Sunshine Beach is one of the Sunshine Coast's most sought-after coastal addresses — and with that prestige comes a property market that demands serious insurance consideration. This article analyses a Home and Contents insurance quote for a five-bedroom, five-bathroom free standing home in Sunshine Beach, QLD 4567, breaking down whether the premium is competitive and what local factors are shaping the cost.

---

Is This Quote Fair?

The annual premium for this property came in at $5,603 per year (or $537/month), covering a building sum insured of $3,000,000 and $180,000 in contents. Our independent price rating for this quote is FAIR — Around Average.

To put that in context:

- The suburb average for Sunshine Beach is $6,142/yr — meaning this quote sits $539 below what others in the postcode are typically paying.

- The suburb median is $3,726/yr, which reflects the wide spread of property types and values across the area.

- At the 75th percentile, Sunshine Beach premiums reach $7,680/yr, so this quote is comfortably within the middle range of the market.

Given the high building sum insured ($3M) and generous contents cover ($180,000), landing at $5,603 is a reasonable outcome. Homeowners with lower rebuild values or fewer contents would naturally expect to pay less, so the "fair" rating is appropriate when the full scope of cover is taken into account. Both the building and contents excesses are set at $5,000, which is on the higher side and will be contributing to keeping the premium more competitive — a common trade-off worth understanding before you commit.

---

How Sunshine Beach Compares

Sunshine Beach sits within the Noosa Local Government Area (LGA), and the insurance data here tells a striking story. The Noosa LGA average premium is $18,770/yr — an extraordinary figure driven by high-value coastal properties, flood and storm risk in certain pockets, and the sheer concentration of premium real estate in the region. This quote at $5,603 is well below that LGA average, which suggests the specific property characteristics are working in the homeowner's favour.

Zooming out further:

| Benchmark | Premium |

|---|---|

| Sunshine Beach suburb average | $6,142/yr |

| Sunshine Beach suburb median | $3,726/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Queensland as a whole carries some of Australia's highest home insurance premiums, largely due to cyclone, flood, and storm exposure across the state. The QLD average of $9,129/yr is significantly above the national average of $5,347/yr. This property's premium of $5,603 actually sits below the QLD state average and very close to the national average — a solid result for a high-value coastal home.

It's worth noting that the suburb sample size is 36 quotes, which is a reasonable dataset but still relatively small. Averages can shift as more data comes in, so checking the latest Sunshine Beach insurance stats regularly is worthwhile.

---

Property Features That Affect Your Premium

Several characteristics of this home are likely influencing the premium — some favourably, others less so.

