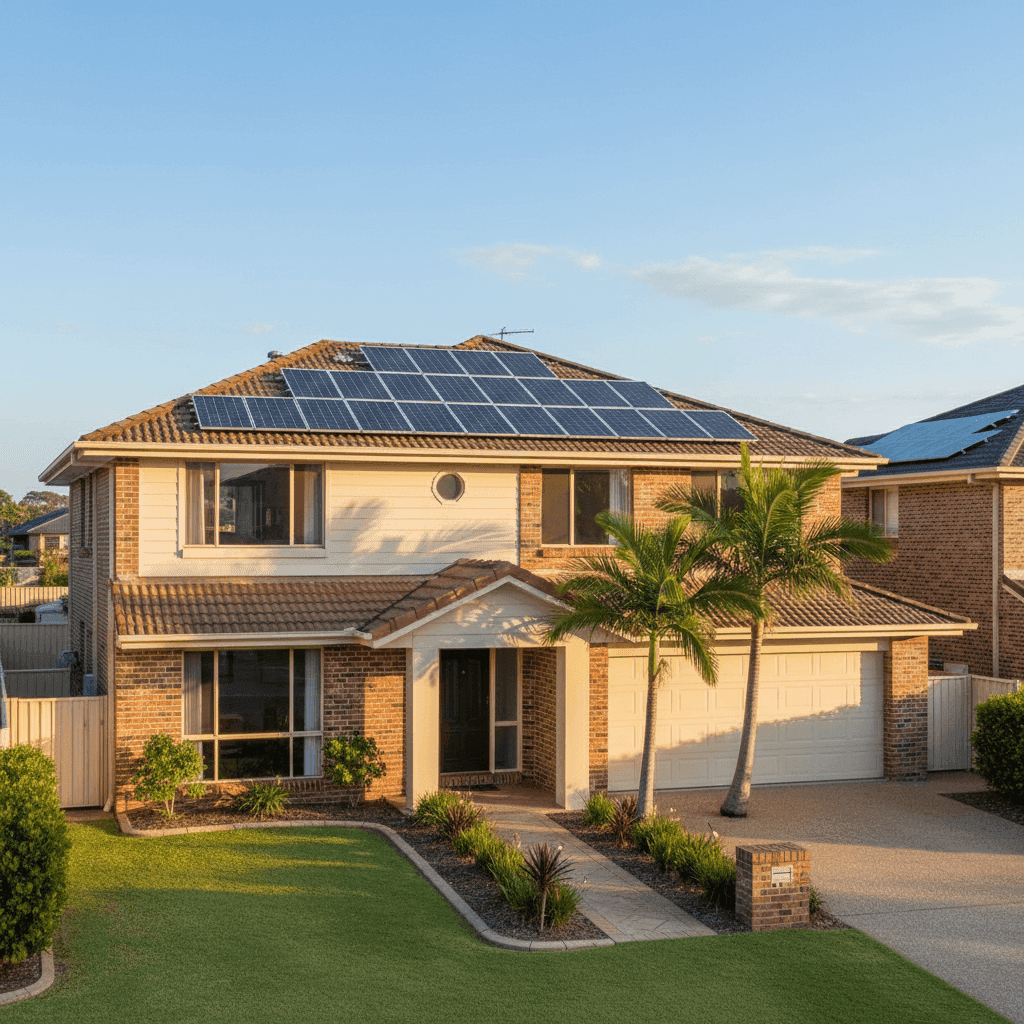

If you own a free standing home in Surfers Paradise, QLD 4217, you already know this stretch of the Gold Coast is one of Australia's most desirable — and most insured — addresses. But desirability comes at a cost, and home insurance is no exception. This article breaks down a real building-only insurance quote for a five-bedroom property in the suburb, benchmarks it against local, state and national data, and offers practical guidance for homeowners looking to get better value.

---

Is This Quote Fair?

The quote in question comes in at $11,216 per year (or $1,075 per month) for building-only cover on a five-bedroom, four-bathroom free standing home, with a sum insured of $1,127,000 and a standard $1,000 building excess.

Our price rating for this quote is Expensive — Above Average.

To put that in perspective: the average building-only premium across the 30 quotes we've collected for Surfers Paradise sits at $6,457 per year, with a median of $5,750. This quote lands well above the suburb's 75th percentile of $7,317, meaning it's higher than roughly three-quarters of comparable quotes in the area. That's a significant gap, and one worth investigating before renewing or accepting as-is.

