Sussex Inlet is a peaceful coastal town on the NSW South Coast, nestled between St Georges Basin and the Tasman Sea. It's a sought-after location for families and sea-changers alike — but like many waterside communities, the cost of protecting your home here deserves a close look. This article analyses a recent home and contents insurance quote for a four-bedroom, two-bathroom free-standing home in Sussex Inlet (postcode 2540), breaking down whether the premium is competitive and what's driving the price.

---

Is This Quote Fair?

The quote in question comes in at $4,059 per year (or $397/month), covering a building sum insured of $779,000 and $50,000 in contents. Our price rating for this quote is Expensive — Above Average.

To put that in perspective:

- The suburb average for Sussex Inlet is $2,434/yr, and the median sits at $2,036/yr

- The NSW state average is $3,801/yr, with a median of $3,410/yr

- The national average across Australia is $2,965/yr, with a median of $2,716/yr

This quote sits 67% above the suburb average and 6.8% above the NSW state average — a meaningful gap. However, context matters. The building sum insured of $779,000 is substantial, and a newly built 214 sqm home with quality fittings, solar panels, and ducted climate control will naturally attract a higher replacement cost than older or smaller properties in the same suburb. The comparison pool of 54 quotes in the area likely includes a wide range of property sizes and values, which can pull the suburb average down considerably.

That said, the premium is still on the higher end — even when accounting for the property's size and features — and it's worth exploring whether a better rate is available elsewhere.

---

How Sussex Inlet Compares

Sussex Inlet's insurance data reveals a wide spread of premiums across the suburb. The 25th percentile sits at just $1,229/yr, while the 75th percentile reaches $2,881/yr — indicating significant variation depending on the property, insurer, and level of cover selected.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,059 |

| Sussex Inlet Average | $2,434 |

| Sussex Inlet Median | $2,036 |

| NSW Average | $3,801 |

| NSW Median | $3,410 |

| National Average | $2,965 |

| National Median | $2,716 |

When you look at NSW home insurance averages, this quote sits above the state norm — which itself is already elevated compared to national benchmarks. NSW homeowners generally pay more than the national average due to factors like storm exposure, bushfire risk in many regions, and higher property values along the coast.

Sussex Inlet's relatively lower suburb average likely reflects a mix of older homes, smaller properties, and varying levels of cover across the sample. A brand-new, well-appointed 214 sqm home with a high building sum insured is a different proposition entirely, and the premium reflects that.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct influence on the insurance premium:

