Sunshine Bay is a quiet coastal suburb tucked along the South Coast of New South Wales, sitting within the Shoalhaven local government area. It's the kind of place that attracts families and sea-changers alike — and with that lifestyle comes the responsibility of protecting your home properly. This article breaks down a real building insurance quote for a four-bedroom, free-standing home in Sunshine Bay (postcode 2536), helping you understand whether the premium stacks up and what's driving the cost.

---

Is This Quote Fair?

The quote in question comes in at $4,072 per year (or $398/month) for building-only cover, with a building excess of $2,000 and a sum insured of $989,000.

Our price rating for this quote is Expensive — Above Average.

To put that in context: the average premium for comparable properties in Sunshine Bay sits at $3,425/year, with a median of $3,347. This quote lands above the suburb's 75th percentile of $3,911, meaning it's priced higher than at least three-quarters of similar quotes we've seen in the area. That's a meaningful gap — roughly $647 above the suburb average — and worth investigating before you simply accept the renewal or sign on the dotted line.

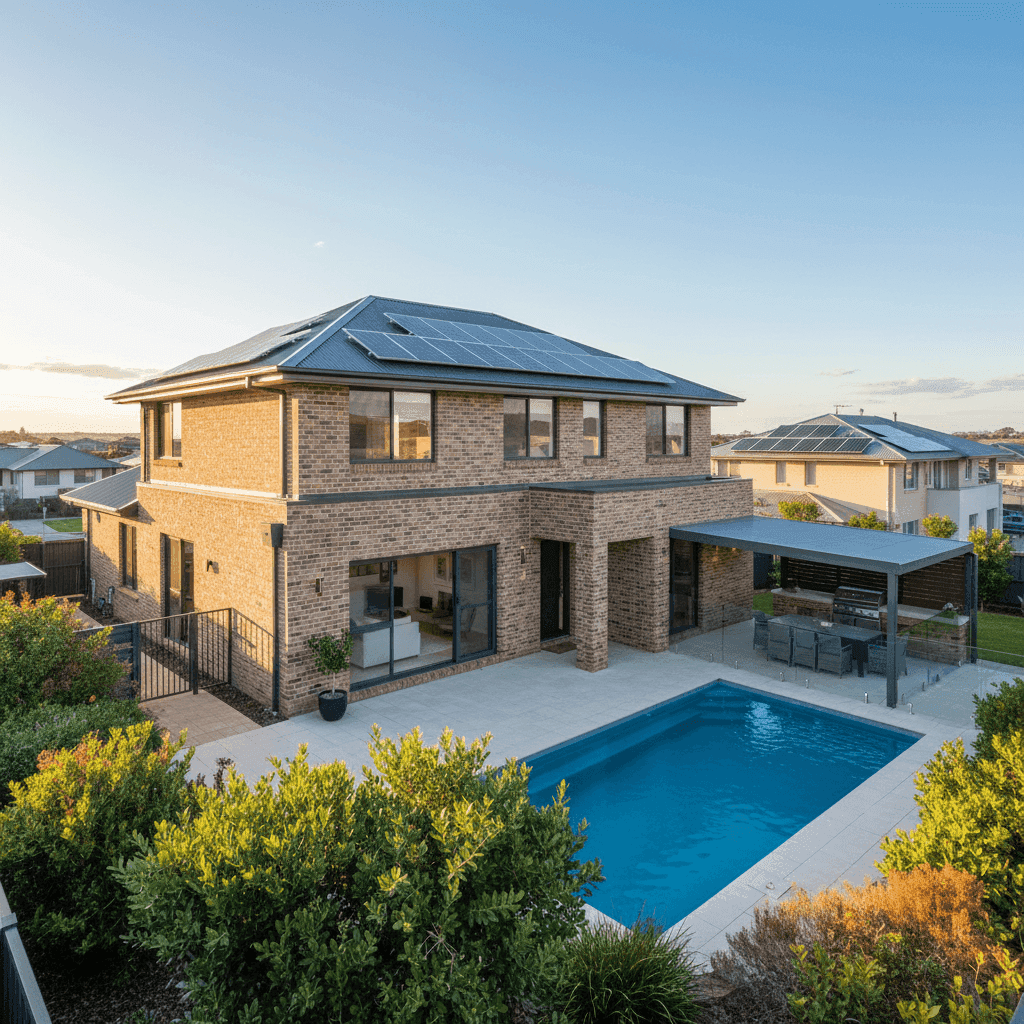

That said, "expensive" doesn't automatically mean "wrong." A high sum insured of $989,000 for a 244 sqm home with top-of-the-range fittings, a pool, solar panels, and ducted climate control will naturally push premiums upward. The question is whether the insurer's pricing reflects your actual risk profile — or whether a comparable policy could be found at a better price point.

