's unpack the key ones:

Construction Materials

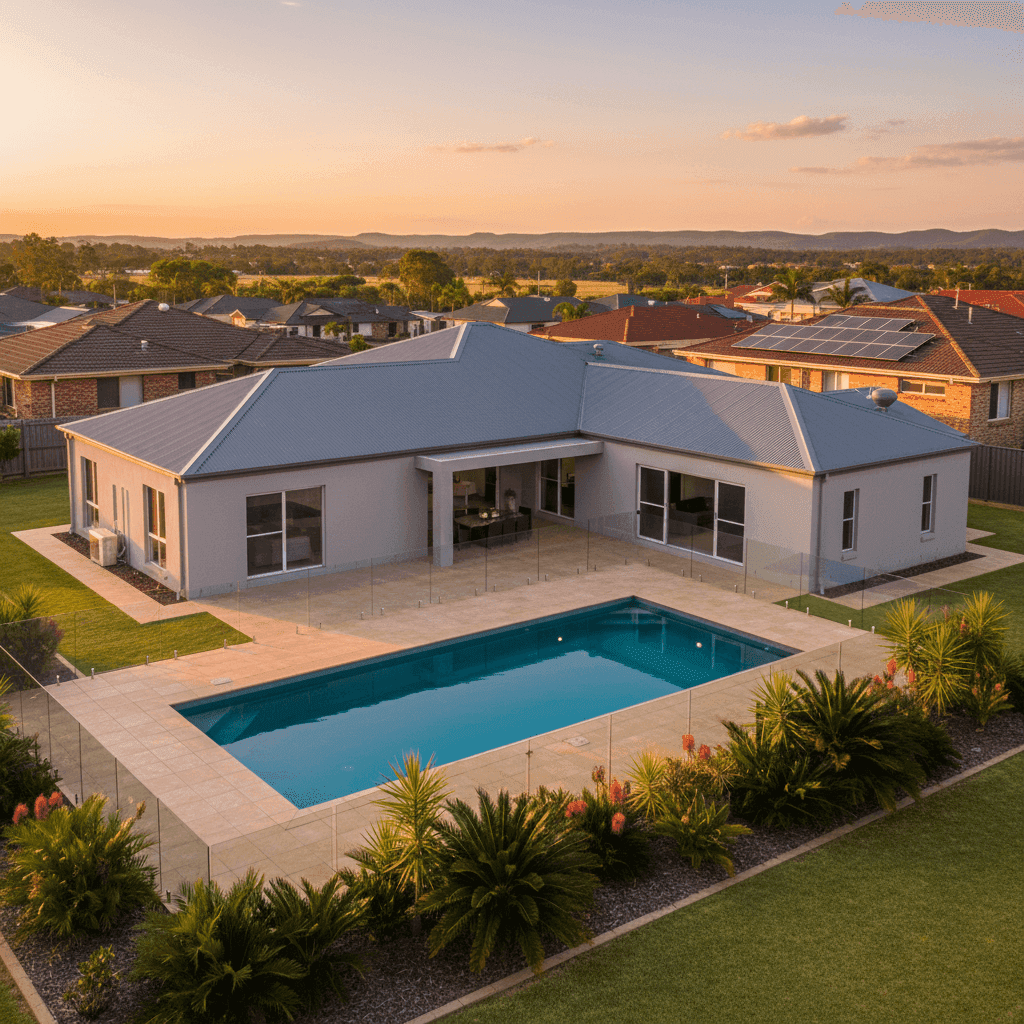

The home features concrete external walls and a steel/Colorbond roof — both considered highly durable and resilient materials by insurers. Concrete construction resists fire, termites, and impact damage, while Colorbond steel roofing is known for its longevity and resistance to corrosion and extreme weather. These materials typically attract lower premiums compared to timber-framed or fibro homes.

Foundation and Flooring

Built on a slab foundation with tile flooring, this home has a solid structural base. Slab foundations are generally viewed favourably by insurers as they reduce the risk of subfloor damage and moisture-related issues. Tiled floors are also more resilient to water damage than carpet or timber, which can help moderate claims risk.

Age of Construction

The home was built in 1976, making it approximately 50 years old. Older homes can sometimes attract higher premiums due to ageing infrastructure, but with durable construction materials and a solid slab foundation, this property appears to have aged well in the eyes of the insurer.

Swimming Pool

The presence of a swimming pool adds to the replacement cost of the property and can slightly increase premiums, as pools represent an additional liability and rebuilding cost. At 139 sqm of building area, the $1,004,000 sum insured accounts for the full scope of the property — pool infrastructure included.

No Cyclone Risk Classification

This is a significant premium driver — or rather, the absence of one. Properties not classified as cyclone risk areas benefit from considerably lower base premiums in Queensland, where cyclone loading can add thousands of dollars annually to a policy. This alone may explain much of the gap between this quote and the broader QLD state average.

Ducted Climate Control

The home includes ducted climate control, which is reflected in the sum insured. While this adds value to the building, it's a relatively standard inclusion in Queensland homes and unlikely to substantially move the needle on premium.

---

Tips for Homeowners in Sunset

Whether you're renewing your policy or shopping around for the first time, here are four practical steps to make sure you're getting the right cover at the right price.

1. Don't underinsure your home. A sum insured of $1,004,000 for a 139 sqm concrete home with a pool and ducted air conditioning seems reasonable, but rebuilding costs can escalate quickly — especially in regional Queensland where trades and materials may cost more. Review your sum insured annually and use a building cost calculator to check your figure is keeping pace with construction cost inflation.

2. Compare quotes regularly. Even if your current premium is competitive, it pays to compare home insurance quotes at renewal time. Insurers adjust their pricing models frequently, and the market can shift significantly from year to year. A quote that was cheap last year may not be the best option today.

3. Ask about discounts for home security. Installing monitored alarms, deadbolts, and security cameras can reduce your premium with many insurers. Given the size of this property, investing in a quality security system may deliver both peace of mind and a tangible reduction in your annual cost.

4. Review your excess settings. This policy carries a $1,000 building excess. Opting for a higher voluntary excess can reduce your annual premium — a useful lever if you're looking to lower your outgoings and are comfortable covering smaller claims out of pocket.

---

Compare Your Home Insurance Today

Whether your property is similar to this one or entirely different, the best way to know if you're paying a fair price is to compare. CoverClub makes it easy to benchmark your current premium against real market data and get quotes tailored to your property. Start your comparison at CoverClub and find out where your premium really sits.