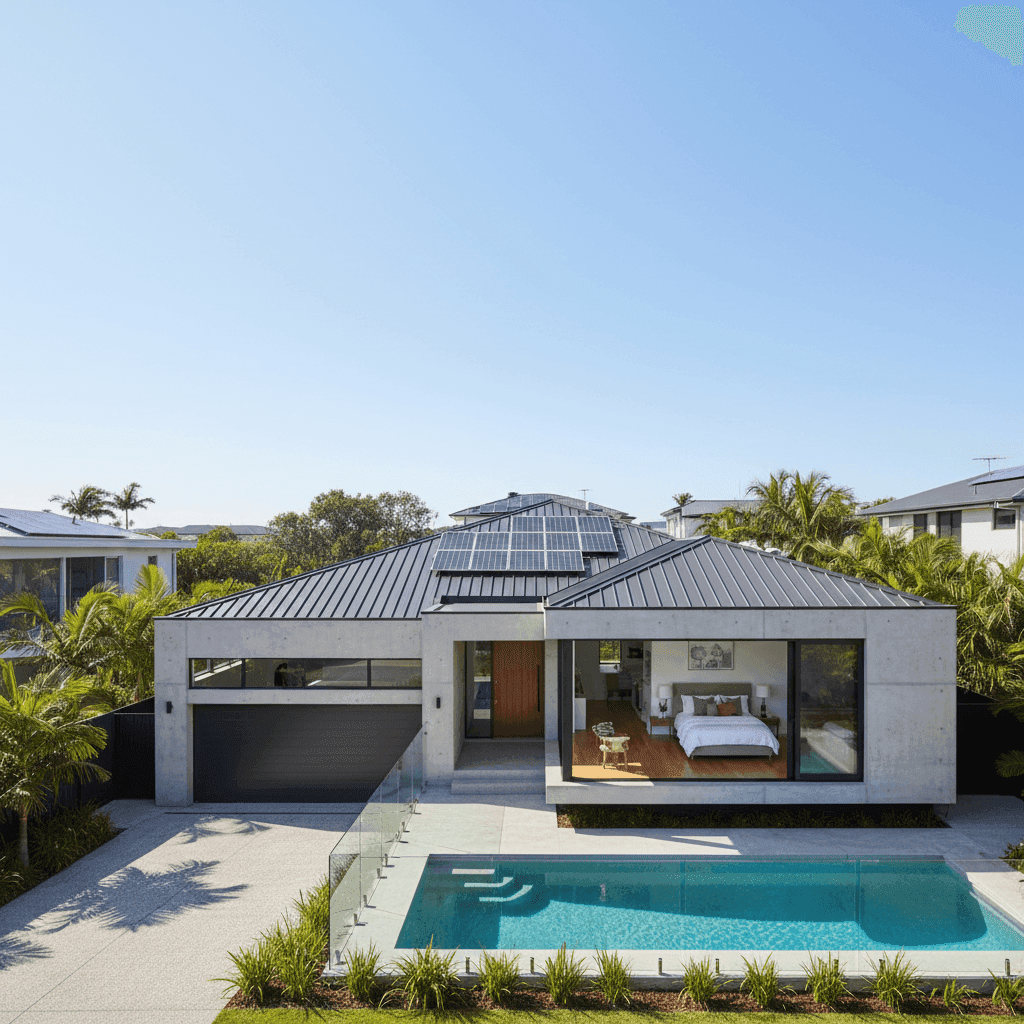

Concrete external walls are one of the most insurance-friendly construction types available. Concrete is highly resistant to fire, wind, and impact damage, and insurers typically reward this with lower premiums compared to timber or weatherboard construction.

Steel/Colorbond roofing is similarly well-regarded by underwriters. It's durable, resistant to ember attack, and performs well in high-wind events — all relevant considerations for a coastal Queensland property.

Slab foundation is a standard, low-risk foundation type that doesn't introduce the elevated flood or moisture concerns that some other foundation styles might.

Tile flooring is a practical choice in coastal homes and generally doesn't attract any premium loading.

Above-average fittings quality is an important factor here. High-end fixtures, finishes, and appliances increase the cost to rebuild or repair, and this is reflected in the elevated building sum insured of $3,000,000. Insurers price accordingly.

Swimming pool adds liability and replacement cost considerations to the policy. Pools can be a source of claims — from accidental damage to third-party liability — so their presence does influence pricing.

Solar panels are increasingly common in Queensland homes, but they do add to the replacement value of the building. A quality solar system on a 315 sqm home can represent tens of thousands of dollars in rebuild costs.

Ducted climate control is another above-average inclusion that adds to the overall insured value of the home.

Slightly elevated (less than 1m) — while this property isn't a raised Queenslander, even a modest elevation can assist with drainage and reduce the risk of inundation during heavy rainfall events, which is a positive factor in coastal Queensland.

No cyclone risk classification is a meaningful premium saver. Many parts of Queensland attract cyclone loading, but Sunshine Beach falls outside the designated cyclone risk zone, removing what can be a very significant cost component for homeowners further north.

---

Tips for Homeowners in Sunshine Beach

1. Review your sum insured regularly With a building sum insured of $3,000,000, it's essential to ensure this figure accurately reflects the cost to rebuild — not the market value of the property. Construction costs have risen sharply in recent years, and underinsurance is a real risk. Use a quantity surveyor or your insurer's building calculator to validate this figure annually.

2. Understand your excess trade-off Both excesses on this policy are set at $5,000. While this helps reduce the annual premium, it means you'll be out of pocket by $5,000 before your insurer contributes to any claim. Consider whether this level of self-insurance aligns with your financial position and claims history.

3. Don't overlook contents coverage $180,000 in contents cover is a solid figure, but for a five-bedroom home with above-average fittings, it's worth itemising your high-value possessions — jewellery, art, electronics, and outdoor furniture — to confirm you're not underinsured in this area.

4. Leverage your low-risk construction When shopping around, make sure insurers are correctly capturing your concrete walls and Colorbond roof. These details can significantly affect your quote, and some comparison tools or call centres may default to less favourable construction categories if not specified clearly.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or insuring a new purchase, it pays to compare. CoverClub makes it easy to benchmark your premium against real data from your suburb, LGA, and across Queensland. Get a home insurance quote today and see how your current cover stacks up — you might be surprised by what you find.