If you own a free standing home in Sunshine Acres, QLD 4655, you already know that finding the right home insurance can feel like navigating a maze. Premiums vary enormously across Queensland — and understanding what's driving your quote is the first step toward making sure you're not overpaying. This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom property in Sunshine Acres, compares it against state and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The short answer: yes, and then some. This quote — at $2,555 per year (or $239/month) — is rated CHEAP, sitting well below the average for both Queensland and the country as a whole.

For a home and contents policy covering a $750,000 building sum insured and $40,000 in contents, that's a competitive outcome. The building excess sits at $2,000 and the contents excess at $500, which are fairly standard figures for policies at this price point.

It's worth noting that a lower excess on contents ($500) means you can make smaller claims on your belongings without a hefty out-of-pocket cost — a useful feature for a household with everyday valuables. The higher building excess of $2,000 is a common trade-off insurers offer to keep annual premiums down on the structural side of your cover.

---

How Sunshine Acres Compares

To put this quote in perspective, here's how it lines up against broader market data:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,555 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

The numbers tell a clear story. Queensland is one of the most expensive states in Australia for home insurance — largely due to the prevalence of cyclone risk, flooding, and severe storm events across much of the state. The QLD state average of $9,129/yr is nearly double the national average of $5,347/yr, reflecting just how heavily weather risk weighs on premiums north of the border.

Against that backdrop, this quote at $2,555 is remarkably competitive — sitting 72% below the QLD state average and 7% below the national median. Even compared to the national median of $2,764, this policy comes in cheaper, which is a strong result for any Queensland homeowner.

Note that suburb-level comparison data for Sunshine Acres isn't currently available, but you can check the Sunshine Acres stats page as more data becomes available over time.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour — and a few add complexity that insurers factor into their pricing.