---

How Sunshine Bay Compares

Understanding where your suburb sits relative to the broader market is one of the most useful tools a homeowner has. Here's how Sunshine Bay measures up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Sunshine Bay (2536) | $3,425/yr | $3,347/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Shoalhaven LGA | $11,272/yr | — |

A few things stand out here. The NSW and Shoalhaven LGA averages look dramatically high — but this is largely a statistical effect driven by high-value or high-risk properties pulling the mean upward. The median figures are far more representative of what most homeowners actually pay, and Sunshine Bay's median of $3,347 is actually quite competitive against NSW's median of $3,770.

What this tells us is that Sunshine Bay is a relatively affordable suburb to insure compared to many parts of New South Wales — but the quote under review is sitting above that local norm. You can explore suburb-level data in more detail on our Sunshine Bay insurance stats page, or broaden your view across the NSW insurance landscape and national benchmarks.

(Note: Suburb comparison is based on a sample of 15 quotes, so treat these figures as a solid guide rather than an exhaustive dataset.)

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge. Here's how they play out:

Brick Veneer Walls & Colorbond Roof Brick veneer is generally viewed favourably by insurers — it offers solid fire resistance and structural durability. Paired with a steel Colorbond roof, which is lightweight, rust-resistant, and performs well in coastal and storm conditions, this combination typically attracts more competitive premiums than, say, weatherboard cladding or terracotta tiles.

Slab Foundation & Tiled Flooring A concrete slab foundation is considered low-risk by most insurers — there's no subfloor space to trap moisture or harbour pests, and slabs are robust against movement in stable soil conditions. Tiled flooring similarly adds minimal risk and is easy to repair or replace.

Top-of-the-Range Fittings This is likely one of the more significant premium drivers. High-end fixtures and finishes — think stone benchtops, premium cabinetry, designer tapware — substantially increase the cost to rebuild or repair. A sum insured of $989,000 for a 244 sqm home reflects this quality level, and insurers price accordingly.

Swimming Pool A pool increases liability exposure and adds to the overall replacement value of the property. Most insurers factor this into their building premium, particularly when assessing the cost to repair surrounds, filtration systems, and associated structures.

Solar Panels Rooftop solar is increasingly common in coastal NSW, but it does add complexity to a claim — panels can be damaged in storms, hail, or bushfire ember attacks, and their replacement cost adds to the insured value. Some insurers are more competitive than others when it comes to pricing solar-equipped homes.

Ducted Climate Control A ducted air conditioning system is a significant fixed asset within the building. Its inclusion in the sum insured is appropriate and will contribute modestly to the overall premium.

No Cyclone Risk Sunshine Bay falls outside designated cyclone risk zones, which is a meaningful advantage. Properties in cyclone-prone areas of Queensland or northern WA can see premiums two to three times higher for equivalent homes. This factor works in the homeowner's favour here.

---

Tips for Homeowners in Sunshine Bay

1. Shop around — seriously With this quote sitting above the 75th percentile for the suburb, there's a reasonable chance a comparable policy exists at a lower price. Different insurers weight risk factors differently, and a home with brick veneer walls, Colorbond roofing, and a slab foundation may be priced more favourably by some underwriters than others.

2. Review your sum insured carefully At $989,000 for a 244 sqm home, the sum insured reflects the top-of-the-range fittings and inclusions. It's worth using a building cost calculator periodically to ensure this figure is accurate — being over-insured costs you in premiums, while being under-insured can leave you exposed at claim time.

3. Consider your excess strategically The building excess on this policy is $2,000. Opting for a higher excess (say, $2,500 or $3,000) can reduce your annual premium — sometimes meaningfully. If you have the financial buffer to cover a larger out-of-pocket cost in a claim scenario, this is a straightforward way to bring your premium down.

4. Ask about discounts for security and safety features Insurers often offer discounts for properties with monitored alarm systems, deadbolts, or fire suppression equipment. If your home has any of these, make sure your insurer knows — and if it doesn't, some modest investments in home security could pay for themselves in premium savings over time.

---

Compare Your Options with CoverClub

Whether you're renewing an existing policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not paying more than you need to. At CoverClub, we make it easy to see how your premium stacks up against real data from your suburb and across Australia. Get a home insurance quote today and find out if there's a better deal waiting for you.