It's worth noting that a $1,127,000 sum insured is substantial — and rightfully so for a large, well-appointed home. However, the premium-to-coverage ratio still warrants scrutiny, particularly when compared against what other Surfers Paradise homeowners are paying for similar cover.

---

How Surfers Paradise Compares

Zooming out to a broader view helps contextualise just how much location influences what you pay.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Surfers Paradise (4217) | $6,457/yr | $5,750/yr |

| Gold Coast LGA | $8,161/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Queensland's average premium of $9,129 is notably higher than the national average of $5,347 — a reflection of the state's elevated exposure to extreme weather events including flooding, storms and cyclones. Second, the wide gap between Queensland's average ($9,129) and its median ($3,903) signals that a relatively small number of high-risk or high-value properties are pulling the average up considerably.

Surfers Paradise itself sits below the broader Gold Coast LGA average of $8,161, which suggests the suburb — despite its coastal profile — may benefit from some favourable risk characteristics compared to other parts of the region.

You can explore more localised data on the Surfers Paradise insurance stats page, or compare it against Queensland-wide figures and national benchmarks.

---

Property Features That Affect Your Premium

Understanding what drives your premium is the first step to managing it. Several features of this particular property have a meaningful impact on what insurers charge.

Construction Era and Materials

Built in 1982, this home sits in an age bracket that insurers view with some caution. Homes from this period may have ageing plumbing, electrical systems or roofing that increases the likelihood of a claim. That said, brick veneer walls and a tiled roof are generally well-regarded by underwriters — both materials are durable, fire-resistant and perform reasonably well in storm conditions.

Slab Foundation

A concrete slab foundation is standard for Queensland homes of this era and is generally considered a neutral-to-positive factor for insurers. Slabs are less susceptible to termite damage than timber subfloors and can offer structural stability — though they can be costlier to repair if issues do arise.

Size and Fittings Quality

At 105 sqm of building area across five bedrooms and four bathrooms, this is a compact footprint for the number of rooms — which may indicate multi-storey construction or efficient layout. The above average fittings quality is a notable premium driver: higher-quality fixtures, finishes and appliances cost more to repair or replace, and insurers price accordingly.

Solar Panels

The presence of solar panels adds an additional layer of risk that many homeowners overlook. Panels increase the replacement cost of the roof, introduce potential electrical hazards, and may require specialist trades for repair. Most policies cover solar panels under building insurance, but it's worth confirming the specifics with your insurer.

Ducted Climate Control

A ducted climate control system is another above-average feature that contributes to the overall replacement cost of the building. These systems are expensive to install and repair, and their inclusion in the sum insured is essential to avoid being underinsured.

---

Tips for Homeowners in Surfers Paradise

1. Review Your Sum Insured Annually

With a sum insured of $1,127,000, it's critical to ensure this figure reflects the true cost of rebuilding — not the market value of the land. Construction costs in South East Queensland have risen sharply in recent years. Use a building cost calculator or consult a quantity surveyor to keep your cover accurate and avoid underinsurance.

2. Shop Around — Seriously

This quote is rated expensive relative to the suburb average. The 25th percentile of Surfers Paradise quotes sits at just $4,346 per year — less than half of this premium. That doesn't mean you should automatically chase the cheapest option, but it does mean there's meaningful room to compare. Head to CoverClub's quote tool to see what multiple insurers would offer for your property.

3. Ask About Solar Panel Coverage

Given the solar installation on this property, confirm explicitly with any insurer whether panels are included in the building sum insured, whether there are sub-limits, and what happens in the event of storm or hail damage. Not all policies treat solar the same way.

4. Consider the Excess Trade-Off

This quote carries a $1,000 building excess. Opting for a higher voluntary excess — say, $2,500 or $5,000 — can meaningfully reduce your annual premium. If you have the financial buffer to absorb a larger out-of-pocket cost in the event of a claim, this is often a smart lever to pull, particularly on a premium this size.

---

Ready to Compare?

A quote this far above the suburb average is a strong signal to explore your options. CoverClub makes it easy to compare home insurance quotes from multiple Australian insurers in one place — so you can see whether you're getting a fair deal or paying too much for your Surfers Paradise home. Get a quote today and find out what you could be saving.