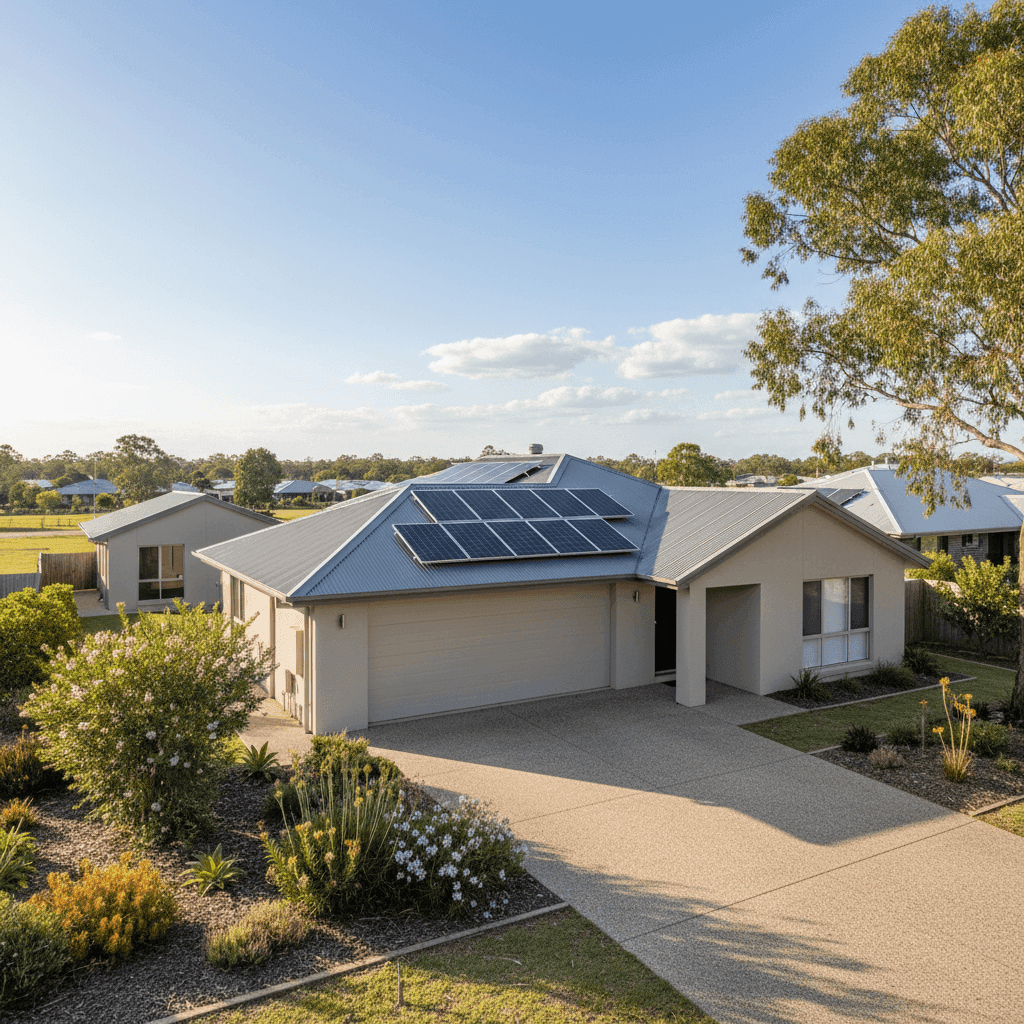

Construction materials play a significant role in how insurers assess risk. This home features concrete external walls and a steel/Colorbond roof, both of which are viewed favourably. Concrete is highly resistant to fire, termites, and impact damage, while Colorbond roofing is durable, lightweight, and well-suited to the Queensland climate. Together, these materials typically attract lower premiums compared to weatherboard or older tiled roofs.

The slab foundation and tiled flooring are similarly low-risk from an insurer's perspective. Slab construction is structurally solid and less susceptible to subsidence or pest damage, while tiles are durable and easier to replace than carpet or timber flooring in the event of water damage.

Solar panels are worth flagging — they add value to the property but also represent a potential liability. Some insurers include solar systems under the building sum insured automatically, while others treat them as an optional extra. It's worth confirming with your insurer that your solar installation is fully covered under the $750,000 building sum.

The granny flat is another feature that deserves attention. A secondary dwelling on the property increases the replacement cost of the home, and depending on how it's used (owner-occupied vs. rented out), it can affect both the building sum insured and the type of cover required. Make sure your policy explicitly covers the granny flat as part of the insured structure.

Ducted climate control is a high-value fixture that should be included in your building sum insured. These systems can cost tens of thousands of dollars to replace, and they're often overlooked when homeowners calculate their sum insured.

The property is not located in a designated cyclone risk area, which is a meaningful factor in keeping this premium competitive. Many parts of Queensland attract significant cyclone loading on premiums — avoiding that surcharge is a genuine financial advantage for Sunshine Acres homeowners.

The home was built in 1990, making it around 35 years old. Properties of this age are generally well-understood by insurers — old enough to have settled, but not so old as to raise significant concerns about building standards. Standard fittings quality aligns with this era and keeps replacement cost estimates straightforward.

---

Tips for Homeowners in Sunshine Acres

1. Double-check your building sum insured At $750,000, the building sum insured needs to reflect the full cost of rebuilding — not the market value of the property. With a granny flat, solar panels, ducted air conditioning, and 160 sqm of living space, it's important to use a building cost calculator or speak with a quantity surveyor to ensure you're not underinsured. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panel and granny flat coverage As mentioned above, don't assume these are automatically included. Ask your insurer directly: Are solar panels covered under the building policy? Is the granny flat listed as an insured structure? Get it in writing.

3. Review your contents sum insured annually $40,000 in contents cover is a starting point, but it's easy to accumulate more than you realise over time — furniture, appliances, electronics, clothing, and valuables all add up. Do a room-by-room inventory every year to make sure your contents cover keeps pace with what you actually own.

4. Consider your excess strategically The $2,000 building excess means you'd cover the first $2,000 of any building claim yourself. If you have savings set aside and want to keep premiums low, this is a sensible trade-off. However, if you'd prefer more financial protection on smaller claims, it may be worth asking your insurer what the premium difference would be at a lower excess.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, comparing quotes is the single most effective way to make sure you're getting fair value. Get a home insurance quote at CoverClub and see how your premium stacks up against the market in minutes — no jargon, no pressure, just clear data to help you decide.