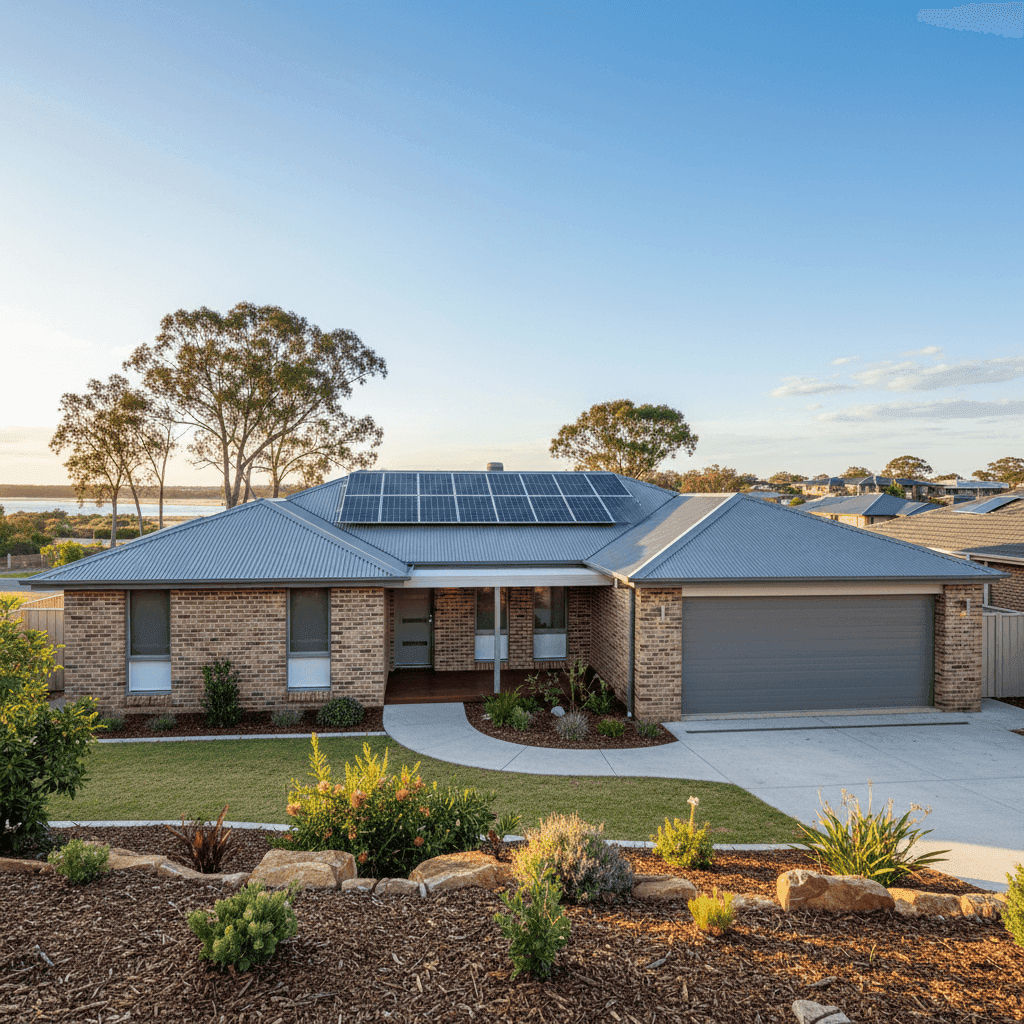

Newly built in 2025 — New homes are generally well-regarded by insurers. Modern building standards mean better structural integrity, updated electrical systems, and compliance with current fire and flood codes. This can work in your favour, though the high replacement cost of a new build naturally pushes the sum insured — and therefore the premium — upward.

Brick veneer construction with a Colorbond steel roof — Brick veneer is a popular and insurer-friendly wall material, offering solid fire resistance and durability. Colorbond roofing is equally well-regarded: it's lightweight, corrosion-resistant, and handles the coastal environment well. These materials are unlikely to attract any loading on your premium and may even contribute to a more favourable rate compared to timber-clad or tiled-roof alternatives.

Slab foundation — Concrete slab is a stable and low-maintenance foundation type that insurers view positively. It carries less risk of subsidence or pest damage compared to raised timber stumps.

Timber and laminate flooring — While aesthetically popular, timber and laminate flooring can be more costly to repair or replace after water damage than tiles. This may contribute marginally to the contents or building premium.

Solar panels — Solar systems are increasingly common, but they do add to the replacement value of the property. Insurers need to factor in the cost of replacing panels and associated equipment, which can nudge the building sum insured higher. It's worth confirming with your insurer that your solar system is explicitly covered under the policy.

Ducted climate control — Ducted air conditioning is a fixed building fixture and should be covered under the building sum insured. Like solar, it adds to replacement cost and is worth verifying in the policy schedule.

No pool, no cyclone risk zone — The absence of a pool removes a common liability and maintenance risk factor. And while Sussex Inlet is on the coast, it falls outside designated cyclone risk areas, which keeps wind-related loadings off the table.

---

Tips for Homeowners in Sussex Inlet

1. Shop around — seriously A premium of over $4,000 for a coastal NSW home isn't unusual, but it's not inevitable either. Given this quote sits above both the suburb and state averages, comparing at least three to five insurers could uncover meaningful savings. Get a comparison quote at CoverClub to see what other providers are offering for the same level of cover.

2. Review your building sum insured carefully At $779,000, the building sum insured is the single biggest driver of this premium. Make sure this figure reflects the actual cost to rebuild — not the market value of the property. Over-insuring can cost you hundreds of dollars per year unnecessarily. Tools like the Cordell Sum Sure calculator (often available through insurers) can help you arrive at an accurate figure.

3. Consider your excess settings This quote carries a $2,000 building excess and $1,000 contents excess. Opting for a higher excess — say, $2,500 or $3,000 on the building — can reduce your annual premium. Just make sure the excess is an amount you could genuinely afford to pay in the event of a claim.

4. Confirm solar and climate control are covered With solar panels and ducted air conditioning on the property, it's essential to verify these are explicitly listed in your policy. Some policies cover them automatically under building, while others require specific endorsement. A quick call to your insurer can save a nasty surprise at claim time.

---

Compare Your Options with CoverClub

Whether you're a new homeowner in Sussex Inlet or reviewing an existing policy, it pays to benchmark your premium against the market. CoverClub makes it easy to see how your quote stacks up against suburb, state, and national data — so you can make an informed decision rather than just accepting the first figure you're given. Start comparing home insurance quotes today and find out if you could be paying less for the same protection.